Whirlpool Corp. (WHR, Financial), one of the world's most well-known appliance makers, is a dicey investment prospect at the moment, in my opinion. Sales are sluggish, the stock is volatile, and while debt has gone down, so has the company's cash balance. Whirlpool’s Beta is a high 1.45. Nevertheless, the company is working to expand and secure additional market share, which could help it grow in the long run. It also offers an attractive dividend yield.

About the company

Whirlpool brands are almost synonymous with household appliances in the U.S. The Whirlpool and KitchenAid brands stand among the Top 50 Brands of 2022 according to the Prophet Brand Relevance Index, which measures U.S. consumers' relationships with 293 "brands that matter most in their lives today." JennAir brand holds the prestigious 2022 Architectural Digest Great Design Award for best-in-class design for its new built-in dishwasher. Other brand names Whirlpool owns include Maytag, Amana, Roper, Affresh, Gladiator, Swash, Speed Queen and Hotpoint.

More than half of its principal products are sold in North America, with 23% sold in Europe, the Middle East and Africa. Latin America and Asia combined are 20% of sales. In India, Whirlpool has a 25% market share but faces stiffening competition. Whirlpool sells online and through retailers, distributors, dealers and builders. Its products include refrigerators, dishwashers, freezers, ice makers, refrigerator water filters, laundry appliances and accessories, cooking appliances, mixers and other domestic appliances.

Positioned for a turnaround

The fiscal year ending 2021 was the fourth all-time consecutive record year for Whirlpool. Revenue was up 13% to $22 billion. However, the second quarter of 2022, which ended June 30, was not so great. It recorded revenue of $5.097 billion, which was a 4.26% decline year-over-year. Whirlpool's revenue for the 12 months ending June 30 was $21.320 billion, a 2.07% decline year-over-year.

Despite the short-term trouble, on July 25, management increased its full-year earnings forecast, and the stock popped. The stock has been very volatile lately, though. Overall, it is down 32.64% over the past year and about 15% for the last five years. The short interest currently is over 11%, suggesting that short-sellers see further downside.

The company’s next earnings report is expected on Oct. 19.

Building greater market share

Management is focusing efforts to gain a greater market share. The company is expanding its online presence, making smarter appliances and continuing mergers and acquisitions.

Whirlpool signed a global agreement with Vtex (VTEX, Financial) in May 2021. Vtex is known as the world’s fastest-growing commerce platform. It brings Whirlpool native marketing and order management capabilities.

The company is heavily investing in its "6th SENSE" technology program, which lets its appliances intuitively learn from the owner’s uses and needs. For instance, freezers and ovens detect temperature variations, minimizing fluctuations and restoring them to optimal settings.

Whirlpool has acquired 10 companies and divested four over the past decade. In August, Whirlpool bought InSinkErator for $3 billion.

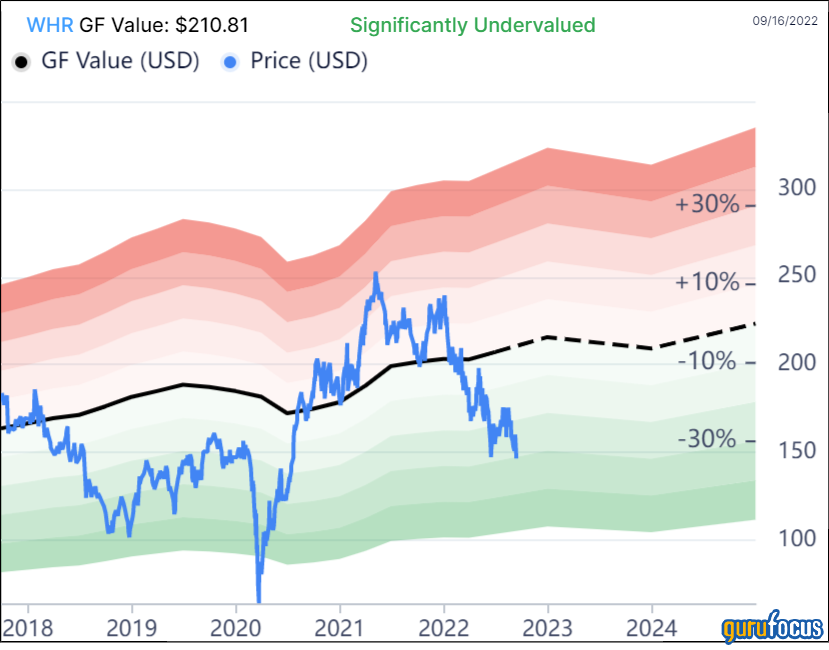

Valuation and sentiment

The GF Value chart rates Whilrpool stock as “Significantly Undervalued.” The GF Value is $210.76.

Whirlpool’s dividend is attractive, too. The forward dividend yield is 4.56% at the present time. That is a higher yield than 75% of the companies in the industry pay. It will cushion bulls' ability to hold shares for the long term.

The company’s overall GF Score is 91 out of 100. It ranks high for profitability, growth and value. Its financial strength and momentum rankings are softer but in healthy territory.

The price-earnings ratio of 13.11 puts the company in the top half of over 300 companies in its industry in terms of being undervalued. The price-sales ratio is 0.41, below 76.79% of peers, and its price-book ratio of 1.98 is in the bottom 61% of the industry. Whirlpool reduced its total debt from almost $7.86 billion in June 2021 to $5.85 billion in June 2022.

Hedge funds move in and out of the stock regularly. As a group, they increased their holdings in the stock by almost 155,000 shares last quarter following two consecutive quarters of reducing holdings. However, 33 funds owned shares in the first quarter of ’22, while only 24 owned shares at the end of the second quarter.

Looking ahead

Whirlpool is a legacy American company producing appliances that are in demand mostly because of brand name and quality recognition. Rising mortgage rates and rents are slowing new housing construction and lowering the moving rate of tenants, and those moving house are the primary consumers of new household appliances. Replacement rates for appliances are unlikely to change. Inventories of parts are smaller due to supply chain shortages. Parts and labor costs are rising, so oftentimes, it is cheaper to buy a new appliance.

The U. S. market is expected to grow at a compound annual growth rate of 4.4% (through brick and mortar locations) to 8.1% with smart home appliances leading the way. This bodes well for Whirlpool, though there is stiff competition from other brand name manufacturers and cheaper off-brands. The most significant headwind for Whirlpool naturally comes from the economy; if there is a recession, business could suffer.