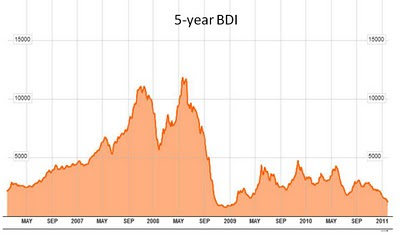

Diana Shipping (DSX, Financial) transports dry-bulk cargo using its fleet of 20+ ships. The state of the industry is pretty poor right now, with shipping rates, as measured by the Baltic Dry Index, having fallen quite a bit:

Rates are quickly approaching those of March 2009! (For a description of how this index works, see here.)

Because of the negativity surrounding this industry, the market may have overreacted to the downside. Shares of companies such as Diana Shipping have fallen significantly; the company trades at a P/E of just 7 and at a 15% discount to book value, which is mostly made up of previously purchased ships. But this company is capitalized to outlast a downturn, with a current debt to total capital ratio under 25%.

Unfortunately, this isn't an open-and-shut case, as there are a few risks here. First, Diana relies on four customers for more than 2/3's of its revenue. If Diana were to lose one of these charterers as a customer, it may not be able to secure equivalent terms on new leases.

There are also risks to the company's short-term profits. The company has mostly chartered out its fleet on 2-3 year contracts. If these contracts expire while shipping rates remain low, the company's profits are likely to fall; so while the current P/E is 7, the future P/E could be higher even without price appreciation.

But perhaps the biggest risk to this company is what it can't control, namely the prices of the goods it transports and, perhaps more importantly, the prices of the services it provides. Similar to the airline industry, which is a terrible industry for long-term investors, shipping transportation companies are enormously affected by the mistakes of their competitors. If some shipping companies over-order new ships (which history shows to be quite likely to occur every now and then), all companies, including Diana, will be forced to cut prices.

To succeed in such an environment, Diana must be one of the lowest-cost operators. The problem with this is that it's not an easy thing to do. As Warren Buffett has stated, value investors want to own companies that can be managed by a monkey. But a company that needs to be the low-cost operator needs a skilled management.

Diana looks cheap and may even be cheap. The upside is likely larger than the downside, based on the company's strong financial position and near-term earnings power. Unfortunately, the company's long-term potential is somewhat out of its control, which increases its risk profile for the value investor.

Disclosure: None

Rates are quickly approaching those of March 2009! (For a description of how this index works, see here.)

Because of the negativity surrounding this industry, the market may have overreacted to the downside. Shares of companies such as Diana Shipping have fallen significantly; the company trades at a P/E of just 7 and at a 15% discount to book value, which is mostly made up of previously purchased ships. But this company is capitalized to outlast a downturn, with a current debt to total capital ratio under 25%.

Unfortunately, this isn't an open-and-shut case, as there are a few risks here. First, Diana relies on four customers for more than 2/3's of its revenue. If Diana were to lose one of these charterers as a customer, it may not be able to secure equivalent terms on new leases.

There are also risks to the company's short-term profits. The company has mostly chartered out its fleet on 2-3 year contracts. If these contracts expire while shipping rates remain low, the company's profits are likely to fall; so while the current P/E is 7, the future P/E could be higher even without price appreciation.

But perhaps the biggest risk to this company is what it can't control, namely the prices of the goods it transports and, perhaps more importantly, the prices of the services it provides. Similar to the airline industry, which is a terrible industry for long-term investors, shipping transportation companies are enormously affected by the mistakes of their competitors. If some shipping companies over-order new ships (which history shows to be quite likely to occur every now and then), all companies, including Diana, will be forced to cut prices.

To succeed in such an environment, Diana must be one of the lowest-cost operators. The problem with this is that it's not an easy thing to do. As Warren Buffett has stated, value investors want to own companies that can be managed by a monkey. But a company that needs to be the low-cost operator needs a skilled management.

Diana looks cheap and may even be cheap. The upside is likely larger than the downside, based on the company's strong financial position and near-term earnings power. Unfortunately, the company's long-term potential is somewhat out of its control, which increases its risk profile for the value investor.

Disclosure: None