Starbucks (SBUX, Financial) has lost a lot of shine this year.

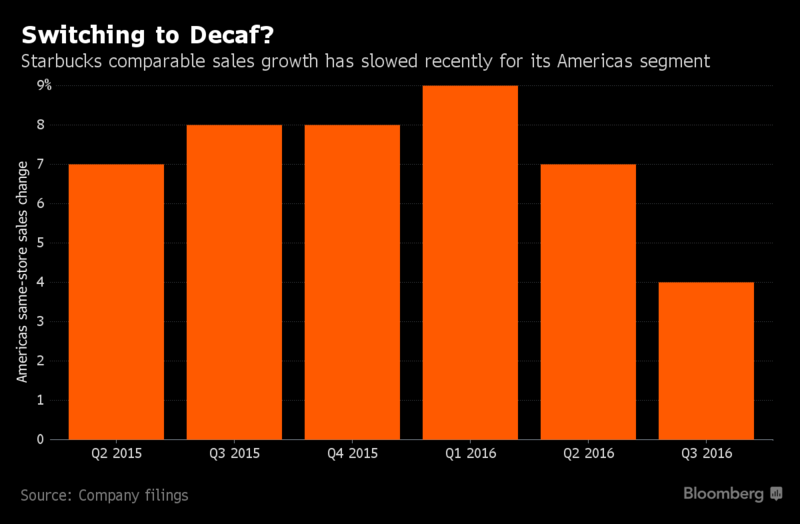

The stock price kept moving sideways as the world’s largest premium coffeehouse chain struggled under the weight of its own past performance. Comparable store sales in the U.S. came in at below 5% last year after staying above the 7% mark for a long time. The company kept saying that the drop in the third quarter was an anomaly; unfortunately, it wasn’t.

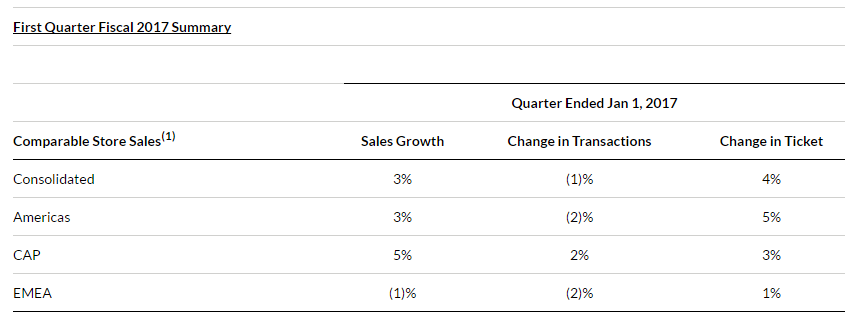

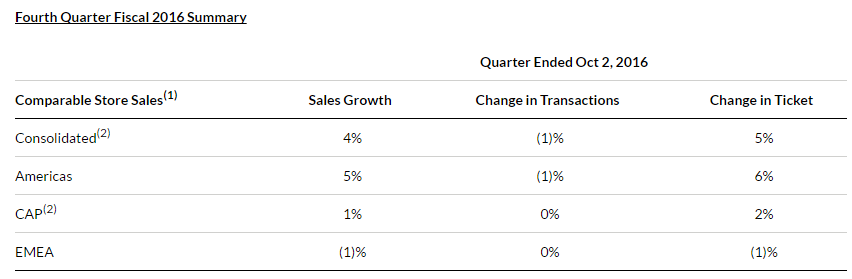

Starbucks' same-store sales in the U.S. during the recently ended quarter (first-quarter 2017) expanded by 3%; during the fourth quarter of 2016, it moved up by 5%.

Though the numbers might not look bad on the surface, the primary reason for growth during the last two quarters was the increase in ticket, which means same-store sales grew because Starbucks increased its prices, and not because more people walked in or ordered more. It’s normal for companies to pass on some of the cost increases to their customers. Besides, as a premium coffeehouse chain, Starbucks does have enough bandwidth to pass on costs. But the problem is ticket increase can only help for some time as it is not a sustainable way to increase same-store sales for prolonged periods.

What about future growth?

Starbucks has been rapidly expanding in overseas markets, and it will continue to do so in the future. But for now, Starbucks is dependent on the U.S. market for its revenues. During the recently concluded quarter Starbucks brought in $3.99 billion in revenues from its Americas segment, accounting for nearly 70% of total revenues. Starbucks’ company-operated stores in the Americas are the real engine behind the company, recording $3.561 billion sales in first-quarter 2016, nearly 61% of total revenues.

Implementing a brisk pace of new store additions, Starbucks added 307 net new stores in the Americas during fourth-quarter 2016, and 251 during first-quarter 2017. Revenue growth definitely has the right support systems under it, but if the contraction in U.S. transactions persists, it will slow things down for the company.

According to Starbucks’ five-year plan the company wants to add another 12,000 stores to its list by 2021. During the recent quarter the company added 690 stores so a 12,000 target in five years time is a bit difficult, but not impossible. It will still be a major achievement even if it gets close to it.

As a long-term investment Starbucks makes a lot of sense because it does stand out from the crowd. The premium segment positioning allows the company to expand to country after country.

But in the short term, U.S. pain could intensify if the company doesn’t turn things around. The stock has been extremely weak due to that, moving up by less than 3% in the last 12 months. If the next quarter comps in the U.S. come in lower than first-quarter numbers, then it may even start moving lower, opening up the best window for investors to load up.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.