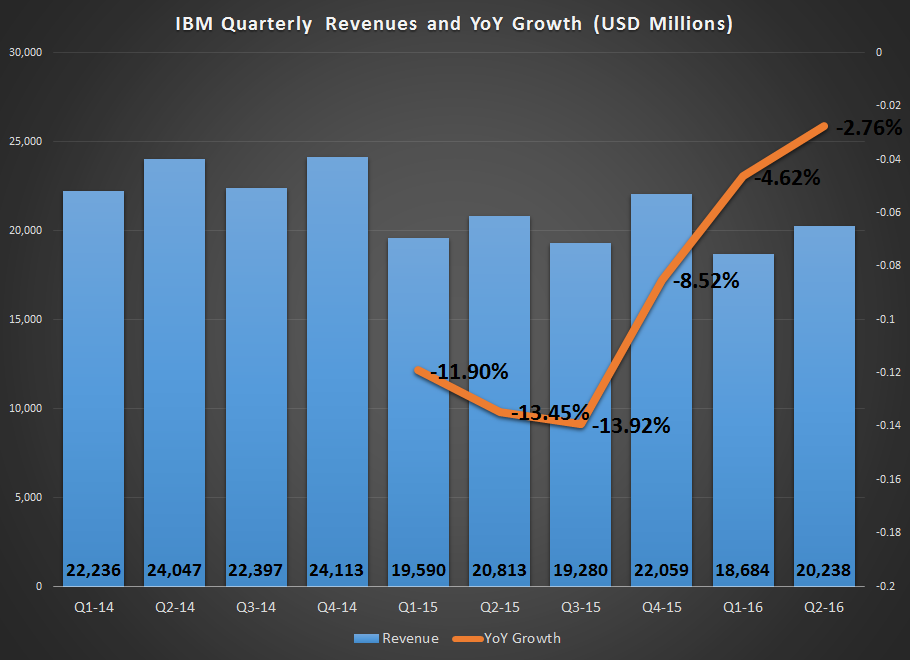

IBM’s (IBM, Financial) painful transition back to revenue growth seems to be closer than ever if the second quarter results are anything to go by. IBM’s second quarter 2016 revenues came in at $20.24 billion, down by 2.76% compared to the $20.81 billion posted last year. Last year, however, IBM’s quarterly revenues were declining at double-digit rates, but that pace has been slowing down since the third quarter of 2015 thanks to some of the new product lines such as analytics and cloud service reporting steady growth over that period.

Growing Parts of IBM’s Business

Let’s take a closer look at the growth drivers so that we can understand how IBM’s transition is taking place. In an earlier article, I spoke about how long that transition would take. In this piece, let’s look at what is supporting the 2018 target I estimated for IBM’s turnaround.

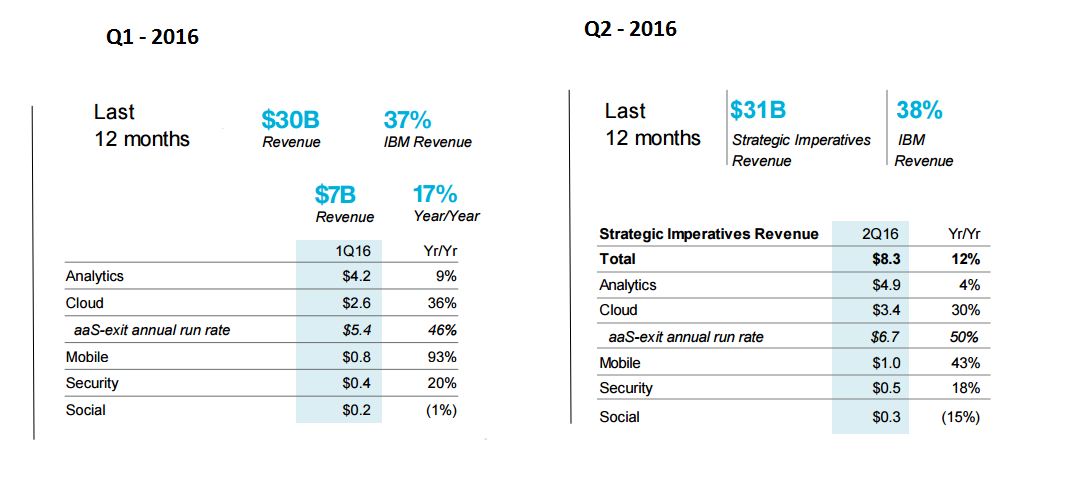

Revenues from IBM’s Strategic Imperatives - essentially comprising all of their newer lines of business including Analytics, Cloud and Security - have grown from $7 billion in the first quarter of this year to $8.3 billion in the second quarter, and now account for 38% of overall revenue on a trailing twelve months basis. With IBM’s legacy business lines declining, it is this group of products that IBM is depending on to get back to its growth story; and as such, it is crucial for these product lines to perform well in the coming quarters.

IBM is, of course, one of the top companies in the cloud space that is shared with other market leaders like Amazon (AMZN, Financial) and Microsoft (MSFT, Financial) - with Google (GOOG) (GOOGL) recently jumping into the fray. Let’s look at how the other top three companies fare on cloud revenues.

Microsoft’s commercial cloud is now at a $12.1 billion run rate, meaning they made $3.03 billion during this quarter. That’s up from a run rate of $10 billion as of the previous quarter. IBM’s -as-a-service business is now at a run rate of $6.7 billion, translating into $1.67 billion during this quarter. Total cloud revenues for the last twelve months were at $11.6 billion.

Amazon’s most recent quarterly (1Q, released on April 28) showed quarterly revenues of $2.6 billion for AWS. That gives them an exit run rate of $10.4 billion and a YoY growth of 64%.

It is a bit difficult to compare these companies and choose a winner because each company has its own set of line items that are included while calculating their cloud revenues. I’ve already shown a more relevant comparison by using their trailing twelve-month cloud revenues. Yet, another effective way to do an apples-to-apples comparison is by looking at their respective growth rates.

Comparative Cloud Growth

Amazon Web Services has been growing at +50% range for the last few quarters while Microsoft’s Azure revenues have grown by +100% during the last two quarters and they exited the current quarter with $12.1 billion run rate from their cloud business. IBM’s cloud business has grown from $4.5 billion in the second quarter of 2015 to the current $6.7 billion, giving them a growth rate of 48%, which is very much in line with what Amazon has been achieving in the last few quarters.

It is indeed a bit heartening to see IBM keeping pace with fast-paced companies like Amazon and Microsoft.

The Watson Angle

Analytics is another segment which I believe will be a key driver for IBM’s growth in the next five years and beyond.

At the end of the second quarter, revenue from analytics touched $4.9 billion, a growth of 4% when compared to last year. Analytics now accounts for more than half of their strategic imperatives revenue, and having interviewed IBM General Manager for Collaborative Solutions Inhi Cho Suh and IBM Watson Health General Manager Deborah DiSanzo as well as other senior executives during this past quarter, I see no problem with IBM achieving an even higher growth rate on analytics as they get involved with healthcare.

The slowing pace of overall decline from almost -14% three quarters ago to -2.8% in the second quarter of 2016 is a clear sign that IBM’s growth cycle is imminent. Cloud and analytics will be the strongest arrows in CEO Virginia Rometty’s quiver, ably supported by Watson, Cognos, Bluemix, SoftLayer and other core offerings that are driving that growth.

I’ve already made my position amply clear on IBM stock in my recent articles on cloud and IBM itself. The growth drivers are in place, legacy decline is approaching zero level and the company is poised on the threshold of their new growth cycle. Investing now will strengthen your portfolio immensely over the next two-to-five year period, and you can keep collecting on the 3.5% dividend in the meantime.

Thanks for your valuable time spent reading this article. If you found any value, I ask that you share it on Facebook and Twitter so others can benefit, too.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.