United Parcel Service’s (UPS, Financial)Â fourth-quarter earnings came in below expectations, causing the stock to decline sharply after the earnings release.

The underperformance and the resultant stock decline is possibly the best thing that happened to investors who are looking to add the stock to their portfolios because the reason UPS missed earnings was the sharp surge in business-to-consumer (B2C) goods, fueled by e-commerce.

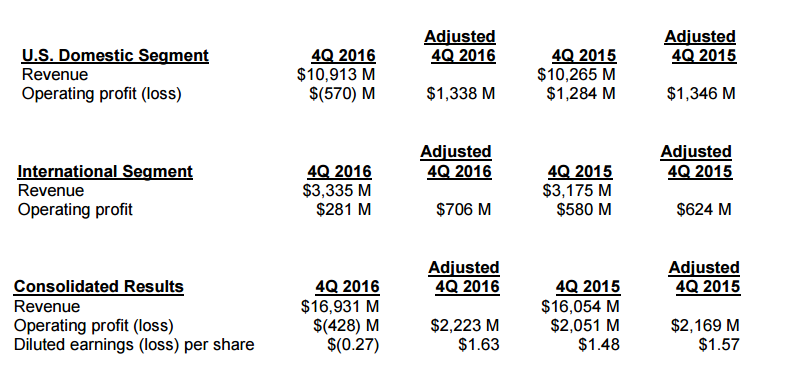

UPS reported earnings per share of $1.63 with revenues of $16.9 billion, both top line as well as bottom line coming in below Wall Street expectations of $1.69 earnings per share and $17 billion in revenues for the fourth quarter.

During the earnings call UPS management went into considerable detail about the strong uptick in business-to-consumer goods volume and how it impacted its overall numbers. UPS delivered 712 million packages globally during the quarter, a 12% increase over last year’s numbers. Clearly, volume was up in double digits but domestic adjusted operating profit after excluding pension-related charges inched lower, which means it shipped a lot more lower-revenue products this year compared to last year.

- "Strong market demand for our e-commerce solutions created a significant shift in product mix during the quarter.

- "B2C shipments grew at 11.5%. We reached a number of historic levels during the quarter, including 55% B2C, the largest volume increase in a quarter and the highest month ever at 63% B2C in December.

- "On the commercial delivery side of the business, B2B shipments were down slightly." – UPS Fourth-Quarter Earnings Call

It’s clear which way the mix is headed. B2C deliveries are inherently more expensive because they involve last-mile deliveries to multiple destination points, each bringing only a sliver of a margin. While the sudden surge in B2C pushed U.S. domestic revenues up to $648 million (6.3% year over year), it led to adjusted operating profits of $1.338 billion for the quarter compared to $1.346 billion in profits in the year-ago period.

Margins are going to get tighter for UPS as e-commerce pushes the volume to higher levels. This quarter was a shock for the company in terms of operating numbers, which will inevitably lead to closer scrutiny of how it is going to handle this steady increase in B2C shipments.

The more this segment grows, the higher the need for established, well-networked shippers like UPS. However, there is no way UPS will continue to allow U.S. domestic numbers to keep bleeding at the operating level.

As it stands, UPS will either try to improve its numbers through efficiency initiatives or gradually pass on the cost to its B2C consignors.

UPS has a positive forecast for 2017. The company expects adjusted diluted full-year earnings in the $5.80 to $6.10 range, a small uptick against the adjusted diluted 2016 EPS of $5.75. Not really a path-breaking number, but it does show that the company expects margins to stabilize even in the face of strong e-commerce-fueled B2C shipping growth.

“2017, the global economic outlook remains generally positive, and forecasts have risen modestly over the last few months. In the U.S., GDP growth for 2017 is forecast to be slightly higher than last year. The expansion of e-commerce is expected to continue with another year of double-digit growth. On the commercial side of the economy, industrial production outlook has gone from negative to slightly positive. That favorable move is a good sign for the manufacturing sector.” – UPS

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.