Salesforce (CRM, Financial) is one of the earliest proponents of the pay-as-you-go model in the software industry. The best part is it proved that even at the enterprise level there is huge demand for the as-a-service model, which has now become the most preferred mode of sales for software companies.

As a niche player in the customer relationship management segment with a unique business model, Salesforce was able to grow at an extremely fast clip, trouncing big enterprise players such as Oracle (ORCL, Financial) and SAP (SAP, Financial) to take the numero uno position in its niche – and also hold on to its position for such a long time.

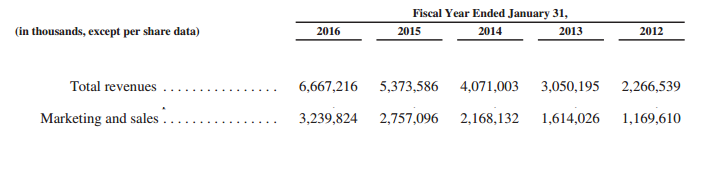

Revenue has grown more than tenfold in the last 10 years, moving from $497 million in 2007 to $6.667 billion in 2016. But throughout this double-digit growth decade Salesforce has remained an unprofitable company, spending nearly half of its revenues in marketing and sales – extremely high by any standards. The problem is that these high customer acquisition costs have continued unabated for many years, even when the size and scale that Salesforce achieved over that period would normally have allowed any other company to finally ditch that growth strategy.

Customer acquisition costs will inevitably be high if there is intense competition in the market. And when the market size potentially gets smaller with each acquisition – as is the case with smaller players with limited market share potential – then acquiring that next customer becomes that much harder than the previous one.

While this position might be more acceptable from a smaller company trying to break into a tough market, the same can’t be said for Salesforce, which has been the No. 1 player for a long time. Despite that, Salesforce has been unable – or unwilling, as the case may be – to bring its sales and marketing expenses under control.

The good news for the company is that it has been able to maintain its prolific growth rate for many years and could well continue the trend in the near future. Oracle is a clear and near-term threat eyeing the CRM and HCM (Human Capital Management) markets, as well as the SaaS market as a whole. The main reason for acquiring Netsuite was to bolster its credentials in the business management as a service market, where Salesforce currently rules the roost.

Microsoft (MSFT, Financial) is a long-term threat, as the company is also eyeing the enterprise software market to boost its own revenues by selling SaaS products. Microsoft is taking the "we have the best bundle for enterprise companies" route, and with Office 365 and Microsoft Azure they already have a potent combination that is extremely useful for enterprise-level companies operating in multiple locations around the world.

Microsoft is also beefing up its Microsoft Dynamics software to gain a foothold in the business management software segment. To prove a point, the company recently snapped up HP Inc. (HPQ, Financial), a long term customer of Salesforce, and added it to its client list.

Competition is only going to increase in this market, making things more difficult for Salesforce to keep up the momentum as it enters the $10 billion-plus league. Its products are top notch, and that provides validation of the company’s current position in the business management SaaS space, but it does not give it immunity from the multipronged attack being launched by Oracle, Microsoft and the rest.

This competitive landscape could slow Salesforce down in the coming years so it’s no surprise the company is supporting its organic growth with an acquisition spree this year. Will that be enough to help it keep the other sharks at bay? It appears we will have to watch developments in this domain closely to see exactly how it will pan out.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.