As a value investor I have often found myself highly dependent on thinking in terms of “margin of safety” when it comes to value. But Michael Mauboussin, Chief Investment Strategist at Legg Mason Capital Management and author of More Than You Know, suggests there is a better way to quantify value and opportunity: Expected Value. It may have been Buffett and Graham who popularized the renowned principal of “margin of safety” (or discount to fair value), but it was also Buffett who defined Mauboussin’s definition of expected value:

In the words of Michael Mauboussin:

Your firm is 80% certain Growth will obliterate earnings estimates and appreciate 40%. But your firm isn’t quite as certain about the upside for Boring. You are also 80% certain that Boring will beat earnings estimates but it will only result in an appreciation of 25%. This must mean Growth is a better investment, right? Not at all. We need to also take into consideration the bear scenario for each stock.

So, despite a very high probability of a massive 40% gain for Growth, Boring offers the same expected value of 18%. Furthermore, many value investors would argue that Boring is a better investment due to the downside protection and an equal expected value.

In other words, being right more than you are wrong is not what makes a good investor. What makes a good investor is the magnitude of your correctness.

Download and share the PDF VERSION here.

“Take the probability of loss times the amount of possible loss from the probability of gain times the amount of possible gain. That is what we’re trying to do. It’s imperfect but that’s what it’s all about”

Margin of Safety vs. Expected Value?

To define margin of safety you only need market price and fair value estimate. The margin of safety is simply the difference between the two. But seasoned investors know that investing is much more complex than this. Expected value looks at value and opportunity in terms of the weighted average of the probability of the bear scenario plus the bull scenario (or as many scenarios as you would like to include in the weighted average). This type of thinking can help you assess risk more effectively.Magnitude of Correctness over Frequency of Correctness

Yet another bonus is that expected value highlights the fact that what matters in investing is the magnitude with which you are right . . . not the frequency. While this lesson may seem elementary, it is often hard to actually internalize this concept when making investment decisions. Expected value helps you quantify this concept, which makes it easier to internalize.In the words of Michael Mauboussin:

“Focus not on the frequency of correctness but on the magnitude of correctness.”(click to tweet the above quote)

Expected Value in Action

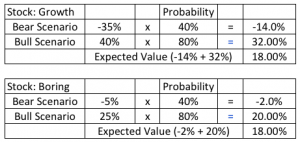

Consider this example: You are working at an investment firm and your team is considering a large investment in one of two stocks. Let’s call one Growth and the other Boring.Your firm is 80% certain Growth will obliterate earnings estimates and appreciate 40%. But your firm isn’t quite as certain about the upside for Boring. You are also 80% certain that Boring will beat earnings estimates but it will only result in an appreciation of 25%. This must mean Growth is a better investment, right? Not at all. We need to also take into consideration the bear scenario for each stock.

Don’t Forget the Bear Scenario!

If your team’s bull scenario estimates are wrong, investors may be deeply disappointed and the stock could plummet as much as 35%. Your firm sees a 40% chance for such a situation occurring. For Boring, however, your team believes that there is a 40% probability of a downside after earnings of only -5%.Weighted Expected Value Calculation

So, despite a very high probability of a massive 40% gain for Growth, Boring offers the same expected value of 18%. Furthermore, many value investors would argue that Boring is a better investment due to the downside protection and an equal expected value.

Expected Value Makes “Boring” Seem More Interesting

While this does not represent a thorough example of expected value thinking, it does make two very good points:- Magnitude of correctness needs to be the focus, not the frequency of correctness.

- Downside protection is very important to expected value.

In other words, being right more than you are wrong is not what makes a good investor. What makes a good investor is the magnitude of your correctness.

Download and share the PDF VERSION here.