Intel Corporation (INTC, Financial) designs, manufactures, and sells integrated digital technology platforms primarily in the Asia-Pacific, the Americas, Europe, and Japan. This dividend achiever has paid dividends since 1992 an increased them for 10 years in a row.

The company’s last dividend increase was in July 2012 when the Board of Directors approved a 7.10% increase to 22.50 cents/share. The company’s peer group includes Altera (ALTR, Financial), Xilinx (XLNX, Financial) and Advanced Micro Devices (AMD, Financial).

Over the past decade this dividend growth stock has delivered an annualized total return of 4.50% to its shareholders.

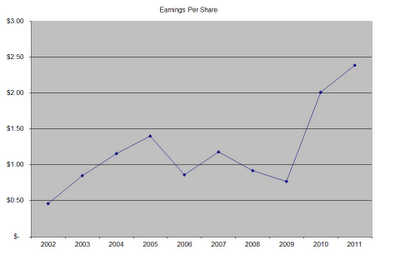

The company has managed to deliver a 20.10% average increase in annual EPS since 2002. Most of the increase came over the past two years however. Before that, earnings were following a rollercoaster pattern. Analysts expect Intel to earn $2.10 per share in 2012 and $2.03 per share in 2013. In comparison, the company earned $2.37/share in 2011.

The company is the dominant supplier of microchips for the computer industry worldwide. Its heavy investment in R&D have ensured that it maintains its dominant position in the market. Unfortunately, the market for traditional computers and notebooks is starting a long decline in units sold as more consumers are going mobile and embracing tablets. Intel has not been very successful in gathering a key position as a supplier of semiconductors for tablets and mobile phones. While shares are really cheap and trading at a super low P/E ratio, the real question is whether earnings will be flat over time or whether they will decrease. If earnings dip due to declines in PC sales and company’s inability to break into mobile, further growth in the dividend will be severely limited and it might even be at risk for a cut. Technology companies are notorious for being in an industry where rapid changes in products due to innovation lead to obsolescence and loss of consumers and revenues. As a dividend investor, I keep asking myself whether the dividend is secure, and whether I can rely on it for the next decade and beyond. While the yield is very high, I have strong doubts that the party would last for long. Even under the best case scenario, it looks like flat earnings would limit growth in distributions, but investors would still get paid a very respectable 4.50% yield for a few years. Shares might even double in value, mostly due to P/E multiple expansion. Of course, what happens if the market actually expects an EPS of $1/share by 2020?

That being said, given the fact that Intel is a market leader in the still very lucrative semiconductor market for PC’s, it has the scale to deliver product at a lower cost than competitors such as AMD. I doubt that the PC is going away, as I simply cannot foresee all businesses replacing computers with tablets. However, companies that end up selling less product than anticipated, might end up with extra inventory that might have to be written down. Inventory obsolescence is a particular concern for technology companies, because technology changes so quickly.

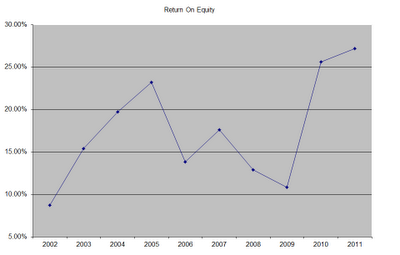

The return on equity has closely followed the trends in earnings per share over the past decade. Rather than focus on absolute values for this indicator, I generally want to see at least a stable return on equity over time.

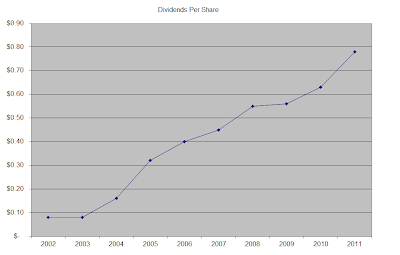

The annual dividend payment has increased by 25.60% per year over the past decade, which is higher than the growth in EPS.

A 25% growth in distributions translates into the dividend payment doubling every three years on average. If we look at historical data, going as far back as 1994, one would notice that the company had managed to double distributions every three years on average.

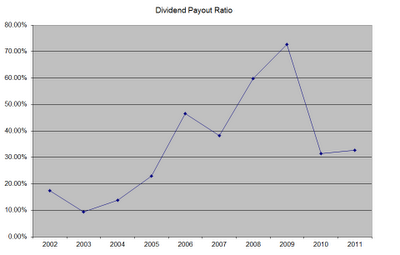

The dividend payout ratio has increased from 17.40% in 2002 to 72.70% in 2009, before reaching a more sustainable 32.60 % in 2011. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

Currently Intel is trading at 8.80 times earnings, yields 4.50% and has a sustainable distribution. Despite the ultra-low valuation, I am hesitant to pull the trigger on this one, due to my inability to determine whether Intel will be able to keep innovating and maintain profitability in the long run. Because of my inability to gauge whether tectonic shifts in technologies will impact the long-term picture for Intel, I will maintain a hold opinion on the stock. I am also unable to determine whether Intel will be able to boost earnings in the near term. That being said, the company’s shares can easily rebound from current lows, and its dividend yield would probably be sustained for the next several years. In addition, it also would add some exposure to technology for my income portfolio. While I am neutral on the stock, I plan on initiating a small started position by the beginning of next year, subject to availability of funds.

Full Disclosure: None

The company’s last dividend increase was in July 2012 when the Board of Directors approved a 7.10% increase to 22.50 cents/share. The company’s peer group includes Altera (ALTR, Financial), Xilinx (XLNX, Financial) and Advanced Micro Devices (AMD, Financial).

Over the past decade this dividend growth stock has delivered an annualized total return of 4.50% to its shareholders.

The company has managed to deliver a 20.10% average increase in annual EPS since 2002. Most of the increase came over the past two years however. Before that, earnings were following a rollercoaster pattern. Analysts expect Intel to earn $2.10 per share in 2012 and $2.03 per share in 2013. In comparison, the company earned $2.37/share in 2011.

The company is the dominant supplier of microchips for the computer industry worldwide. Its heavy investment in R&D have ensured that it maintains its dominant position in the market. Unfortunately, the market for traditional computers and notebooks is starting a long decline in units sold as more consumers are going mobile and embracing tablets. Intel has not been very successful in gathering a key position as a supplier of semiconductors for tablets and mobile phones. While shares are really cheap and trading at a super low P/E ratio, the real question is whether earnings will be flat over time or whether they will decrease. If earnings dip due to declines in PC sales and company’s inability to break into mobile, further growth in the dividend will be severely limited and it might even be at risk for a cut. Technology companies are notorious for being in an industry where rapid changes in products due to innovation lead to obsolescence and loss of consumers and revenues. As a dividend investor, I keep asking myself whether the dividend is secure, and whether I can rely on it for the next decade and beyond. While the yield is very high, I have strong doubts that the party would last for long. Even under the best case scenario, it looks like flat earnings would limit growth in distributions, but investors would still get paid a very respectable 4.50% yield for a few years. Shares might even double in value, mostly due to P/E multiple expansion. Of course, what happens if the market actually expects an EPS of $1/share by 2020?

That being said, given the fact that Intel is a market leader in the still very lucrative semiconductor market for PC’s, it has the scale to deliver product at a lower cost than competitors such as AMD. I doubt that the PC is going away, as I simply cannot foresee all businesses replacing computers with tablets. However, companies that end up selling less product than anticipated, might end up with extra inventory that might have to be written down. Inventory obsolescence is a particular concern for technology companies, because technology changes so quickly.

The return on equity has closely followed the trends in earnings per share over the past decade. Rather than focus on absolute values for this indicator, I generally want to see at least a stable return on equity over time.

The annual dividend payment has increased by 25.60% per year over the past decade, which is higher than the growth in EPS.

A 25% growth in distributions translates into the dividend payment doubling every three years on average. If we look at historical data, going as far back as 1994, one would notice that the company had managed to double distributions every three years on average.

The dividend payout ratio has increased from 17.40% in 2002 to 72.70% in 2009, before reaching a more sustainable 32.60 % in 2011. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

Currently Intel is trading at 8.80 times earnings, yields 4.50% and has a sustainable distribution. Despite the ultra-low valuation, I am hesitant to pull the trigger on this one, due to my inability to determine whether Intel will be able to keep innovating and maintain profitability in the long run. Because of my inability to gauge whether tectonic shifts in technologies will impact the long-term picture for Intel, I will maintain a hold opinion on the stock. I am also unable to determine whether Intel will be able to boost earnings in the near term. That being said, the company’s shares can easily rebound from current lows, and its dividend yield would probably be sustained for the next several years. In addition, it also would add some exposure to technology for my income portfolio. While I am neutral on the stock, I plan on initiating a small started position by the beginning of next year, subject to availability of funds.

Full Disclosure: None