McDonald’s Corp. (MCD, Financial), the world’s largest restaurant chain with more than 35,000 stores across the globe, turned things around in 2016. After watching its comparable stores sales decline quarter after quarter in 2015, the company reported global comparable store sales growth of 3.8% in 2016.

McDonald's made several strategic decisions, which included introducing its all-day-breakfast program, in-store mobile ordering and enhancing its digital capabilities. In additon, the company decided to cut down on risk by reducing the number of company-owned stores while increasing franchisee stores.

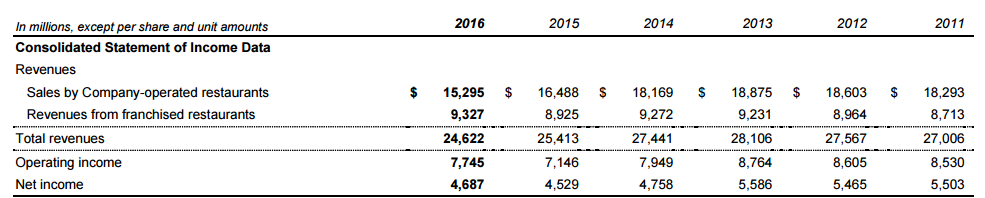

The fast-food chain is planning to move toward a franchise-heavy model, targeting 95% franchised restaurants and 5% company-owned stores. This move will reduce revenues in the long run, but also reduce capital expenses and increase operating margins. During 2016, McDonald's reported $15.295 billion in revenue from company-owned restaurants and $9.32 billion from franchised restaurants.

At the end of 2016, McDonald's had 5,669 company-operated restaurants and 31,230 franchised restaurants. Company-owned restaurants accounted for nearly 15% of system-wide restaurants, which means McDonald's will have to transfer another 35,00 to 4,000 company-owned units to franchisees. Revenue will decline while operating margins slowly improve over time.

The problem for McDonald's is the transition is going to take some time, but the stock has already gone past 20 times earnings. Due to the franchise-heavy nature of its business plan, revenue growth is going to be slow, which, in turn, will also slow down stock price appreciation. But that is the tradeoff that occurs when shifting to a franchise-heavy model where company revenue is based on the one-time fee new franchisee’s pay in addition to a percentage of monthly sales.

Although McDonald’s overall income levels will be steady with this model, the company may no longer be an ideal fit for investors looking for capital appreciation. But for investors who are looking for stable dividend income, a franchise-heavy McDonald's will be an ideal fit. The dividend yield at the time of writing was 2.84%, which is attractive.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.