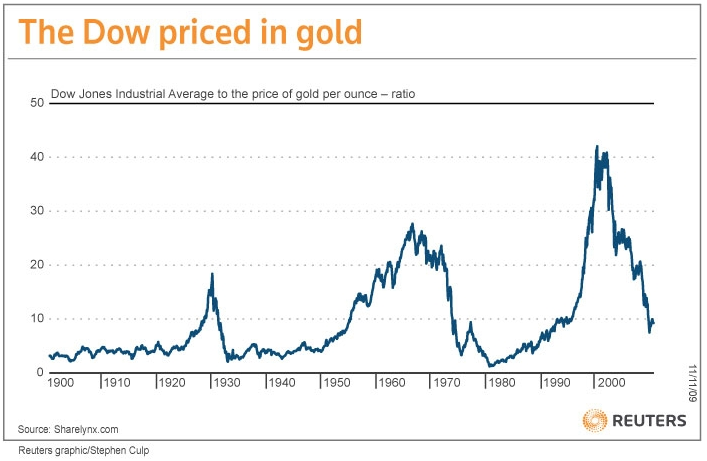

One of my favorite macro indicators is the long-term Dow:gold ratio. Rolph Winkler of Reuters blog Contingent Capital did the heavy lifting last week to produce a chart of the Dow Jones Industrial Average priced in gold per ounce since 1900:

The Dow:gold ratio is not everyone’s cup of tea. Paul Kedorosky likens it to measuring yo-yos in meerkats, but says it’s “semi-useful.” I agree. Several semi-useful observations that can be made from the chart include:

One thing clear to me from the chart is that buying equities from the late 1990s to the present was like running up the down escalator. It was fun, but it wasn’t the easiest way to get to the top. Standing still on the up escalator was an easier ride. This was the point of my Buffett on gold post last week. The change in the Dow:gold ratio for the period 1964 to 1979 makes it clear why Buffett was bested by gold over that period. The change in the ratio for the period from the early 1980s through to the late 1990s, combined with Buffett’s otherworldly ability to identify undervalued equities, also explains the lollapalooza gains made by Berkshire Hathaway during that period. It might also suggest that at some stage in the near future equities will again be the up escalator, but not quite yet, for the reasons below.

In an inflationary environment a business must keep increasing the price of its goods or services just to keep its margins static, and any reinvestment in plant and machinery must be undertaken at increasingly higher prices. If it can’t increase its prices or it doesn’t earn enough to keep up with its maintenance capital expenditure, then it will shrink and risks falling behind any competitor that can. In other words, it has to run up the down escalator, and if it can’t run faster than the escalator, then it’s going backwards. Businesses with no pricing power and low returns-on-equity will therefore suffer in an inflationary environment. While it is true that a business with pricing power and high return-on-equity is better able to protect itself somewhat from inflation, it is not true that inflation is good for this business either. Since I (and, I suspect, most investors) can’t prospectively pick one from the other, perhaps stepping onto the up escalator in such times is not such a bad idea. All gold does is sit there, yes, but it can’t be printed, so it tends to appreciate against the dollar as the dollar is debauched.

Has the dollar been debauched? The Austrian economist in me thinks so.Einhorn, John Paulson, Rogers and Buffett’s commentary on US fiscal and monetary policy can’t all be wrong. Keeping interest rates too low for too long and printing too much money – what Buffett describes as “Greenback emissions” – will result in inflation measurable in the CPI in the not too distant future. (As an aside, I think there is inflation now, but because it’s not running through the CPI yet it doesn’t exist according to the orthodox view, which also happens to be the one in power, and on both sides of politics, for that matter).

What can we deduce from the foregoing? If gold does as it has done in past cycles, it should do well for the foreseeable future. That has to be tempered by the fact that the gold price has run a long way, both in dollar terms and in comparison to equities (as measured against the DJIA). Gold could have a big reversal – in the mid-1970s the DJIA rallied significantly against gold before sinking to its long-term bottom – before it continues onto historical highs. In this regard, Jim Rogers’ recent commentary is instructive [via The Globe and Mail]:

Greenbackd

http://greenbackd.com/

The Dow:gold ratio is not everyone’s cup of tea. Paul Kedorosky likens it to measuring yo-yos in meerkats, but says it’s “semi-useful.” I agree. Several semi-useful observations that can be made from the chart include:

- Gold has outperformed the DJIA from the late 1990s to the present. In the late 1990s the Dow was more expensive in gold than it had ever been in the preceding 100 years.

- In 2009, the gold trade is getting long in the tooth. Most of the really big gains in gold have already been made. It’s no longer obviously cheap relative to equities, however…

- …it’s probably not over yet. The Dow:gold ratio has traditionally bottomed at a point significantly lower than we have seen this time around. This might suggest that it still has a ways to fall before it reaches the nadir. For the bottom to come in, either gold has to go up, equities have to come down, or some combination of both has to occur. My guess is the latter, however, this is not the only view out there. For example, in the Buttonwood’s notebook column of the Economist, Buttonwood asks, “Is gold the next bubble?“ WHAT are the preconditions for a bubble? Perhaps there are four: easy credit conditions, a significant trend-breaking event, the lack of plausible valuation measures and an appealing story.

Gold fulfils most of these conditions. One can argue about the credit conditions; lending is still weak but crucially interest rates are low. That helps given that gold has no yield; in effect, the opportunity cost of holding gold has disappeared. The event that changed minds was the credit crunch, which caused a partial loss of faith in banks. Gold has no valuation issues (no yield or earnings); since people hold it as a store of value, it can be worth whatever they want it to be worth. And it has a plausible backstory; spendthrift governments are monetising their deficits like the Weimar Republic before them.

…

…whereas one can say, based on historic valuation measures, that Wall Street is currently 40% overvalued, one can make no such bold statement on gold.The next stage of a bubble would be broad-based public interest

One thing clear to me from the chart is that buying equities from the late 1990s to the present was like running up the down escalator. It was fun, but it wasn’t the easiest way to get to the top. Standing still on the up escalator was an easier ride. This was the point of my Buffett on gold post last week. The change in the Dow:gold ratio for the period 1964 to 1979 makes it clear why Buffett was bested by gold over that period. The change in the ratio for the period from the early 1980s through to the late 1990s, combined with Buffett’s otherworldly ability to identify undervalued equities, also explains the lollapalooza gains made by Berkshire Hathaway during that period. It might also suggest that at some stage in the near future equities will again be the up escalator, but not quite yet, for the reasons below.

In an inflationary environment a business must keep increasing the price of its goods or services just to keep its margins static, and any reinvestment in plant and machinery must be undertaken at increasingly higher prices. If it can’t increase its prices or it doesn’t earn enough to keep up with its maintenance capital expenditure, then it will shrink and risks falling behind any competitor that can. In other words, it has to run up the down escalator, and if it can’t run faster than the escalator, then it’s going backwards. Businesses with no pricing power and low returns-on-equity will therefore suffer in an inflationary environment. While it is true that a business with pricing power and high return-on-equity is better able to protect itself somewhat from inflation, it is not true that inflation is good for this business either. Since I (and, I suspect, most investors) can’t prospectively pick one from the other, perhaps stepping onto the up escalator in such times is not such a bad idea. All gold does is sit there, yes, but it can’t be printed, so it tends to appreciate against the dollar as the dollar is debauched.

Has the dollar been debauched? The Austrian economist in me thinks so.Einhorn, John Paulson, Rogers and Buffett’s commentary on US fiscal and monetary policy can’t all be wrong. Keeping interest rates too low for too long and printing too much money – what Buffett describes as “Greenback emissions” – will result in inflation measurable in the CPI in the not too distant future. (As an aside, I think there is inflation now, but because it’s not running through the CPI yet it doesn’t exist according to the orthodox view, which also happens to be the one in power, and on both sides of politics, for that matter).

What can we deduce from the foregoing? If gold does as it has done in past cycles, it should do well for the foreseeable future. That has to be tempered by the fact that the gold price has run a long way, both in dollar terms and in comparison to equities (as measured against the DJIA). Gold could have a big reversal – in the mid-1970s the DJIA rallied significantly against gold before sinking to its long-term bottom – before it continues onto historical highs. In this regard, Jim Rogers’ recent commentary is instructive [via The Globe and Mail]:

Rogers: I don’t ever like to buy something making all time highs however I’m not selling my gold. Gold is going to go much higher in the course of the bull market. Doesn’t mean it can’t go down 20 per cent next year but during the course of the bull market it is going to go much higher it is certainly not a bubble yet.

Jim you are typically a contrarian investor. If everyone is buying, shouldn’t you be selling?

Rogers: Yes, I should be selling at the top, but I don’t think this is the top. Gold, if you adjust it for its old highs, adjust it for inflation back in 1980, gold should be over $2000 an ounce right now. In my view, in this bull market in commodities gold will make all new highs adjust for inflation.

…

When will gold hit 2k?

Rogers: I wish I was that smart. You should watch TheStreet.com. They know everything.

Greenbackd

http://greenbackd.com/