- “The market” has done well this year. The S&P, the best of the bunch, is up over 10%.

- How about you? If you haven’t kept pace, here’s a rock-solid sector that has hit a temporary speed bump.

- If history is any guide - and it is - these great companies won’t stay cheap for long.

- The time to do your due diligence is today - and if you agree, the time to buy is now.

As recently as last week, I would have included Baker Hughes (BHI) in my discussion below. But then Halliburton divulged that it would like to acquire its very large rival Baker Hughes. BHI jumped 15% in 25 minutes. (Not that anyone would invest in just one company, of course, but that's 50% better than the S&P has done all year long!)

That's what happens when oil and gas stocks become temporarily cheap. As I wrote to the (too few, in retrospect) clients of ours that owned BHI, "I did not have inside information prior to BHI's 15% jump just prior to the close today. But I know the energy industry and know that, when quality companies get this cheap, (1) competitors will buy them out rather than build new business from scratch, and (2) these companies will inevitably rebound. This one just started to rebound faster in light of Halliburton's possible buyout."

(click to enlarge)

All oil and gas explorers, producers, servicers, drillers, machinery providers, and transport and storage firms are considerably cheaper today than they were just 6 weeks ago - so cheap, in fact, that one might make enough by buying them to do every bit as well as the market this year - even starting this late.

It couldn't come at a better time, in my opinion! I was cautious on the market by the end of summer, expecting an October time frame pullback. Our clients were mostly in preferred stocks and bond funds, with a healthy dollop of long/short mutual funds and even a few put options. Ouch. It certainly felt like the right thing to do all the way through mid-October as the market was falling and we were making money.

But then the market rebounded in a V-shaped recovery that, in 12 days, undid the entire 10% decline. We didn't immediately go long because every bear correction (well, every other bear correction) is punctuated by a series of head-fake rallies, but then resumes its decline. After five years straight up, those two weeks were our entire correction?? Couldn't be. But it was. So now we are starting from the uncomfortable position of making less than the market this year, and that will not stand. We have sold all those bonds, bond funds, preferreds, preferred ETFs and other income-only investments.

Fortunately, the sector I have known the best for the past 40 years in this business is oil and gas - fortunate because that is where the bargains are today, if only we have the fortitude to buy them. Oil and gas always suffer a so-called glut after the summer vacation driving season ends and people no longer need their air conditioner when it stays light until 9 p.m. or so. And that glut, during which time we can normally pick up some fine bargains as people tear their hair out over the demise of oil and gas, is ended when the days get shorter, the lights go on earlier, and we need heat here in the Northern Hemisphere. The glut goes away, and we who have bought oil and gas in the "glut" pocket our profits.

This year the problem has been exacerbated, however, by a serious slowing of manufacturing and production in Europe and Asia and by the marvelous enhanced oil & gas production we are enjoying in North America; not just US shale production, but Canadian and soon to be Mexican successes as well.

Goldman Sachs recently wrote that worldwide demand is likely to stay flat for some time because China and the developing nations will consume less. I don't think they will. People with a bicycle want a motorbike; those with a motorbike want a car. This trend is unstoppable, as is the need to mine resources or manufacture "things" for export.

Goldman further sees U.S. shale as a target for the Saudis and their OPEC brethren to break by producing all-out. While it is true that the Saudis can be profitable at a lower price point, I don't think U.S. shale producers are their target. I think it is their fellow OPEC partners and other competitors. It wouldn't hurt the Saudis' feelings if arch-enemy Iran were squeezed and brought to the bargaining table. And it wouldn't hurt U.S. diplomacy, either, if Russia, Iran and Venezuela were eating crow instead of selling oil & gas at a profit.

Indeed, unlike Goldman, I see U.S. shale production as a way to defeat any attempt to put the U.S. over a barrel (so to speak). According to the International Energy Agency (IEA), producers in the Marcellus Shale can make a 20% pre-tax return on investment in the Marcellus even if oil goes below $40 a barrel. The Eagle Ford, Utica and Bakken are still that profitable at less than $60 a barrel. In fact, according to the IEA, only 4% of shale production needs $80 oil to return that 20% pre-tax profit.

I further break down the oil and gas industry in the energy sector into four rough sub-sectors: machinery and equipment; transport and storage; field services (to include offshore); and the drillers, both land-based and offshore. It would be pretty cumbersome to put all these in a single article, so I will cover the first two sub-sectors here and will include the other two big sectors, plus (bonus round!) two more speculative special situations I think have superb potential. Let's start with…

Machinery & Equipment

National Oilwell Varco's stock symbol is NOV, which customers and nervous competitors sometimes say stands for "No Other Vendor." With good reason: NOV controls about 50% of the deepwater equipment market, while competing against the likes of Halliburton (HAL), Baker Hughes (BHI), FMC Technologies (FTI), Weatherford International (WFT), and Cameron International (CAM), all fine companies in their own right. (I have not included Dresser-Rand because its merger with giant conglomerate Siemens looks like a done deal, or Bolt Technology, because it is a smaller player, albeit with great strength in the niche market of subsea vehicles and equipment.)

These firms, and scores of others, build, sell and service entire rig systems, both offshore and land-based, as well as any of the hundreds of individual pipes, pumps, control systems, fluid handling and power systems, and all the rest that goes into the rigs. They also provide wellbore support with everything from drill bits and drilling fluid to coring services and waste management. For an in-depth overview, I suggest you go to nov.com and click on "Products." Every single item on that page has its own link for further info.

The bottom line is, without these companies making finely-honed, sturdy, and reliable equipment, there would be no exploration or production of oil and gas. As investors, we don't need in-depth knowledge of all the components that make this all come together; we need to know (1) that this is an essential industry that offers above-average growth, and (2) which companies are the most attractive to buy right now. While many other industries have run to new highs and are now on every momentum investor's buy list, none of these firms have set the world on fire. NOV is selling for 5% less than it did 12 months ago. BHI (well, until about 3:35 yesterday afternoon, anyway) was down 14%, HAL is down 4%, and WFT is down 4%. CAM is up 5%, while FTI is up 9%, the only one that has even come close to keeping pace with the market.

I don't think you could go wrong buying any of these. But of the five, leaving BHI out for now, HAL has the biggest enterprise value, NOV the lowest P/E, HAL and FMC the best ROA and ROE, NOV the best operating and net margins and the lowest debt/equity ratio, and HAL and NOV the best five-year revenue and earnings growth. Of the two that seem to float to the top here, NOV beats HAL on valuation criteria like Price/Book, Price/Sales and the PEG Ratio (Price/Earnings Growth). Of the bigs, NOV is still our favorite. And when the biggest, most competitive and most highly-regarded firms in the industry have sold off every bit as much as the less well-managed or less well-capitalized firms, why not buy the best? We are buyers first of NOV, then of HAL.

Transport and Storage

The benefit of owning pipeline and storage companies is that they get paid on through-put, not on the price of the commodity. Also, these are by and large domestic, or at least North American firms, so their earnings are less dependent upon the currently-weaker economies of Europe, Asia and the emerging markets. If Americans consume more oil and gas this winter, the transport and storage outfits make money. It doesn't much matter if that oil-equivalent barrel is priced at $70 a barrel or $100 a barrel; they get paid to transport something regardless of its value. Think of these companies as a UPS or FedEx (FDX) - whether the contents of the package UPS delivers is worth $10 or $100, UPS charges by weight and distance, not by the value of the contents. That's what pipeline companies do. The storage end of the equation is slightly different; the prices received for storage are less subject to federal regulation and are therefore more subject to the laws of supply and demand.

So what are the best pipeline companies to own? That depends upon your end-goal. If you're looking solely for current income you might buy Niska Gas Storage (NKA) which pays at a 30% yield - but has lost 69% of its value over the last 12 months. I can name another dozen that pay double-digit yields, though I personally wouldn't buy one of them for myself or our clients. I'd rather have steady, conservative growth with a well-managed company that increases its DCF (distributable cash flow) every year and its distributions as often.

Pipeline firms don't really "compete" with each other; FERC, the Federal Energy Regulatory Commission, regulates most aspects of interstate pipelines, and gives an effective monopoly to the pipeline from point A to point B and sets rates for flow that are "just and reasonable." So when reviewing competitive position in this sub-sector, we want to select those companies with management that is most astute and a network of pipelines that are in basins with lots of proven reserve life left in them, instead of old fields only pumping with tertiary recovery methodologies.

A few names percolate to the top as pipeline builders in the newest and most prolific areas. Among these are TransCanada (TRP), Enbridge (ENB), Oneok (OKE) and Statoil (STO).

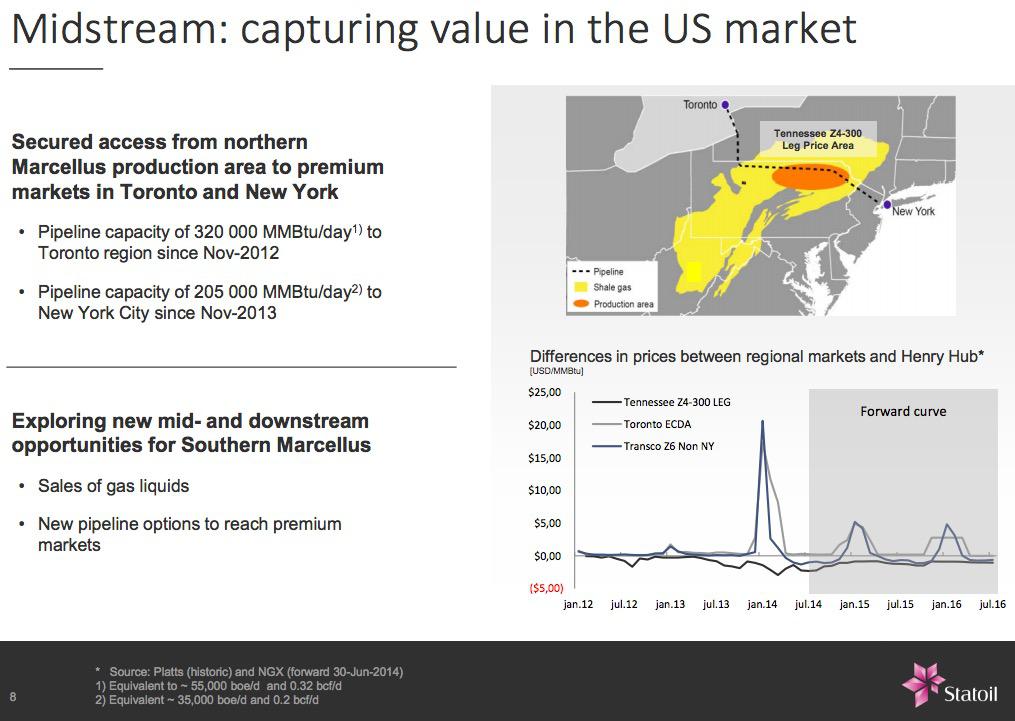

Statoil? Statoil? What am I smoking, you ask? For those who only know STO as the Norwegian state oil company, a powerhouse in Europe and the supplier of the world's newest LNG terminal (the Klaipeda terminal in Lithuania, which completely eradicates the Russian stranglehold on Lithuania,) you may wonder at its inclusion here. But STO also spent $4 billion to buy the U.S. company Brigham Exploration, a major Bakken player, and is hard at work building storage facilities here in the U.S. STO is now a serious producer in the Marcellus and the Eagle Ford. And in addition to its 5,000 miles of pipelines in Europe, it now owns pipelines from the Marcellus shale direct to New York City and Toronto. This is yet another concrete example that there is tremendous overlap in each of these sub-sectors - here's a major integrated oil company that is now expanding its pipelines and storage divisions.

(click to enlarge)

You'll notice there is something missing from my analysis of the transporters. We made superb money and attracted lots of followers in previous years talking about the steady-Eddie income, growth and tax benefits of MLPs. Where are the MLPs (Master Limited Partnerships) that have done so well for us in the past? Well, old favorites KMP and EPB are being absorbed by our also-favored parent company KMI. That leaves Plains All American (PAA) and, for both growth and yield, QR Energy (QRE), Linn Energy (LINE), and EV Energy (EVEP) atop our few remaining MLPs we might still consider buying, except...

...I am more and more interested in acquiring the parent companies that pay ordinary dividends rather than the MLPs that pay tax-advantaged distributions via K-1s these days. My reason has nothing to do with K-1s, however. It has to do with the growing sentiment in Congress to do in the U.S. what the Canadians did in 2011 and remove the tax-advantaged status of LPs. It makes me uneasy at best. It doesn't have to even happen to cause a big downdraft in MLPs; just being floated as an idea by some Congressman will be enough to send them down 10% in a day. We've seen enough of that kind of volatility, thank you. If I have to pick only one, it would be KMI.

Bottom line - we are buyers of NOV, HAL, STO and KMI, with a dozen more to come next. In Part II, I'll cover the dirt-cheap drillers (where we are placing most of our funds right now) and the biggest and best servicing outfits, as well as our favorite big integrated oil and gas companies. Oh, and those special situations for the more risk-tolerant, as well!

The Fine Print: As Registered Investment Advisors, we believe it is our responsibility to advise that we do not know your personal financial situation, so the information contained in this communiqué represents the opinions of the staff of Stanford Wealth Management, and should not be construed as personalized investment advice.

Past performance is no guarantee of future results, rather an obvious statement but clearly too often unheeded judging by the number of investors who buy the current #1 mutual fund one year only to watch it plummet the following year.

We encourage you to do your own due diligence on issues we discuss to see if they might be of value in your own investing. We take our responsibility to offer intelligent commentary seriously, but it should not be assumed that investing in any securities we are investing in will always be profitable. We do our best to get it right, and we "eat our own cooking," but we could be wrong, hence our full disclosure as to whether we own or are buying the investments we write about.