Microsoft Corp. (MSFT, Financial) has been on a steady march towards revenue growth as the company has smartly turned its focus toward multiple product lines and cloud, while slowly pushing Windows to the back burner. The technology giant has created a solid portfolio of products that it sells using the as-a-service cloud-delivered model.

The company’s push into the enterprise software segment is built around Office 365, which is part of the Productivity and Business Processes segment. Although we do not exactly know how much its IaaS offering Azure brings in, recent estimates suggest it could be around $2.7 billion dollars in 2016. If that assumption is true, then a large bulk of its cloud revenue is coming from SaaS products because the annualized commercial cloud run rate crossed $14 billion during the most recent quarter.

Considering the rate at which Office 365 has been growing, it is not really a surprise that the SaaS lineup is bringing in revenues in the billions. Office 365 commercial revenue has been growing above 50% for the past several quarters, with the latest quarter growth coming in at 47%. Dynamics 365, Microsoft’s product to address the growing ERP and CRM segment, also witnessed 9% revenue growth during the second quarter.

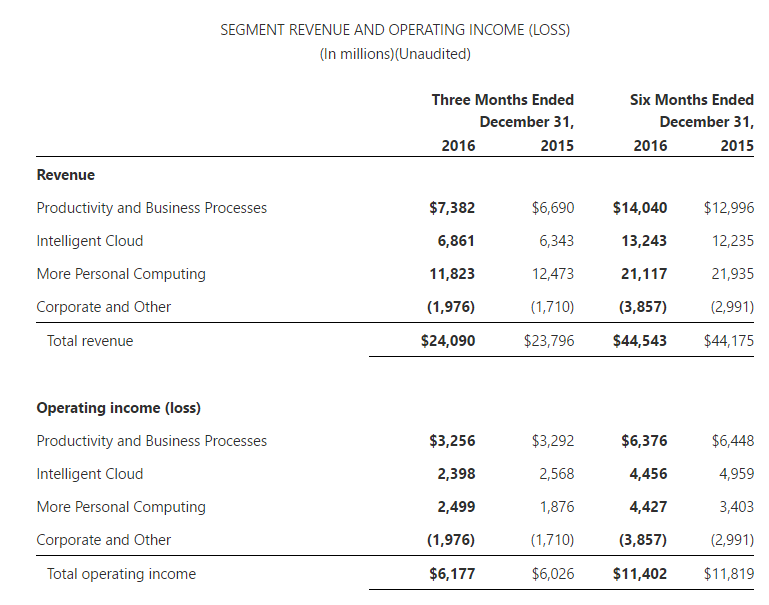

Revenue from Productivity and Business Processes grew 10% during the second quarter to reach $7.4 billion. More than the revenue growth rate, Microsoft’s management must be extremely happy with the margin levels offered by the productivity segment. During the second quarter, the segment reported an operating income of $3.256 billion with an eye-popping margin of 44.10%, while the margin for the first two quarters was 45.41%.

Source: Microsoft Q2-17 Press Release

The software segment is inherently a high-margin business, but above 40% margins is not something you come across often. It shows the pricing power Microsoft has and is a clear sign it is at the top of the segment. Even if the competition were to catch up to it, Microsoft has plenty of room to move in the event of a price war.

Microsoft’s SaaS office collaboration products are possibly in the same position as Amazon (AMZN, Financial) Web Services’ products in the IaaS world - way ahead of the rest of the pack.

Office 365 and AWS both have the size and scale of multibillion-dollar businesses, but they still keep adding service after service to their offerings, making it extremely difficult for the competition to enter the market, let alone play catch-up.

It is not easy to drag either unit into a price war because they both enjoy the fattest margins possible. Moreover, it is not easy to create a better product because they are relentless in expanding existing functionality and enhancing performance, all while continuously keeping a finger on the pulse of pricing.

Both companies have no reason to slow down and should continue to enjoy robust growth in their respective segments. One has a very strong enterprise productivity business, while the other has a fast-growing IaaS unit.

If you are watching Microsoft and Amazon, these two segments should get as much attention from you as their core businesses of software and retail.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.