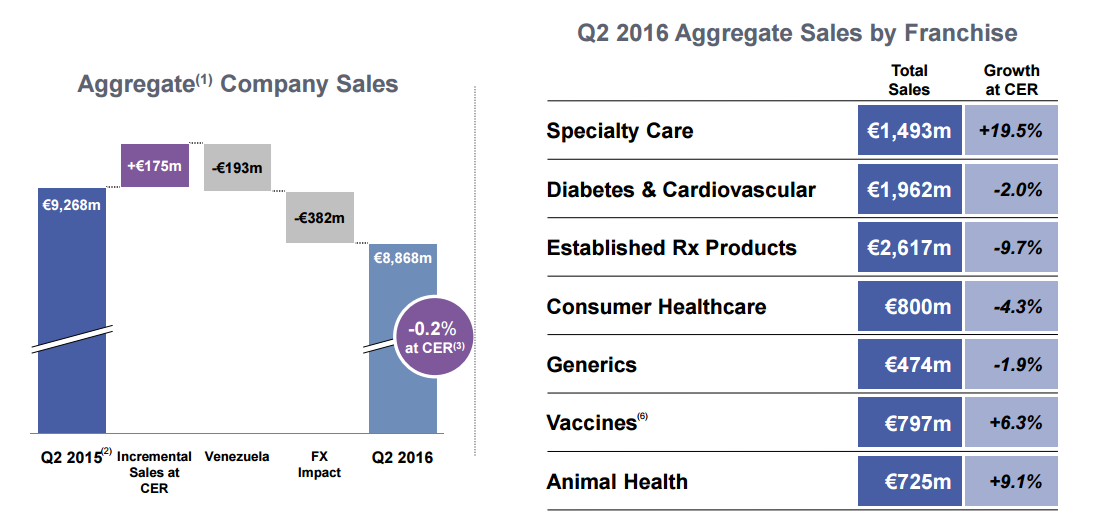

Of the top pharma companies with more than $100 billion valuation, Sanofi (SNY, Financial) is one of the cheapest, trading at 21 times earnings and a lowly 12.3 times forward earnings. Revenue has been flat for the last three years while their stock price followed suit, staying put around the $70 level. Sales decline is yet to stop, with the company reporting a 0.2% decline during the second quarter - the primary reason behind such low valuation for the company.

Segment analysis

Specialty Care, Vaccines and Animal Health segments grew, while Sanofi reported declines in Consumer Health Care, Generics, Established Prescription Products and Diabetics and Cardiovascular segments. The problem for Sanofi is that the company expects its flat growth to continue in 2016, and it has guided for a stable business EPS at constant exchange rate for the year. With the dollar continuing to strengthen against emerging market currencies, Sanofi, which earns a major portion of its revenues from outside the United States, will continue to face currency headwinds.

Sanofi’s pipeline looks reasonably well-positioned with 14 products in late stages and 30 products in phases 1 and 2, but the fact that Sanofi was one of the bidders in the much-hyped buyout of Medivation (MDVN, Financial) makes it amply clear that the company is not expecting blockbusters to keep tumbling out of its pipeline.

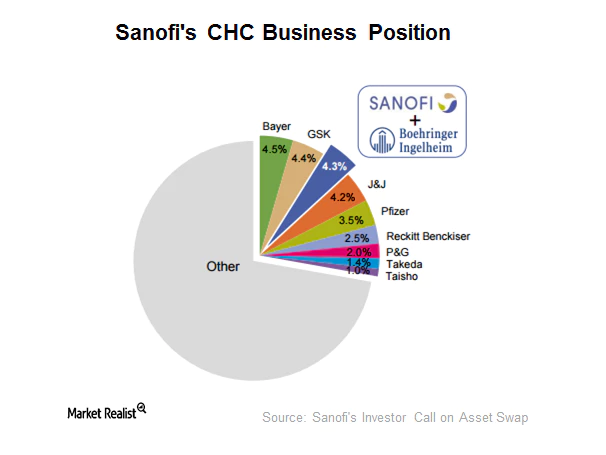

Established Products still account for a major portion of Sanofi’s overall sales and has been declining steadily over the years. Vaccines and Specialty Care are growing, but they are not moving at a pace that can offset the decline from other segments. The company has taken a strategic decision to swap its Animal Health Care unit for Boehringer Ingelheim’s Consumer Health Care (CHC) business. The deal, once complete, will catapult Sanofi to third place in the CHC market, above Johnson & Johnson (JNJ, Financial) and below Bayer (BAYRY, Financial) and GlaxoSmithKline (GSK, Financial).

The $22.8 billion asset swap (the equivalent of $11.4 billion from each party to the deal) has the potential to improve Sanofi’s CHC numbers, while also providing the French pharma major with diversified revenue streams. But the results are not going to come in thick and fast because the segment itself is extremely defensive. At best, the company can expect stable but reasonable growth from this unit. The deal will be accretive to Sanofi’s EPS after 2017.

In the short term, Sanofi will have to bear the pain of growing segments not adequately compensating for Established Prescription Products. Since their best-selling diabetes drug Lantus declined from increased competition, the company hasn’t been able to improve its performance in this segment. Acquisitions and deals such as the Boehringer swap seem to be the only way Sanofi can offset its short-term troubles. The 4.7 billion euros Sanofi will get in gross cash settlements as part of the swap will leave it in a good position to acquire new assets as they present themselves.

What is hurting investor sentiment, however, is the time they have to wait. Once the deal is announced, the forward earnings multiple has only one way to go.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.