As the U.S. retail industry continues to be shaken up by the growth of online retail, the bigger and stronger retailers will be the last ones standing as smaller ones struggle due to sustained competition at the top.

In a recent article, I picked Wal-Mart (WMT, Financial), Costco (COST, Financial) and Amazon (AMZN, Financial) as the three retailers that will stand out from the crowd due to their differentiated offerings, size and scale. Kroger (KR, Financial) is another company that might be the dark horse in the future retail race. From the current valuation perspective, Kroger looks much cheaper compared to the other three.

Grocery is one of the strongest points of Kroger. The company has more than 2,796 grocery retail stores spread across 35 states operating under two dozen banners. The company also has 787 convenience stores and is investing quite heavily in technology as well. That footprint, coupled with its robust grocery retail operations, provides Kroger with plenty of room to take on any sort of competition in the next five years.

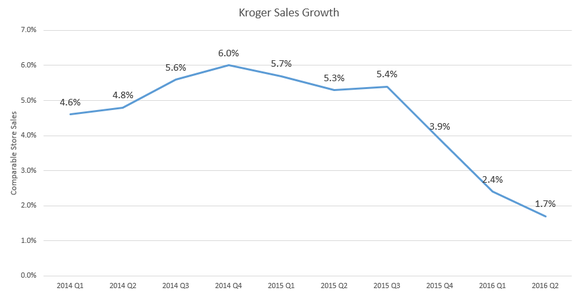

Kroger’s stock price has declined by nearly 15% in the last 12 months due to the gradual decline in same-store sales growth over the last year or so. Nevertheless, Kroger’s same-store sales have grown for 51 consecutive quarters, which is impressive considering the state of the market during the last four quarters of that period.

What makes this prolonged growth so sweet is that it came despite the company growing at a fast pace through acquisitions. It is not an easy job to take over company after company and still keep your same-store sales moving, as things can easily go wrong. But fortunately for Kroger, this inorganic growth strategy has paid off big time.

Â

And yet, the stock price kept edging lower during the year due to the slowdown in same-store sales growth in the last five quarters. Kroger also adjusted its full year outlook downwards, adding more pressure to the stock.

“Kroger narrowed its net earnings guidance range for fiscal 2016 to $2.03 to $2.08 per diluted share for 2016. The previous guidance range was $2.03 to $2.13.” - CNBC

The U.S. market has been on a deflationary path for a really long time, which has started to hurt big retailers.

Kroger now expects slightly positive or identical same-store sales growth during the fourth quarter, excluding fuel. The company blamed persistent deflation for its not-so-rosy outlook.

“As expected, deflation persisted during the third quarter," Rodney McMullen, Kroger's CEO, said during the third quarter call. "And as we’ve said before, transition periods create a difficult operating environment. This is the third time we’ve had deflation in 30 years; and in previous instances, deflation lasted from three to five quarters in a row. We’re in the middle of the cycle right now, and it’s not fun, still our tonnage continues to grow, our total market share continues to expand, and we’re focused on executing our strategy.”

Continued deflation in the market and the slowdown in same-store sales growth has caused the stock price to edge lower and lower throughout the year. The stock is now trading around 16 times earnings and at 0.3 times sales, much lower than Wal-Mart, Costco or Amazon. Considering the current price point and the amount of room Kroger has to grow - mostly via acquisitions - the stock is an attractive investment with a huge margin of safety.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.