After declining through major parts of 2014 and 2015, Qualcomm’s (QCOM, Financial) shares have rebounded by more than 25% in the last twelve months. The slowdown in smartphone sales has greatly affected the company, causing revenues to decline from $26.48 billion in 2014 to $25.28 billion in 2015. But the company managed to arrest the decline during the third quarter of the current fiscal, posting 4% year-over-year growth.

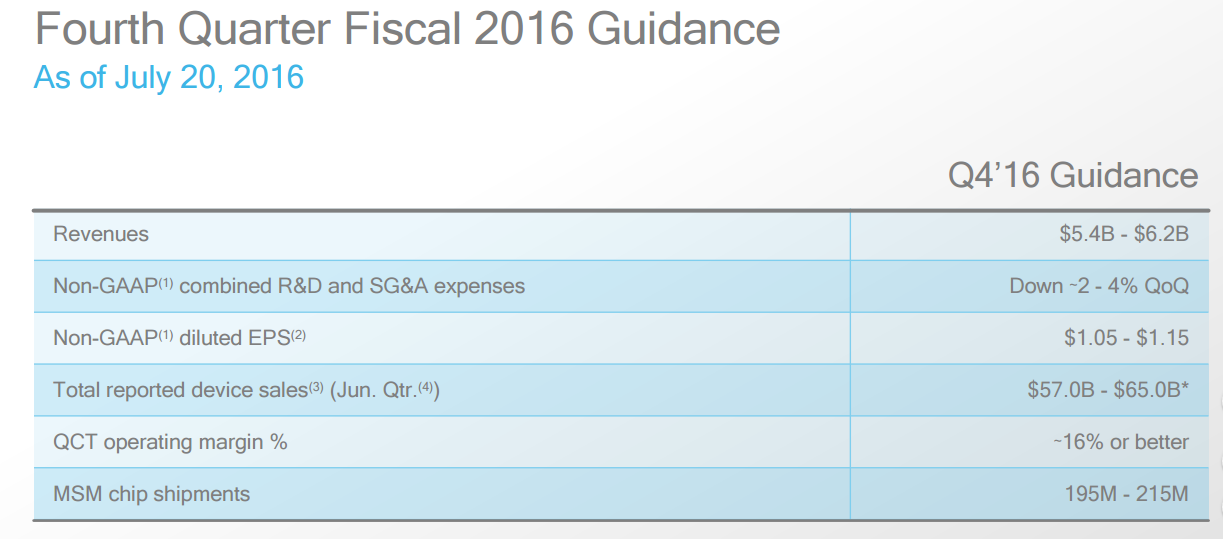

Total sales numbers for the first nine months of the current fiscal are still much lower than what the company made last year due to their underperformance during the first two quarters, but the company seems to be upbeat about its chances during the fourth quarter, guiding for $5.4 billion to $6.2 billion in sales. Qualcomm posted $5.5 billion in sales during the fourth quarter of 2015, which means the company is expected to either meet those numbers or exceed them, posting growth. The news that the company did not project much lower numbers will be a huge relief for the investors who have pushed the company’s stock up by more than 25% since the start of this year.

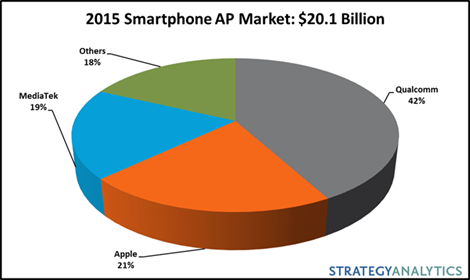

Though things have changed for the better during the second half of the current fiscal, Qualcomm is still facing several issues that it needs to address. Its competition with MediaTek (TPE:2454, Financial) has intensified in the smartphone application processor (Smartphone AP) segment, causing it to lose market share. According to Strategy Analytics, Qualcomm, which is still the leader in the segment, lost 10% in market share to now hold 42%, while MediaTek improved its numbers by 5%. The overall market itself declined in 2015, and losing 10% market share in a declining market is less than ideal.

Source: Strategy Analytics

Qualcomm’s revenues come from three segments: QCT (Qualcomm CDMA Technologies), which sells integrated circuit products and its system software to manufacturers of mobile phones, tablets, laptops and other devices; QTL (Qualcomm Technology Licensing), which grants licenses for a fee to third parties to use the company’s intellectual property portfolio (patents); and QSI (Qualcomm Strategic Initiatives), its investment arm.

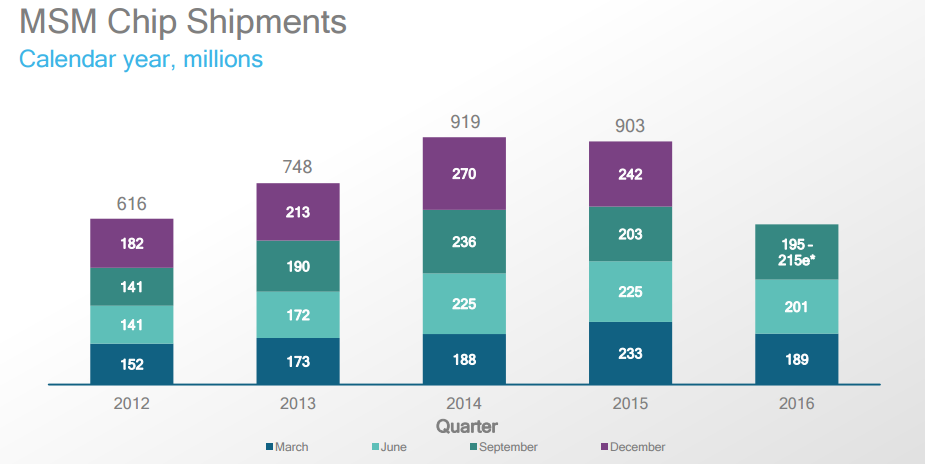

As the leader of the mobile chipset market, Qualcomm’s revenue is invariably tied to the health of smartphone sales around the world, which has been on a slowdown since 2014. Mobile Station Modem (MSM) chipset shipments declined from 919 million in 2014 to 903 million in 2015, and it has declined even further in the first three quarters of this year.

Things are not looking rosy next year either, with Gartner Inc. estimating global smartphone sales will continue its slowdown and will no longer grow in double digits.

“Worldwide smartphone sales are expected to grow 7 percent in 2016 to reach 1.5 billion units. This is down from 14.4 percent growth in 2015. In 2020, smartphone sales are on pace to total 1.9 billion units.” - Gartner

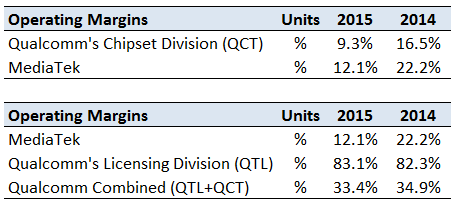

As if the market slowdown were not enough, Taiwan-based MediaTek has been breathing down Qualcomm’s neck. MediaTek’s operating margins are much better than Qualcomm’s, and a shift in sales towards lower margin products and slowdown in China added to the pressure on Qualcomm’s overall margins.

“QCT results of operations in the first nine months of fiscal 2016 were negatively impacted by the effects of a shift in share among our customers within the premium tier, which reduced our sales of integrated Snapdragon processors and skewed our product mix towards lower-margin modem chipsets in this tier, a decline in demand for our thin modem products, a decline in share at a large customer and the competitive environment in China.”

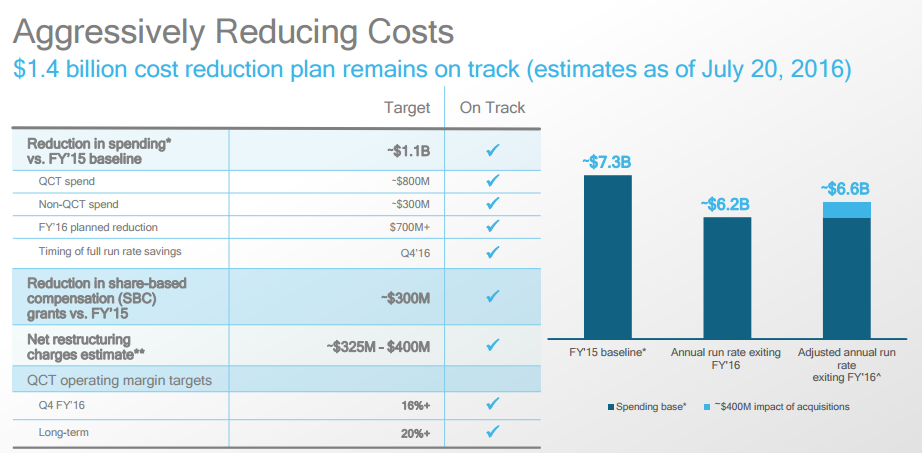

The market is getting increasingly difficult for Qualcomm to navigate. Slowing smartphone sales, rising competition and the shift in product mix are all going to affect the company in the next few years. The company has been aggressively reducing costs, reducing full-time staff and temporary employees, and aims to achieve $1.4 billion in cost reduction.

On the positive side, Snapdragon sales should pick up as several brands ready their early 2017 smartphone launches, including Samsung (SSNLF, Financial) and Google (GOOGL, Financial). In the meantime, Qualcomm needs to push through as best it can and fend off margin pressure by implementing further cost-cutting measures.

Disclosure: I have no position in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.