Shares of Mastercard Inc. (MA, Financial) have fallen a little more than 6% year-to-date, which is better than the 14% decline in the S&P 500 Index. Despite not participating much in the general market correction, Mastercard still trades below its GF Value. By my estimations, this stock could offer an excellent risk-reward scenario for those investors looking for high-quality and undervalued stocks. Here's why.

Takeaways from recent earnings results

Mastercard last reported third-quarter earnings results on Oct. 27. The company’s revenue increased almost 16% to $5.8 billion while adjusted earnings per share of $2.68 showed 13% growth versus the prior-year’s period of $2.37. Both results were ahead of what analysts had anticipated.

For context, Mastercard’s revenue grew 30% and earnings per share improved 48% in the third quarter of 2021, so the most recent quarter was coming off one of the best comparable periods of the last five years for the company.

In local currency, gross dollar volumes improved 11% to $2.1 trillion, with the U.S. up 10% and the rest of the world growing 12%.

Cross border volumes, which are a lucrative business for Mastercard and other credit card companies, were higher by 44%, which was down from 58% growth in second quarter of 2022. The improvement in cross-border volume is an important mark for the company, led by air travel rates beginning to normalize against 2019 levels. European and North American air travel were still down 18% and 10%, respectively, from pre-pandemic levels, but this was an improvement over previous periods.

Though cross-border growth did decline somewhat on a sequential basis, outside of Europe, volume increased more than 50% from the previous year and travel-related volume is well above even pre-pandemic 2019 levels.

Mastercard did see a 17% spike in expenses for the period due to costs incurred from acquisitions, higher personnel expenses, advertising and data processing costs. However, the company’s adjusted operating margin expanded 100 basis points to 57.7%, showing that Mastercard’s spending isn’t impacting its ability to improve its profitability.

According to Morningstar Inc. (MORN, Financial), analysts expect Mastercard to earn $10.36 per share in 2022, which would represent growth of 18.3% from the prior year. Revenue is projected to grow 17.5% to $22.2 billion for the year.

A high-quality name trading below GF Value

Analysts expect that Mastercard will see double-digit growth for both revenue and earnings per share this year. This shouldn’t surprise those that follow the name as high teens growth on both the top and bottom lines has been a long-term trend enjoyed by the shareholders.

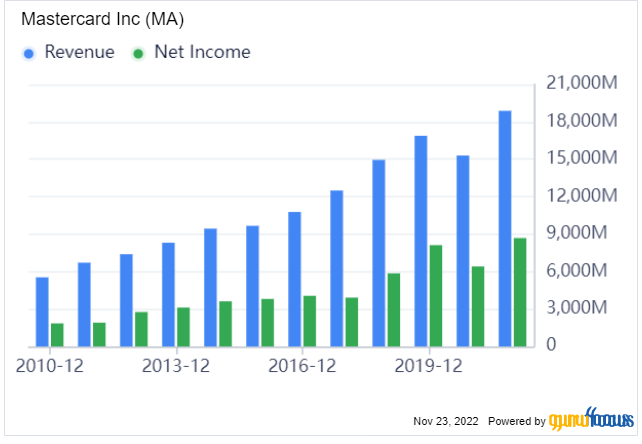

Aside from 2020, both revenue and net income have steadily increased for the vast majority of the last decade. This speaks to the strength of the business model and the quality name of Mastercard.

The company is one of the rare few with a GF Score of 98 out of 100:

Of the five components that comprise the GF Score, Mastercard receives a 10 out of 10 from GuruFocus in all but one area, financial strength.

The most impressive of these is on profitability, where the company ranks ahead of at least two-thirds of the competition and most metrics score near the top of the group. Mastercard’s return on invested capital (ROIC) is very close to the top of its peer group, showing that the company’s investment dollars are leading directly to bottom-line growth. This has helped the company be profitable every year for the last decade.

Growth is also a standout, driven by future revenue and earnings growth estimates for the next three to five years that are ahead of what Mastercard has seen over the last three years (data from Morningstar analysts). Companies with market capitalizations approaching $340 billion typically don’t grow at extremely high rates, but analysts are predicting that Mastercard will do just that.

Financial strength is the lone category where Mastercard doesn’t have a perfect score, but the company does have a solid score of 6 out of 10. The primary reason for this is that debt levels have increased dramatically. Mastercard had zero long-term debt on its balance sheet as recently as 2013, but that figure stands at nearly $14 billion as of the most recent quarter. The debt metrics, particularly cash-to-debt and debt-to-equity, are below two-thirds of peers and, more importantly, are at the lowest levels for the company in the last 10 years.

On the plus side, the company’s Piotroski F-Score is 8 out of 9, indicating that Mastercard is in strong financial position. The Altman Z-Score is very much in the safe reading, meaning that it is very unlikely that the company is at risk for bankruptcy. Mastercard’s ability to turn invested dollars into profits is once again reflected in the return on invested capital (ROIC) and weighted average cost of capital (WACC) scores of 42.5% and 8.8%, respectively.

The stock does sit at 33.6 times forward earnings estimates, but this isn’t too far off of its 10-year average price-earnings ratio of 30, according to Value Line.

Mastercard is trading at a discount to fair value according to the GF Value chart.

With a current share price of $348.64, Mastercard has a price-to-GF-Value ratio of 0.74, implying a possible return of 35% from current levels if the stock were to reach its GF Value. The stock offers a small dividend yield of 0.6%, but the dividend has doubled over the last five years.

Final thoughts

Mastercard continues to grow well as a dominant player in the U.S. payments processing industry. This is made more impressive by the fact that the company is lapping comparable periods where growth was especially high.

This type of performance has come to be expected from the company over the long-term and is made possible by its high scores on various fundamental metrics. This is likely to continue as revenue and earnings projections over the medium-term are ahead of what the company has seen over the past few years.

The stock is trading at a premium to its historical valuation, though the top- and bottom-lines are expected to grow at a higher than historical rate.

Given these factors, Mastercard would appear to have earned its premium multiple in my opinon Using the GF Value chart, the stock appears attractively priced and could lead to mid-30% returns by my estimates, giving Mastercard a good risk-reward profile.