Procter & Gamble (PG, Financial) has long been the darling of dividend investors, but many things have changed in the past five years. The company suffered massive setbacks as volumes continued to decline, and P&G decided to restructure itself, selling several brands while holding on to what it considered as products that had better growth prospects and better margins.

And that brings us to a common error in judgment when it comes to dividend investing. One of the key factors that is always overlooked by dividend investors is the company’s ability to grow its revenue in the future, not just this year and the next but for this decade and many more decades if possible.

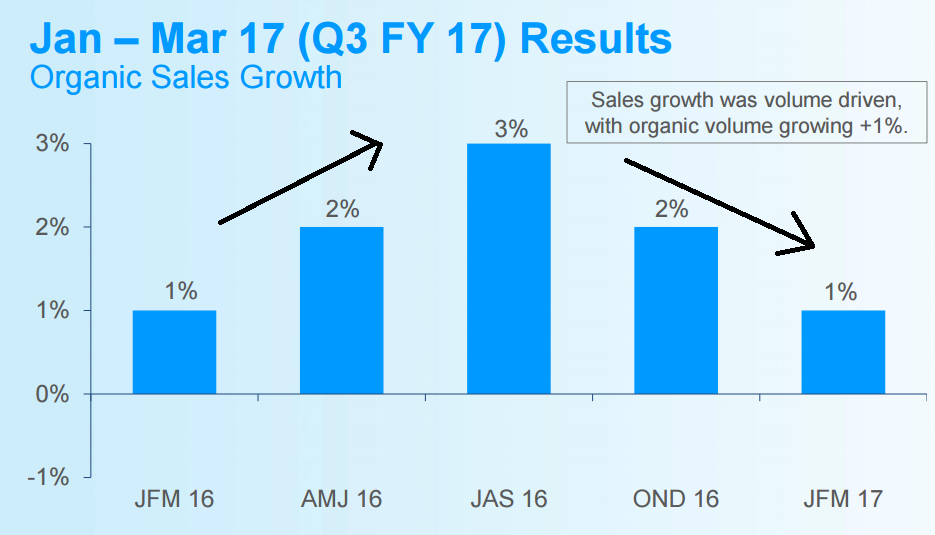

P&G’s sales have been coming down for the past five years, and with the the company selling off several brands in the past, sales growth is inevitably going to come down. On the positive side, the restructuring is nearly complete.

- P&G has sold off more than 100 noncore brands since 2014 in a bid to refocus its business behind roughly 65 labels competing in 10 product categories.

- Last fall, P&G completed the split off with 41 beauty brands that were immediately merged with New York-based Coty (COTY, Financial), the maker of Rimmel makeup and Calvin Klein perfume.

- Also last year, P&G sold the Duracell batteries business to Warren Buffett (Trades, Portfolio)'s Berkshire Hathaway (BRK.A, Financial)(BRK.B, Financial). In 2014, P&G sold its Iams and other pet food businesses to Mars Inc.

- Those three major transactions removed nearly 14,000 workers from P&G's payroll and 23 factories from the company's production pipeline. – USA Today

That said, the selling of brands cannot continue forever, and the company has already reached the stage where the brands it is holding on to have started to show results on paper. The question is: where can P&G go from here? Will the company be able to grow its revenues at a steady enough pace that it can afford to keep increasing dividends in the future?

Unfortunately, things haven’t really gone as per plan for the world’s largest consumer goods company. During the last three quarters, net sales dropped to $48.979 billion compared to $49.197 billion last year while operating profits improved slightly to $11.006 billion compared to $10.939 billion last year. But considering the volume of products the company decided to move, one would expect the numbers to be much better.

But the real problem for dividend investors is the lack of sales growth, and organic sales growth has to break out of the current downward trend as soon as possible. At the end of the third quarter P&G had $14.32 billion in cash and securities while long-term debt stood at $16.6 billion. P&G paid $5.4 billion as dividends to shareholders during the third quarter, more than half of its operating cash flow of $9.06 billion while capital expenditure was $2.2 billion.

Adjusted free cash flow, which is operating cash flow less capital expenditures and excluding tax payments related to the sale of the Beauty Brands, was $7.0 billion during the quarter. P&G is still walking a tight rope when it comes to dividends. As long as sales remain under pressure, the company does not have much room to let its dividends grow at a rate that investors have been used to in the past.

If you are a dividend investor, it will be better to wait and watch P&G for some more time before making a decision to jump in.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Also check out: (Free Trial)