The residential real estate industry has been targeted by tech players for disruption. It has all the ingredients for process innovation. It's a huge complex market with multiple independent players who need to coordinate with each other like buyers, sellers, their agents and brokers, lawyers, mortgage providers and servicers, escrow and conveyance services, title insurance, movers, etc. This market has attracted multiple "disruptors" in recent years. Compass Inc. (COMP, Financial) is one such disruptor.

Compass is building a tech-enabled platform for full-service real estate agents. In this, it is similar to Redfin Corp. (RDFN, Financial), which is more of a discount operator.

The company was incorporated on Oct. 4, 2012 in Delaware under the name Urban Compass Inc. On Jan. 8, 2021, the company changed its name to Compass Inc. It completed its initial public offering on April 1 of that same year.

Compass provides an end-to-end platform that enables its residential real estate agents to deliver services to clients. The platform includes an integrated suite of cloud-based software for customer relationship management, marketing, client service and other critical functionality for the real estate industry, which enables its core brokerage services. The platform also uses proprietary data, analytics, artificial intelligence and machine learning to deliver recommendations and outcomes for Compass agents and their clients.

The company’s agents are independent contractors who affiliate their real estate licenses with it, operating their businesses on Compass' platform and under its brand. Compass generates revenue from clients through its agents by assisting home sellers and buyers in listing, marketing, selling and finding homes as well as through the provision of services adjacent to the transaction, like title and escrow services, which comprise a smaller portion of the company’s revenue to date. The company currently generates substantially all of its revenue from commissions paid by clients at the time that a home is transacted.

Since its IPO, shares have dropped.

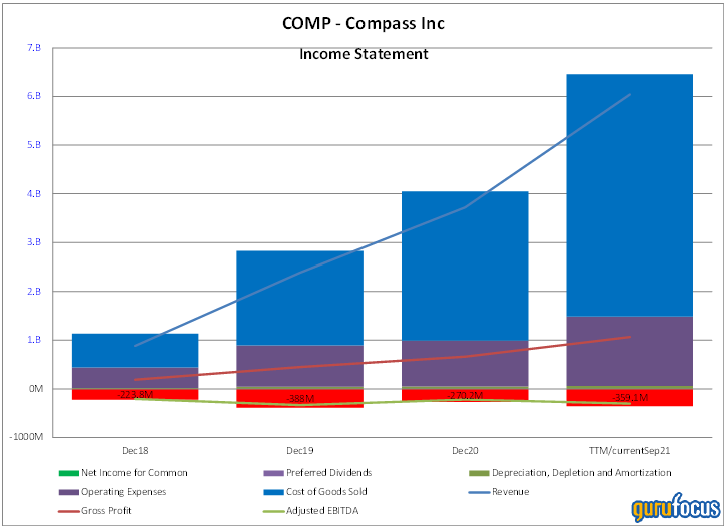

Sales are growing rapidly, but so are losses

The following diagram shows the income statement over the last four years. Compass appears to be losing money on a GAAP basis. This is mainly due to the large amount of stock option compensation and restricted stock that has been given out to executives and other associates. The stock option overhang is a significant dilution risk to shareholders.

The large stock-based compensation can be seen in the cash flow diagram below (light blue). The company issued stock compensation worth $306 million this year to insiders. While about $150 million of this related to the IPO, the company is still issuing about $50 million to $70 million per quarter of stock options. This is an excessive amount of compensation for insiders while the stock continues to plummet. Indeed, that may be the reason why investors are fleeing.

Since stock-based compensation is non-cash, the company is able to show that it is free cash flow positive. However, that is not the case. Positive free cash flow is illusory without prospects of GAAP profitability. The latter seems to be elusive given the amount of ongoing (non-cash) stock compensation to insiders.

Dual class share structure

As of Sept. 30, 2021, the company has approximately 399 million shares of its common stock outstanding, which consists of about 384 million class A shares (having one vote each) and15 million class C shares (having 20 votes each). The latter is held by founder Robert Reffkin, who effectively controls the company. The 10-Q also discloses another 120 million of convertible securities (mainly outstanding stock options and RSUs), which could potentially dilute the value for shareholders. These securities potentially represent a significant overhang on the value of the stock.

Conclusion

Given the egregious stock option compensation and dual voting structure of the company, I think it may have an agency problem. Compass seems to be run more for the benefit of insiders than for outside shareholders. Given this conclusion, I don't think this is an attractive stock to own. While the company is showing strong top-line growth, it is not reflected in the bottom line. Unless the company can show sustainable top-line growth with some profitability, I think investors should stay away.