Thoughts on current valuation and does it matter for such a strong compounder?

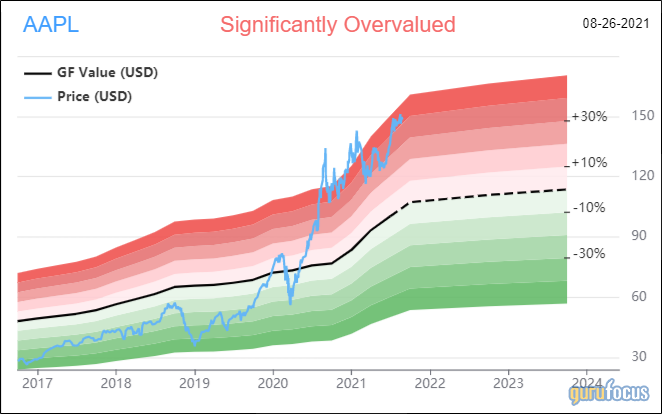

AAPL

We missed the boat on apple for the time being.

I prefer to own Apple via Berkshire. Berkshire own over 5% of apple shares - plus you get a lot of other great businesses for a much more reasonable valuation.

Worldwide smartphone shipments are expected to recover from last year's pandemic-related losses to post a 7.4% growth in 2021, according to new IDC forecasts.

Did you notice that Apple's TTM p/e is less than that of S&P 500?

If you own AAPL, ignore the short term ups and downs and hold it for the long run.

It´s a very hard question :)

I think the better question to ask is what will make them continue their impressive growth in the future?

IPhone accounts for more than half of their revenue and they have a fairly stable global market share between 10-20% of the global market.

The market is being saturated, but can they keep generating more revenue from their phones? Or will they expand into other areas?

If they introduce an electrical vehicle, will the current Apple fans buy into it? Then it could expand their revenues significantly. On the other hand, the EV market is increasingly being crowded and they are not first-movers like they were with the iPhone.

Tesla was the real first mover in EV and I understand that their marketshare is falling. We have a lot of new entrants Nio, Xpeng, Mercedes, Ford, VW e.t.c.

I'm not sure when this was posted but at the current time 9/15/21 at a price of $149 it looks like it could drop 22% to get to a fair value, IMO. I am doing my growth projections and I'm much more conservative in my revenue estimate for 2022. There seems to be a cool-off year after these large surges in revenue like we're seeing in 2021, I think 2022 we'll see a dip around 5%, even if Profit & FCF margins on the high end near 25% & 28%, respectively, price could drop to $115, I think, but this is apple I'm betting against, I must be an idiot, so who knows ¯\_(ツ)_/¯

Apple doesn't need to be the first mover in technologies. They've shown repeatedly (iPod, computers, tablets, phones, watches, etc.) that they are able to learn from competitors and make a product that people really want and are willing to pay a premium. Smartphones will continue for some time, but I trust that Apple will be able to create smart glasses or whatever is next for personal computing and connectivity.

... but I trust that Apple will be able to create smart glasses or whatever is next for personal computing and connectivity.

Perhaps, but I would like to hear what that trust is based on. Post 1997, Apple became a company producing a constant stream of devices people want. I for one don't fully understand what changed in 1997 but whatever it is, why should it remain so for the next decade (or two)? That is what the current stock price implies.

Take Union Pacific. It is somewhat easier to make a coherent argument why that company is likely to dominate its industry in 2051 (let alone 2031) and their EPS too has been compounding at double digits. Apple is more expensive and (at least to me) less easily understood.

Would love to hear more thoughts.

Survey

We'd love to learn more about your experiences on GuruFocus.com and how we can improve!

Take Survey

Follow Us

Disclaimers