FRMO Corp. (FRMO, Financial) is out with another annual letter to investors by CEO Murray Stahl (Trades, Portfolio) and CFO Steven Bregman, and as always, it is highly interesting and a must-read for any enterprising value investor who enjoys creative ideas. The full letter can be read here, but I have taken the liberty to summarize the actionable investment ideas for you:

1. CASH

If there is one important idea in the letter it is to keep cash. For some time now, Stahl and Bregman have been fairly bearish on the outlook for the investment landscape. Especially liquid investments contained in many ETF’s are highly unattractive to them.

Readers of our Shareholder Letter for 2015 will recall that in the first paragraph we made reference to exceedingly low interest rates. We did not imagine the appearance of negative interest rates. As far as we can determine, after consulting Sidney Homer’s classic text The History of Interest Rates, we are now in the lowest interest rate environment in the last 5,000 years. This is important, since interest rates establish value for all financial assets. Consequently, valuations for many types of financial assets are high. The investment opportunity set is, therefore, unusually narrow. It is for this reason that we carry about $49 million of cash and cash equivalents on our balance sheet. Indeed, viewed on a tangible assets basis, we are largely uninvested, since much of the balance sheet valuation of our Horizon Kinetics LLC assets is necessarily intangible.

One of the solutions proposed and put in practice by the duo is to hoard cash in large quantities. Not just as a defensive measure, but also in an offensive way. The cash can be used ONCE asset prices go down. What is merely zero yielding cash now, can be highly lucrative firepower later. Their argumentation strongly reminds me of "The Dao Of Capital" by Spitznagel. From the blurb:

We arrive at his central investment methodology of Austrian Investing, where victory comes not from waging the immediate decisive battle, but rather from theroundabout approach of seeking the intermediate positional advantage (what he calls shi), of aiming at the indirect means rather than directly at the ends.

The roundabout is where he bets first on something that will decline in crisis, to reap rewards exactly at a time where liquidity comes at a premium. It is then the Austrian Investor is flush with cash and can harvest.

2. BITCOIN

Stahl and Bregman have, as long as I have tracked their moves, taken optionality very seriously. One outgrowth of that preference is the ownership interests in many exchanges of financial assets carried by FRMO. Bitcoin (BTC, Financial) and other altcoins are, in essence, exchanges as well. They represent a method to exchange value or store value. Still in the early innings of what they could be, there is tremendous optionality within Bitcoin, the blockchain and other altcoins. FRMO holds an investment in the Digital Currency Group, which is an investor in many different bitcoin and blockchain related companies. Among other assets, it holds a stake in Coinbase (a very user friendly bitcoin and ethereum wallet) and the GBTC, which is one of the few ways institutional investors can buy Bitcoin. In addition in 2016, as per the annual letter, Horizon Kinetics also established a fund that invests in bitcoin:

The fund established an investment maximum of $50,000 per client. We are not aware of any other firm that so constrains client contributions. However, we believe it is the easiest and most obvious way to control risk. We simply limit the amount of money that can possibly be lost to an amount that is tolerable. Investment firms often complain about the short-term focus of clients. The short-term focus is more understandable if the investment in failure mode could quite negatively impact their lives. In any case, we rapidly sold essentially every available slot in the fund.

I like this for two reasons: 1) the fact that they set up another successful fund and 2) This increases FRMO’s exposure to crytocurrency, a currency or asset class (however you want to call it) that I’m bullish on as it solves real-world problems. For a more in-depth discussion, you can reference my writing in 5 reasons to buy bitcoin and 6 reasons why you shouldn’t invest in bitcoin.

MICROCAPS

As an extension of Stahl and Bregman’s distrust of large liquid assets, they pursue lots of illiquid assets but also have become interested in the micro cap space.

As a consequence of the industrial scale upon which indexes operate, the largest companies frequently have valuations far in excess of smaller companies. For example, large-capitalization shares have outperformed micro-capitalization equities for years. The S&P 500 trades at nearly two times the price-to-book-value ratio of a typical micro-capitalization index. This is very unusual. However, the enormous industrial scale of indexation investing, as well as the market capitalization float adjusted methodology of weighting, requires maximum trading liquidity that simply cannot be provided by genuinely small companies. Another factor, the importance of which is difficult to quantify, is that the large companies frequently pay robust dividends. This is not usually true of small firms. There are many large capitalization equity indexes that are marketed as so-called “bond substitutes.” This is nothing other than a consequence of the worldwide central bank effort to lower interest rates, to zero in many instances. The theory behind this effort was to essentially force investors into risk-based assets and, hence, stimulate economic growth.

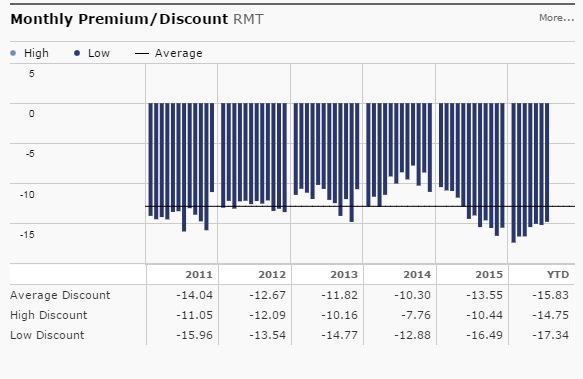

It is not referenced by name in the current annual letter, but I believe their investment in the Royce Microcap Trust (RMT, Financial), through Horizon Kinetics funds, is inspired by this idea. This is a closed-end fund that is trading at a historically very sizeable discount, while micro caps have underperformed for years on end. Lots of potential to get a double whammy here if both micro caps close the valuation gap with large caps and the discount to intrinsic value narrows. As you can see below, the discount is really much wider than it has historically been:

Disclosure: Long FRMO Corp and Bitcoin.

Start a free 7-day trial of Premium Membership to GuruFocus.