Bill Gross commented on the drop in equity markets yesterday. The legendary bond guru had quite an interesting take on the “turmoil” and didn’t ascribe as much weight to the $50 billion to $60 billion of tariffs the administration wants to slap on Chinese imports as the financial media.

Gross opined that a trade war certainly wasn’t good for economic growth and inflation. It surprised him that the bond market primarily responded to expected slower growth while it disregarded expected higher inflation. In his eyes those are a push.

Fed Chair Powell left the impression of favoring a pragmatic instead of academic approach. The Fed is going to decide on a meeting-to-meeting basis what to do. Gross also pointed out and believes it is important he doesn’t follow models as much. The former Fed chairs took a 30 to 40-year look at an economy that doesn’t exist anymore.

Historical evidence would suggest a neutral Fed funds rate of 2% (it is at 1.42%; see graph below). If unemployment goes lower, but there is no inflation, look for the 10-year at 3% for a long, long time. The Fed is suggesting its decisions will be primarily based on wage growth. If the Fed funds rate is at 2% or 3%, that is OK. It would reflect a hibernating bear market.

Wage growth:

Unemployment:

However, the real beast is in China and elsewhere where there’s too much debt.

The problem is not in household or government debt. The problem is in corporate debt and in zombie corporate debt. If rates go higher we might see casualties in high yield debt.

Gross also mentions the SWAP curve which is very flat. Historically, this has very often preceded a slowdown if not a recession.

Investors should position for slower growth. Central banks have been raising rates. Curves are flattening. Growth will be slow. Gross believes equities may be pricing that in.

Gross built his career positioning his fund right for the given interest rate environment. The cool thing with (successful) practitioners is that you don’t have to go by their word. You can look what they are actually doing. That’s why I pulled up the top 25 holdings of the Janus Unconstrained (JUCAX) that Gross manages:

Data: Morningstar

Gross' biggest bet is on Time Warner, which is a mergers and acquisitions play. The government is trying to stop its acquisition by AT&T (T, Financial) on antitrust grounds. The government has a very tough case on its hand because these aren’t direct competitors. It’s uncommon for bond funds to hold much equities, but Gross has ventured into M&A opportunities for several years now. He’s playing these as an angle to the low interest rate environment. Companies can borrow very cheaply due to Fed policy and M&A is one way to profit from that.

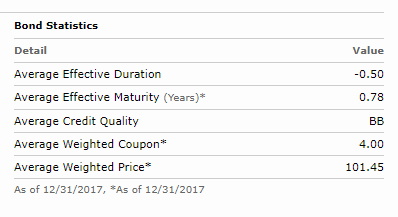

The statistics on the portfolio are also highly informative:

The duration of this bond fund is -0.5. That means it is going to rise 0.5% in value for every 1% interest rates are raised. Usually bond funds have positive duration figures meaning they go down in value if interest rates are rising. Gross must have obtained this exposure through derivatives.

The average credit quality of his portfolio is also very low at BB. Because the average coupon is so low given the credit quality I’d expect he mostly holds shorter term bonds.

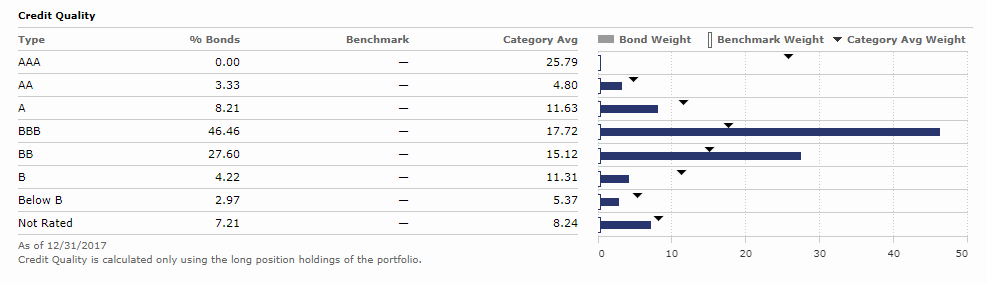

He’s underweight the benchmark’s 25% AAA bonds by 100%. This signals he really doesn’t like developed world Treasuries.

To sum it up, the takeaways from Gross portfolio:

- (Selective) M&A plays.

- Avoid interest rate risk.

- Avoid exposure to AAA rated sovereign debt.

Disclosure: Author is long TWX.