The transportation and logistics segment is one of the least prone to disruption, thanks to the capital-intensive nature of the business. Fueled by the growth of e-commerce, the logistics business has never been more relevant, despite being one of the oldest industries created by man.

There are several players in the market, but large players like United Parcel Service (UPS, Financial), DHL and FedEx (FDX, Financial) control the market, and it is difficult for a new player to rise above and compete with established players, simply because building the kind of logistics network the bigger players have built over the years is not an easy job. Ironically, unless you have that kind of reach and scale you will never be able to match the pricing of bigger players; and if you are not able to match their pricing and speed of delivery, then your business is never going to be able to compete with them on an even scale.

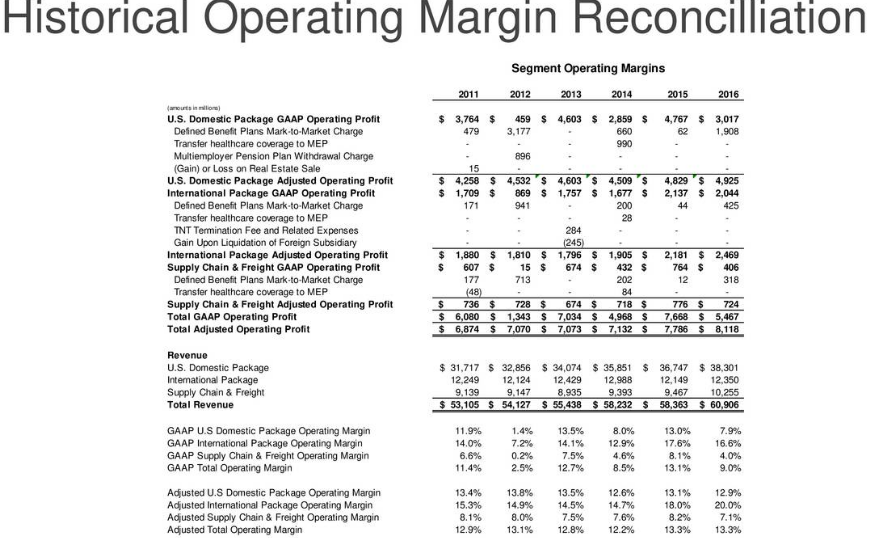

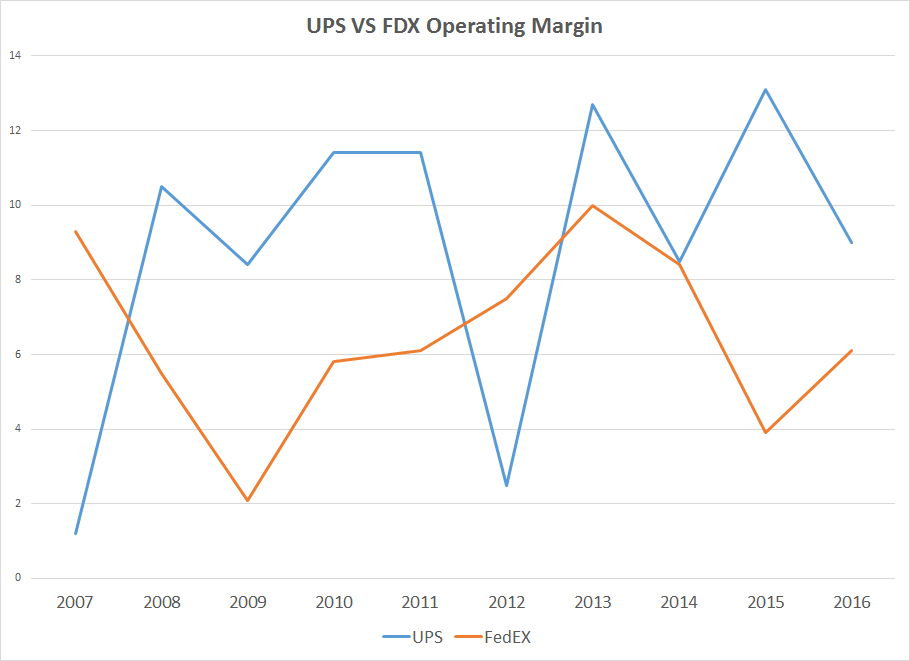

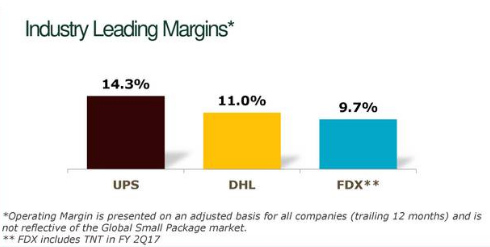

The 109-year-old United Parcel Service is the largest package delivery company in the world, shipping 4.9 billion packages in 2016, an average of 19.1 million pieces per day. In addition to industry-leading volumes, United Parcel Service has always had better operating numbers than its competitors. United Parcel Service's adjusted operating margin has been almost consistently in the 12% to 13% range for the last five years while FedEx and DHL struggle to get close to double digits.

Source: UPS Wolfe Research Global Transportation Conference Presentation

Source: Morningstar

The above-average profit margins have been the hallmark of United Parcel Service as the company keeps pushing in multiple directions to keep them as high as possible. Continuous capital investment to improve its network capacity, automation and technology – all of these are contributing factors.

Source: UPS Wolfe Research Global Transportation Conference Presentation

UPS also completed the deployment of ORION (On Road Integrated Optimization and Navigation system), which aims to create optimal delivery routes, reducing unwanted trips and thus decreasing overall costs.

“ORION employs advanced algorithms to determine the optimal route for each delivery while meeting service commitments. Despite continuing growth in package volume and delivery stops, ORION is helping bend the cost curve by limiting miles driven, which results in fuel and productivity savings. For instance, average daily volume and delivery stops increased 4.1% and 4.4% in our U.S. domestic package operations in 2016 while average daily package miles driven only increased 0.2%.” – UPS Annual Report 2016

Although the larger players will all have their space in the fast-growing logistics market, UPS – with high volumes and above-average operational results – stands to benefit the most. Its operational efficiency will also allow the company to undercut the competition on the pricing front and offer better deals to large customers. It’s not really a surprise that UPS trades around 1.5 times sales – much higher than FedEx’s 0.96 – but if you are in for the long term, UPS is still the better opportunity. You will not find a company like UPS with a 3.1% dividend yield very often.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.