Verizon’s (VZ, Financial) revenue has been declining since the start of the year, and the current fiscal could be the first time since the recession that the company reports a sales decline. Total operating revenues in the first six months reached $62.7 billion, down 2.3% compared to the $64.20 billion the company reported in the prior period. Verizon had guided 2016 adjusted earnings to be at a level comparable to 2015, excluding the 7 cents per share impact of the work stoppage.

So it's clear that the company is not expecting things to be rosy for the rest of the year. In the second quarter, Verizon reported earnings that beat analyst expectations, but the top line missed Wall Street’s benchmark. Wall Street expected earnings of 92 cents on the back of $30.94 billion while the company came out with earnings of 94 cents on $30.53 billion.

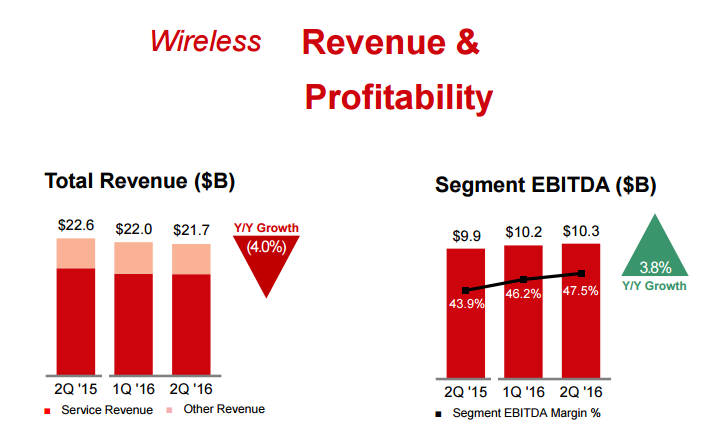

The results of the previous quarter were a bit of a mixed bag for the company, with wireless net additions touching 615,000, taking the total number of connections to 113.2 million, a growth of 3.3%. But revenues from the segment declined by 4% despite EBITDA margin improving by 3.8%. With the bulk of the company’s revenue still coming from this segment, Verizon’s results are completely dependent on its performance here.

For all the top wireless carriers, sales growth is directly proportionate to the number of subscriber adds they make. Unfortunately, that growth will not last for ever. As the U.S. market’s wireless device penetration keeps moving higher and higher, the probability of slower growth increases as well. Verizon is already anticipating that day and is preparing by transforming itself into a major player in the growing digital advertising market, currently led by Google (GOOG, Financial) and Facebook (FB, Financial).

Verizon’s forward P/E of 12 times earnings clearly shows that the market is not expecting the company to report great growth numbers in the next few quarters, and the dividend yield of above 4% just validates the low expectation levels set for the company. Though the content portfolio that has been built on the back of acquisitions seems to be strong with AOL (AOL, Financial) properties and the recently added Yahoo (YHOO, Financial), it will take time for results to filter down to the bottom line.

Nobody is expecting the company to show strong growth in the short term, but of the top two wireless carriers, Verizon is better positioned to handle the next ten years. This is the crucial period when additions to wireless subscriber bases can be stable at best, and tight margins further intensifying the pressure on these companies.

So far, Verizon seems to be the only one fully prepared to tackle that problem.

Disclosure: I have no positions in any of the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.