If you’re not familiar with Pool Corporation (POOL, Financial), it’s a wholesale distributor of swimming pool equipment and related leisure products… and it’s headed for rough waters.

Agora Financial’s expert on beleaguered corporations Dan Amoss, has just reported back on issues with working capital that are going hit its cash flow statement hard.

According to Amoss:

“Poolcorp (POOL) maintained its string of disappointing earnings reports. It lowered 2010 earnings guidance to a range of $1.00 to $1.15 per share, which is below what the consensus of analysts had modeled. The CEO’s guidance on the conference call sounded like nearly every other CEO’s guidance — low expectations for the first half and a rebound in the second half of 2010:

“‘We anticipate lower sales and gross margin in the first part of 2010 with gradual recovery during the year including positive sales and earnings comps in the second half.’

“Poolcorp management touts the company’s ‘record cash flow from operations’ in 2009, but much of this cash flow was one-time in nature as inventories were drawn down to match lower sales.

“Storing inventory is a costly drag on cash flow. Poolcorp spends 3-4 cents of every dollar in sales on rent for its sales centers. Poolcorp’s sales have shrunk on a year-over-year basis in every quarter since Sept. 2007. As sales shrink, lease costs grow as a percentage of sales.

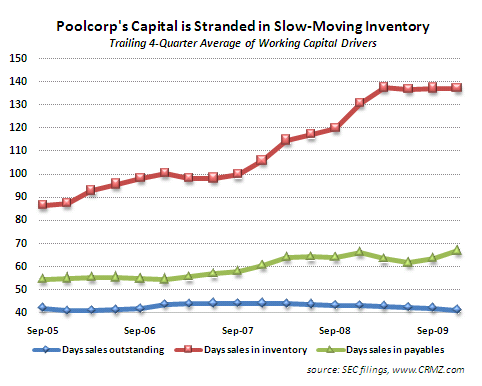

“As sales shrink, inventory turnover also slows. This cuts into Poolcorp’s return on equity. With data courtesy of CreditRiskMonitor, we charted Poolcorp’s ‘days sales in inventory,’ which is a measure of the number of days it would take to turn its inventory into sales (red line in the chart below). Its ‘days sales outstanding’ (blue) measures how long it takes to collect cash after a sale has been made. And its ‘days sales in payables’ (green) measures how long it takes to pay suppliers for items shipped on credit.

“Since the company’s working capital fluctuates wildly with the pool season, we smoothed the chart out by taking the trailing four-quarter average for each metric. The result shows a clear, steady deterioration in working capital efficiency. The deterioration has slowed in recent quarters, but the damage has already been done.

“Poolcorp’s cash flow has exceeded its earnings since the recession began, but whenever the recovery in sales arrives, cash flow will take a major dive. At $20 per share, the stock sells for roughly 20 times sustainable free cash flow. This is too expensive for a business with this type of long-term growth profile.”

Amoss paints a grim picture for Poolcorp’s current cash position, and it will be an interesting, if a bit unsettling, story to watch unravel over the near term. He has a unique gift for finding weaknesses in company balance sheets. You can read more about his work and recommendations by visiting the Agora Financial reports page.

Rocky Vega

The Daily Reckoning

Agora Financial’s expert on beleaguered corporations Dan Amoss, has just reported back on issues with working capital that are going hit its cash flow statement hard.

According to Amoss:

“Poolcorp (POOL) maintained its string of disappointing earnings reports. It lowered 2010 earnings guidance to a range of $1.00 to $1.15 per share, which is below what the consensus of analysts had modeled. The CEO’s guidance on the conference call sounded like nearly every other CEO’s guidance — low expectations for the first half and a rebound in the second half of 2010:

“‘We anticipate lower sales and gross margin in the first part of 2010 with gradual recovery during the year including positive sales and earnings comps in the second half.’

“Poolcorp management touts the company’s ‘record cash flow from operations’ in 2009, but much of this cash flow was one-time in nature as inventories were drawn down to match lower sales.

“Storing inventory is a costly drag on cash flow. Poolcorp spends 3-4 cents of every dollar in sales on rent for its sales centers. Poolcorp’s sales have shrunk on a year-over-year basis in every quarter since Sept. 2007. As sales shrink, lease costs grow as a percentage of sales.

“As sales shrink, inventory turnover also slows. This cuts into Poolcorp’s return on equity. With data courtesy of CreditRiskMonitor, we charted Poolcorp’s ‘days sales in inventory,’ which is a measure of the number of days it would take to turn its inventory into sales (red line in the chart below). Its ‘days sales outstanding’ (blue) measures how long it takes to collect cash after a sale has been made. And its ‘days sales in payables’ (green) measures how long it takes to pay suppliers for items shipped on credit.

“Since the company’s working capital fluctuates wildly with the pool season, we smoothed the chart out by taking the trailing four-quarter average for each metric. The result shows a clear, steady deterioration in working capital efficiency. The deterioration has slowed in recent quarters, but the damage has already been done.

“Poolcorp’s cash flow has exceeded its earnings since the recession began, but whenever the recovery in sales arrives, cash flow will take a major dive. At $20 per share, the stock sells for roughly 20 times sustainable free cash flow. This is too expensive for a business with this type of long-term growth profile.”

Amoss paints a grim picture for Poolcorp’s current cash position, and it will be an interesting, if a bit unsettling, story to watch unravel over the near term. He has a unique gift for finding weaknesses in company balance sheets. You can read more about his work and recommendations by visiting the Agora Financial reports page.

Rocky Vega

The Daily Reckoning