Microsoft (MSFT, Financial) stock has surged by more than 25% in one year and is now trading closer to its 52-week high. The stock does look a bit expensive at 30 times earnings and nearly six times sales. A closer look at Microsoft’s revenue streams may reveal why the company is commanding such high valuations.

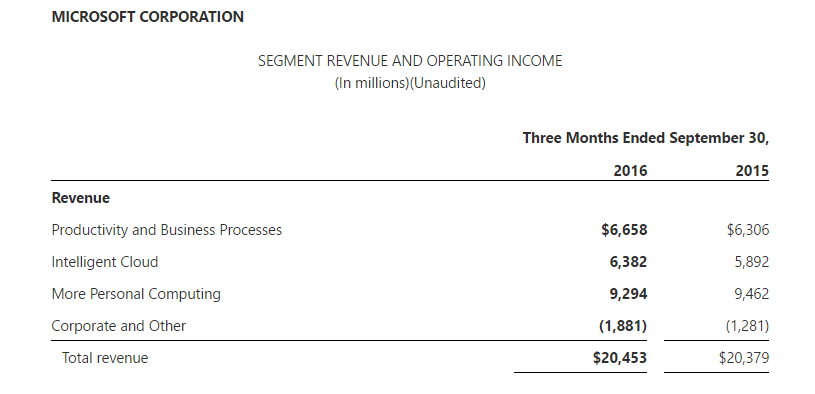

The biggest problem Microsoft faces - and one that it is furiously working to solve - is its Windows-dependent revenue streams. Microsoft changed its financial reporting segments two years ago and we do not know exactly how much money now comes from Windows. The fact that it is now buried under a pile of gaming, search advertising and devices certainly does not help, nor does the non-self-explanatory segment title of More Personal Computing.

Common sense and a little knowledge of Microsoft’s past suggests the bulk of MPC revenues must be coming from Windows. Further, the fact this segment posted a revenue decline for first-quarter 2017 indicates this segment is in trouble. Revenue growth from Windows OEM and Windows commercial products and services was flat during the quarter compared to the prior period.

This is happening along with a trend of declining PC shipments worldwide for the past five consecutive years. If Gartner is correct, it will remain flat for another five years.

It may be hard to accurately predict when the decline will stop, but it is easy to predict the market for Windows on PCs is shrinking.

The new Microsoft, however, is not sitting around waiting for the inevitable, like a lot of other companies did before they realized they needed to make a U-turn. Instead, it built a strong foundation and enviable position in the cloud industry through its cloud infrastructure (IaaS) and multiple cloud software (SaaS) products.

That effort is ongoing, with Dynamics 365 now in the fray battling alongside Office 365 against other SaaS giants like Salesforce (CRM, Financial), SAP (SAP, Financial) and Oracle (ORCL, Financial). There are billions of dollars worth of potential in SaaS subsegments like customer relationship management and enterprise resource planning. To Microsoft, it represents a way out of its Windows predicament.

From the most recent quarterly report, we know Microsoft is now able to offset its core losses with gains from forward-looking businesses. SaaS products and Microsoft Azure are the two segments that are going to drive future revenue streams. That is also why I believe Microsoft put them in different segments - Productivity and Business Processes and Intelligent Cloud. That way, investors get to see Microsoft’s better side while being distracted from looking too closely at More Personal Computing.

In any case, these two areas of focus are extremely forward-looking and will keep expanding Microsoft’s revenue streams for several years, if not decades.

Microsoft’s commercial cloud annualized revenue has now exceeded $13 billion and the company has now set its sights on $20 billion annually by 2020 - a target that is well within reach.

At six time sales, Microsoft looks expensive, but the growth prospects coupled with a clear direction for the future are unmistakably attractive.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.