It isn’t often that you see a stock that reported more than 4% revenue growth for the last five quarters have its stock slide by more than 15%, but that’s exactly the position Nike (NKE, Financial) is in right now.

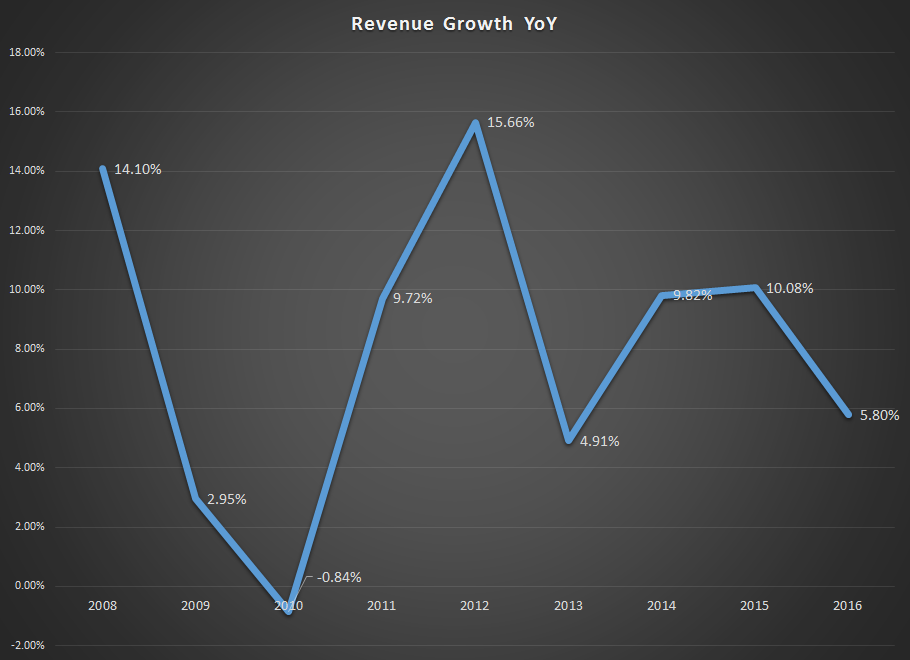

The footwear maker’s annual revenue grew by 5.8% last year while the stock price moved down 17% from its 2015 high of $66 to the current $55 level. Nike’s year-to-date return of 0.03% makes you question the company’s growth story. But let’s analyze this in a little more depth and see why the market seems to be in a not-so-good mood with the company.

We know that Nike is aiming to hit $50 billion in sales by 2020, a reachable number considering the segment in which the company is operating. The footwear market is highly fragmented and worth more than $200 billion and growing. As such, Nike, the undisputed leader of the segment, has plenty of opportunity to keep growing at a steady pace. But to reach the $50 billion target the company has to grow at around the 10% level, not the 6% level it showed last year.

One of the biggest reasons for the lackluster stock performance is the slowdown in revenue growth. Since Nike’s growth has been a bit up and down in the last 10 years, numbers in 2016 have been a bit of shock for many investors as everyone including Nike was expecting the company to stay at or above the 10% level. As the company reported quarter after quarter of sub-6% growth, the stock kept moving lower and lower over the last eight months.

“After years of robust growth, Nike is facing challenges on several fronts. The strong U.S. dollar is hurting sales overseas, and footwear competition is mounting. Under Armour Inc. is making headway in Nike’s longtime stronghold of basketball shoes, while a revived Adidas AG is encroaching on the running-sneaker segment. That’s raising concern about Nike’s plan to reach $50 billion in revenue by 2020, up from about $32 billion now. Still, its China division showed no signs of slowing down, and an inventory glut in North America that hampered results has largely been fixed.” - Bloomberg

With more than half of its sales coming from overseas markets Nike’s top line takes a huge hit when the dollar gets stronger; and, unfortunately, under the current market condition there is no way that the trend can reverse itself. With Nike’s sales expected to increase at a much faster rate in international markets compared to the home market, Nike will continue to face forex issues for many years.

But on the positive side, even if the company fails to achieve its self-proclaimed target by 2020 Nike will always be a "standout" brand because of the huge lead it has established over other players in the market such as adidas (ADS, Financial) and the newcomer, Under Armour (UA, Financial).

Nike is still the segment leader and also enjoys better margins than other companies in the industry, and the company is well received all over the world. This is not the industry where someone suddenly comes out of the woodwork and sweeps the world off its feet. You have to be in the game for many year to even think of getting close to doing what a company like Nike has achieved.

Under Armour, despite the strong double-digit growth it been posting for the last 10 years, is more than $25 billion away from Nike, which clearly validates the kind of control the company has over the market. Despite the drop, Nike is still trading at 25 times earnings, which is a reasonable level for a brand like Nike that has plenty of opportunity to keep growing over the next two decades.

Disclosure: I have no positions in any of the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.