With both Buffett and Klarman loading up on refineries, it is hard not to be intrigued. Last month, I examined what could motivate Buffett to pursue Philips 66Â and in this article I’ll do the same for Klarman, who acquired 16% of PBF Energy (PBF, Financial).

I believe there are three important drivers of Klarman’s interest:

- High insider ownership

- Valuable tangible assets that add a margin of safety

- Low valuation in relation to operating cash flow

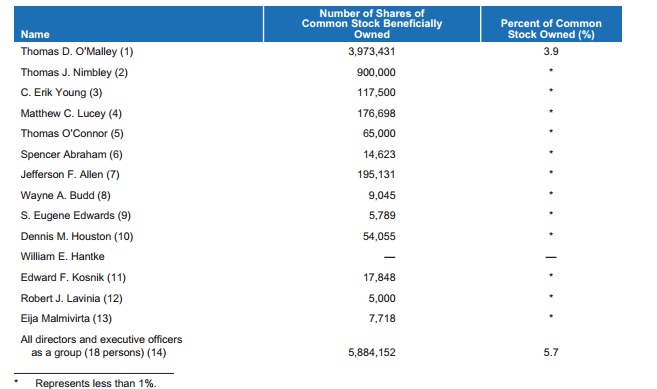

High Insider Ownership

From the company’s proxy I pulled the following table that shows the executive team owns a sizable chunk of shares. However, Malley, 75, has stepped down from the board and is only a consultant to the company at this time. CEO Nimbley’s stake is worth ~$20 million. Definitely a stake most people would be careful to protect, although it should be put in perspective of his $8 million annual compensation. I’d really like to see him increase the size of his stake relative to annual compensation.

Margin of safety due to valuable underlying assets

The cost of building a new oil refinery today may be made prohibitively expensive by environmental legislation, endowing older facilities with a scarcity value.

Klarman in his famous but rare book: Margin of Safety

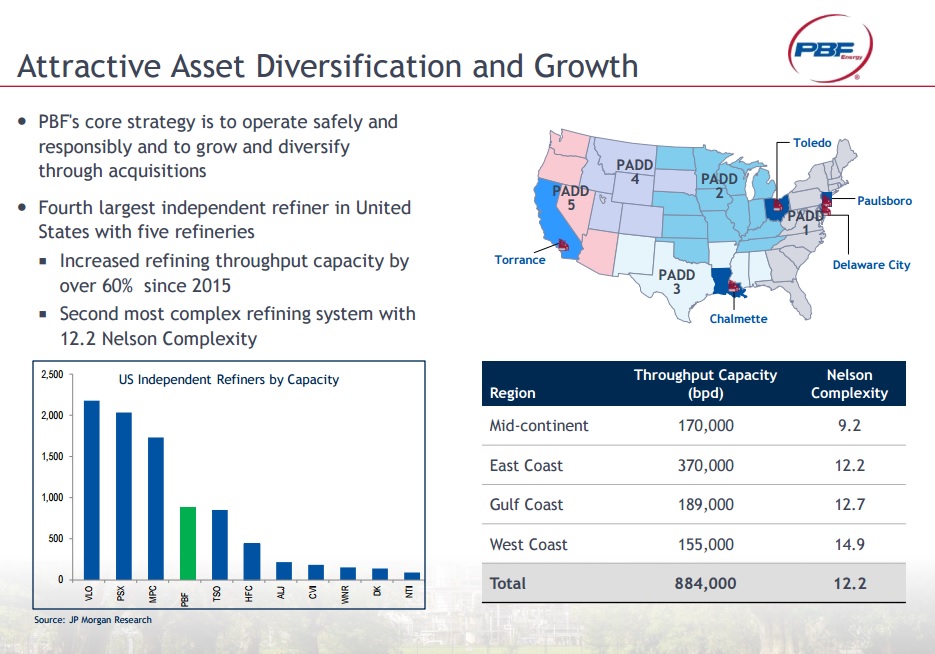

PBF Energy may be the fourth largest refiner by throughput in terms of bpd, but that’s not the whole story. Tesoro (TSO, Financial) is close on its heels while the firm severely lags the nr.1 - nr.3 on thoroughput. On the other hand, its Nelson Complexity rating is quite high and it takes second place in that ranking. The Nelson Complexity informs us about the quality of the refining capacity. The higher the rating the better. A high rating also indicates the assets, used to attain it, are generally more valuable. Something to keep in mind. For a full definition, check Wikipedia, but here’s the gist of it:

The NCI assigns a complexity factor to each major piece of refinery equipment based on its complexity and cost in comparison to crude distillation, which is assigned a complexity factor of 1.0. The complexity of each piece of refinery equipment is then calculated by multiplying its complexity factor by its throughput ratio as a percentage of crude distillation capacity. Adding up the complexity values assigned to each piece of equipment, including crude distillation, determines a refinery’s complexity on the NCI.

The NCI indicates not only the investment intensity or cost index of the refinery but also its potential value addition. Thus, the higher the index number, the greater the cost of the refinery and the higher the value of its products.

The table, from the company’s Barclays presentation, below shows the relative position of the company in terms of throughput:

Â

Valero (VLO, Financial) has an enterprise value of $28 billion, Philips 66 (PSX, Financial) has an enterprise value of $49 billion, Marathon Petroleum Corp. (MPC, Financial) has a enterprise value of $38 billion. Tesoro has an enterprise value of $15 billion. In contrast, PBF Energy’s total enterprise value is only $3.5 billion.

I’ll be the first to say these companies are not one-to-one comparable. For example in my article on PSX, the central idea came down to the market perceiving the company as a refiner while this is only one part of its operations and pipelines made up a sizeable chunk of value.

Each company has its individual characteristics. However, all five are considered to be primarily refining businesses. PBF ranks fourth in terms of throughput of raw material and it ranks second in terms of the complexity of refining processes it can undertake. Meanwhile, its enterprise value is a shadow of that of its peers. On a relative basis, as a PBF investor, you are buying lots of refiner for your buck.

On top of that the company owns an equity interest in a drop-down company called PBF Logistics with a market cap of $850 million. PBF’s stake should be worth in the ballpark of $400 to $450 million.

Low Multiple to Operating Cash Flow

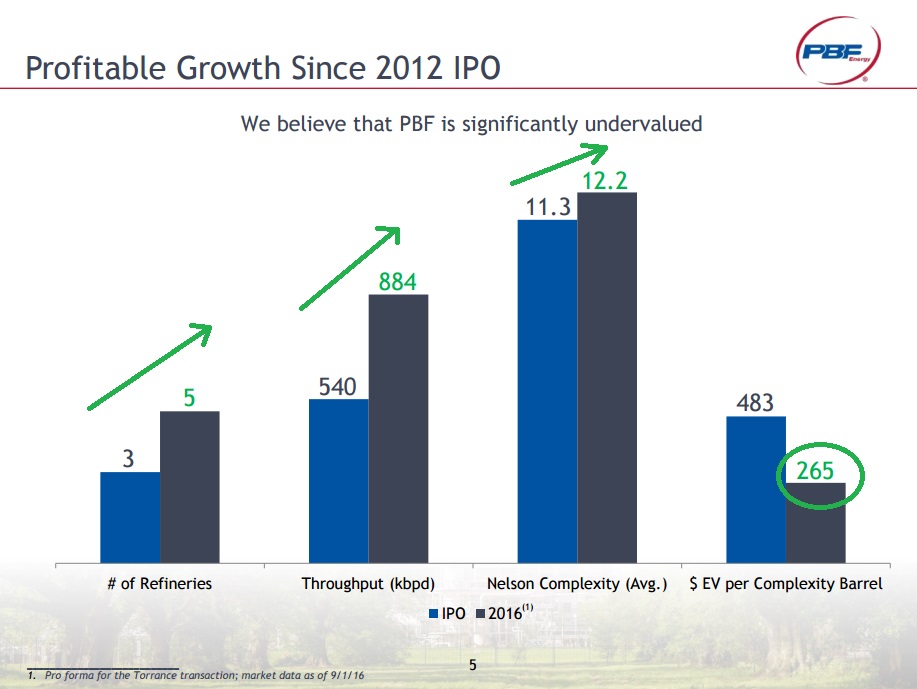

PFB has been growing quite aggressively over the past few years:

To an extent, this has obscured FCF. If I look at operating free cash flow, we are looking at ~$4.5 per share. Some guesswork is involved to separate maintenance CapEx from growth CapEx to find a reasonable FCF figure, but I would be surprised if it were below $400 million, or $4 per share. Given that shares trade at $21 per share, potentially PFB trades at just 5x normalized FCF. Just the kind of bargain I imagine Klarman would look for.

Disclosure: Long Tesoro.

Start a free 7-day trial of Premium Membership to GuruFocus.

Also check out: