United Parcel Service (UPS, Financial), one of the world’s largest logistics companies, continues to be undervalued by the market, making it one of the best bargains at the current price point. Despite showing its ability to steadily increase its revenues over the last few decades, UPS trades around 18 times earnings and 1.5 times sales.

Annual revenues have grown from $45.49 billion in 2009 to $60.90 billion in 2016. The logistics industry is not a fashionable one, and considering the size and scale of players like UPS and FedEx (FDX), growth has been slow but extremely steady in the last decade. During the first six months of the current fiscal, UPS reported revenues of $31.065 billion, equating to a growth rate of 6.9%, only to see the stock price decline by 2.7% since the start of the year.

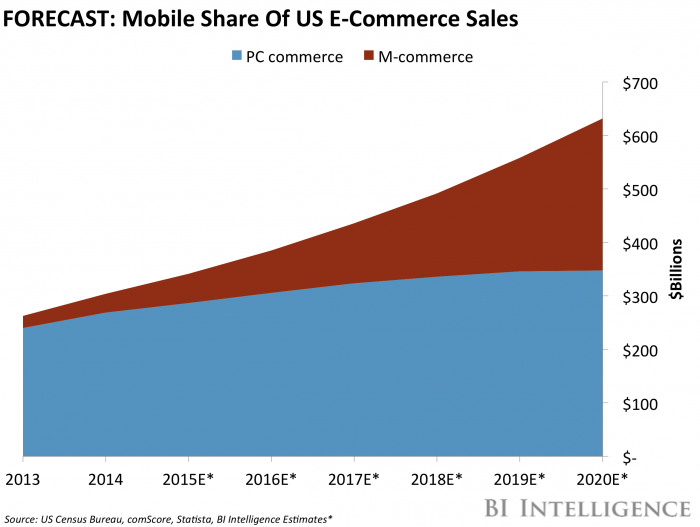

The growth of e-commerce has breathed new life into the age-old shipping industry. With every major retailer in the U.S. doing its best to improve its online sales to stay alive, e-commerce sales will only pick up speed over the next decade, making the services of UPS and FedEx extremely important and valuable.

E-commerce has grown at a very fast clip in the last five years, but it still accounts for only a small percentage of overall retail sales in the country. According to the US Census Bureau, e-commerce sales during the first quarter of 2017 totaled $105.7 billion, accounting for a mere 8.5% of total retail sales in the country. The National Retail Federation is expecting the e-commerce segment to growth in the 8% to 12% range in 2017, and continue such growth through 2020.

The way all the top retailers are competing against each other in the online front will, itself, keep pushing e-commerce sales to higher levels, thus providing steady demand for the services of players like UPS.

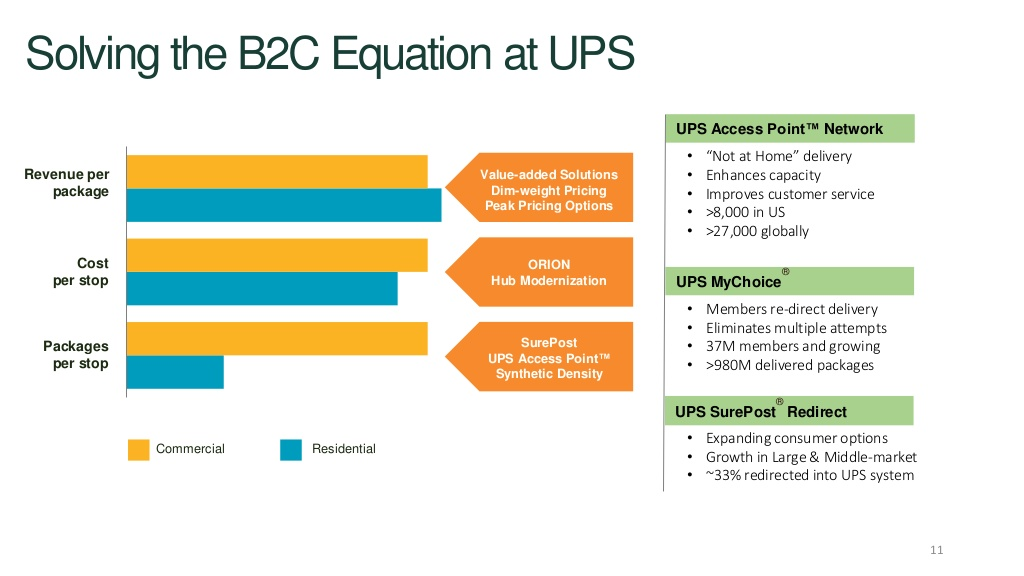

Source: UPS Presentation

UPS expects business-to-consumer (B2C) shipments to steadily rise in the next two years, and the company has been constantly improving its capacity to address that need. The retail industry has no choice but to use UPS and FedEx to take care of their shipping because the low-margin nature of the retail business and the high competition gives them no room to take care of the shipping part on their own.

The path for revenue growth is extremely clear and extremely long for UPS. But, for some reason, the market refuses to acknowledge the amount of future demand that UPS can generate. UPS’s current dividend yield, which is around 3%, makes it one of the best bargain investments that you can buy and hold forever.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.