The GEO Group, Inc. (GEO, Financial) is a prison operator structured as a real estate investment trust (REIT). It describes itself as specializing in the design, financing, development, and operation of secure facilities, processing centers, and community re-entry centers in the United States, Australia, South Africa, and the United Kingdom. GEO's worldwide operations include the ownership and/or management of 118 facilities totaling approximately 93,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 22,000. Most of its revenues and income are derived from the U.S.

GEO's stated mission is to develop public‐private partnerships with government agencies around the globe providing enhanced rehabilitation and community reintegration programs for the prisoners contracted for under its care. GEO and CoreCivic (CXW), the two companies that manage federal prisons, alone combine for 17 contract facilities that accommodate around 13 percent of the Federal Bureau of Prison's (BOP) total capacity of roughly 9,800 inmates. BOP represents 14% of Geo's 2020 revenue.

The company's stock price has been crushed because of the Biden administration's dislike of private prison operations and a recent executive order to the Federal Bureau of Prisons to not renew contracts with private prison operators, going forward. Further due to social pressures andESG mandates, many financial institutions have stated that they will withdraw from lending money to private prison operators. On April 7, 2021, GEOsuspended its quarterly dividend payments, with the goal of maximizing the use of cash flows to repay debt, deleverage, and internally fund growth, and its stock price collapsed further. It is possible that GEO may convert from REIT to a C-Corp to navigate its current funding issues and impending non-renewals.

The above and following charts give the company's revenue and net operating revenue distribution.

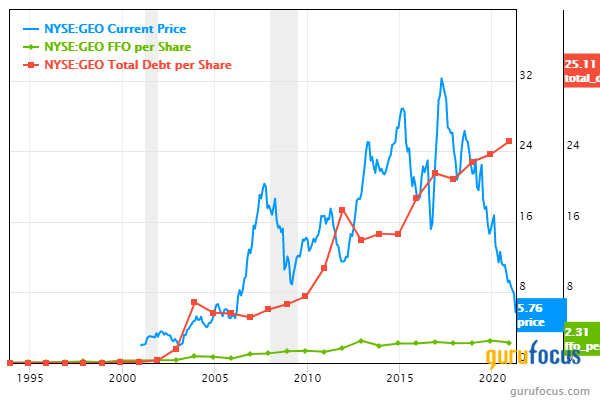

Geo group is quite highly leveraged with debt of ~9 billion and equity of 2.1 billion. Market capitalization is only 690 million.

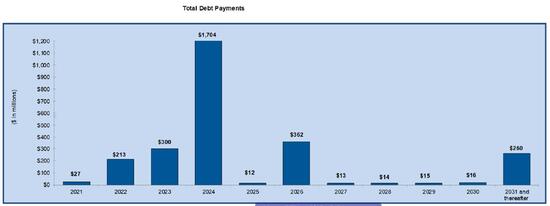

The following chart shows the schedule of Debt Payment. $1.7 Billion of debt comes due in 2024. Therefore, GEO has about 3 years to figure out how to reschedule or repay this bolus of maturing debt. That will in turn depend on GEO ability to sell or re-lease the properties which are not being renewed by the Feds. The company has ample to time to sell or re-lease the properties which the BOP is not renewing. There is a good possibility the BOP will buy the properties from GEO, or just rent the property and operate it itself, as it will be more economical that building a new custom facility. We will just have to wait and see how the chips fall in the quarters ahead.

Valuation

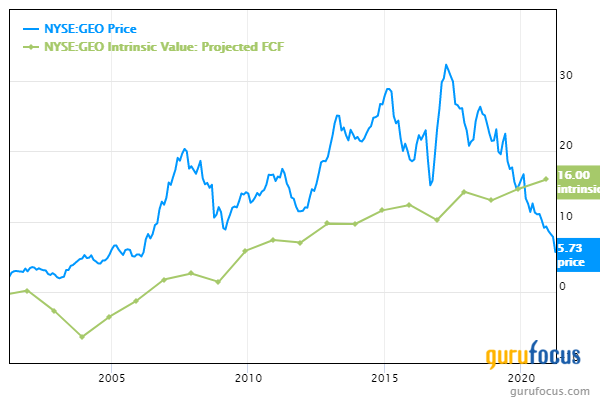

I think a good way to value the company is by theProjected FCF method pioneered by Gurufocus. The method which uses a combination of 6 years of normalized Free Cash Flow and 80% of book value is designed for companies which have somewhat erratic cash flow from year to year. This method indicates a value of $16 a share and shows considerable margin of safety as the stock price is below $6 presently. It implies a 150% upside.

Conclusion

Looking at the chart below over the last 20 years, GEO has never traded at such a discount from its projected FCF value. Clearly the stock market is expecting GEO to be at high risk of insolvency over the next 3 years. While that pessimitic scenario is not unreasonable, I think there is a greater chance that GEO will muddle through by selling off unneeded assets, and thus this market despondency represents an opportunity for investors with a high tolerance for risk.

In my opinion President Biden's executive order is unlikely to solve much, as the root cause is that the US justice system still relies heavily on indiscriminately locking people up for long periods of time rather than immigration reform, addiction treatment or rehabilitation of inmates and prisoners. The net result is the US has thehighest prison population in the world on a per capita basis in the industrialized world. While this may not be a growth industry, rumors of the death of the industry are greatly exaggerated. It would require fundamental reform, which will eventually happen, but will take a long time. For example we have known that cigarettes are harmful for over 50 years now, yet cigarette companies remain viable and very profitable. While the preceding example may be too exagerated, I think there is ample time for GEO to right size its footprint and re-tool its services to navigate the new slowly emerging reality. Crime & Punishment are not going away.

Disclosure: The author owns stock of The GEO Group Inc.

Read more here:

- Cognitive Biases in Investing

- Manila Electric Co. - Strong Balance Sheet and Good Dividend

- Watsa's Atlas and Fairfax Are in a Sweet Spot

Not a Premium Member of GuruFocus? Sign up for a free 7-day trial here.