Netflix (NFLX, Financial) is one of my favorite companies, not just because of the way the company has grown in the last 10 years but more because of the way it was able to adapt to evolving situations. It has incrementally improved its business from being just a rental company that couriered DVDs to the one company that every other video on demand (VOD) service provider keeps looking up to.

As you can see from the chart above, the stock has been extremely volatile, moving sharply with each earnings report depending upon how the subscriber base grew. The results have been mixed so far this year with the company missing its own targets in the second quarter and doing better than expected in the third. But what is evident is that the company’s valuation is extremely dependent on one number: the user base added during the most recently reported quarter. And there’s a valid reason for that.

For a video on demand service provider like Netflix, sales growth is directly proportional to the number of users the company added during the given period. Netflix already has a sizable presence in the U.S., and growth will be a bit slow in its home market due to high penetration levels. To counter the slowdown the company has been forced to move at a rapid pace, expanding its network to nearly 190 countries in a short span of time.

In a way, Netflix does have a lead over other providers within the U.S. as well as outside. The company has been reducing its licensed content library as it increases its focus on building its own content base. As a company with worldwide reach, the licensing route is not something on which the company wants to depend. And there is the added benefit of standing out from the crowd when you create your own content. Netflix has the money, so by reinvesting in a time-consuming and cost-intensive production process, the company wants to take the risk while it can and create a gulf between itself and its competitors.

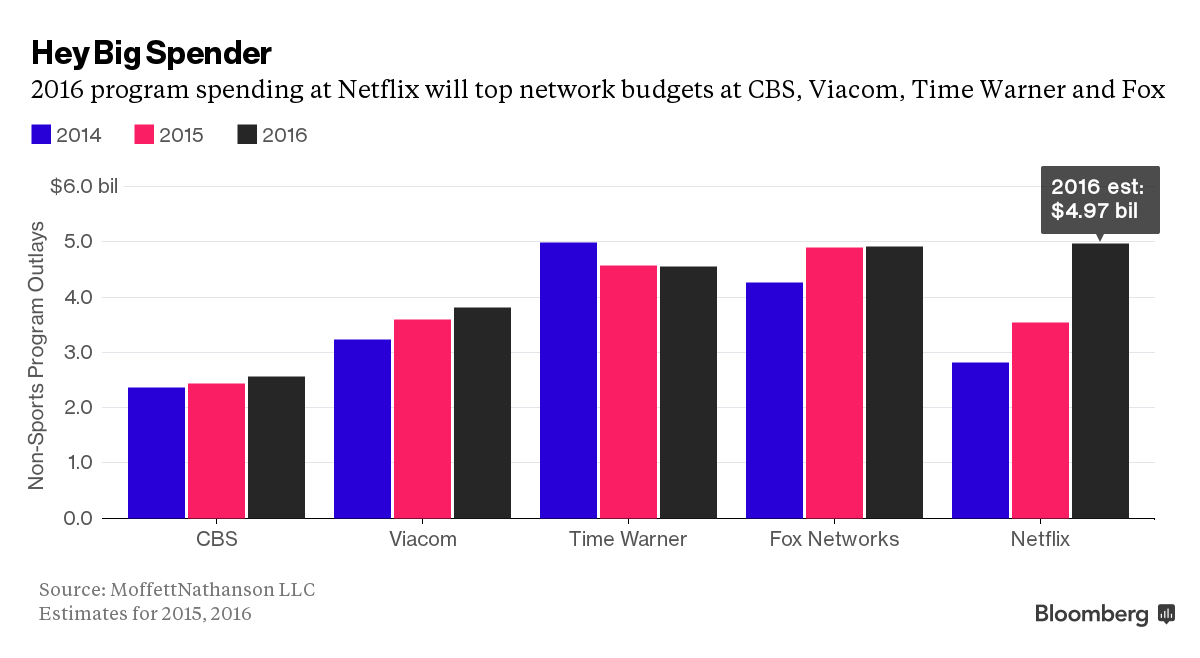

Looking at the number of hit shows the company has been able to churn out in a short period, it’s obvious that Netflix will be able to deliver on that promise of owned content. Netflix’s spending has already crossed big-ticket spender Time Warner Inc. (TWX, Financial) this year, and the company is only going to increase it over the years as its subscription base keeps growing at home and around the world.

Netflix crossed $2 billion in quarterly revenue during the second quarter of this fiscal, and the company should lock in somewhere in the $7 billion to $7.5 billion range for the current year. With long-term debt of $2.373 billion at the end of the third quarter and a cash position of $969 million, the balance sheet has enough strength to support its content investment spree. With quarterly revenues already above $2 billion, content investments can and will accelerate, and the more this increases, the gap between Netflix and its fellow competitors is only going to increase.

Netflix’s scale has possibly reached a point where it can help the company immensely. For companies like Apple (AAPL, Financial) and Amazon (AMZN, Financial), Video on demand is a crucial part of their business and they have a lot of money, but it will never be the product on which their lives depend the way it is for Netflix. Whatever money Netflix earns and whatever strength it has is only going to be funneled toward its one single product, which is delivering video on demand in whatever way it can to its hungry masses, and this is exactly what is going to make Netflix stay at the top of the pile.

It is the gazelle running for its life while the others are the cheetah running for its next meal.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.