S&P 500 is trading at low price multiple to expected earnings, 13.7 according to WSJ. The historical forward P/E has been in the range of 14-16, depending on how far you look back. With interest rates incredibly low, 3.88% on the 10-year, should make the fair-value multiple even higher.

According to my calculations, the S&P 500’s mean P/E = 14.2 and median = 13.2. Thirteen companies were excluded due to negative earnings. The highest P/E was 90, and only ten firms had multiples greater than 30. The chart shows the frequency distribution of the individual firm’s P/Es constituting the index.

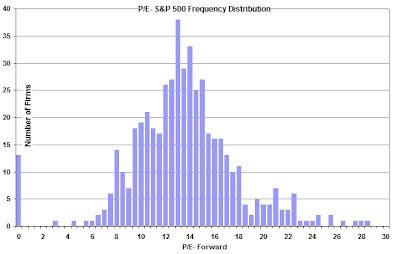

So is the market cheap? The low price multiples suggest that it is.

The Consensus estimates point to a strong recovery. According to Thompson, Analysts predict earnings to jump 15.3 percent this year.

In my opinion, that magnitude of growth is wildly optimistic. The Market isn’t buying it either. It’s not that the market is cheap, it’s that investors believe consensus estimates are too high. Why do I think that? Because if the market had full confidence in the forecasted numbers, I doubt the market would trade at these multiples. Hence, investors are pricing in lower earnings than the consensus forecasts thus making multiples higher.

The most probable outcome will be downward revisions to the earnings estimates. It’s possible that some of the consensus numbers are stale, meaning analysts have been slow to update them. This seems plausible given the current environment of uncertainty, and the inherent lack of visibility, may delay updates to estimates. In some cases, analysts may be waiting for a clearer picture going forward, or updated guidance from firms before making revisions to this and next years’ full year estimates.

Another possibly is that the required rate of return investors demand from equities rose, the “Equity Risk Premium.” This implies that the Market perceives increased risk inherent in the equity markets. This seems plausible since volatility has increased relative to years past. Higher perceived risk leads to higher demanded returns which compresses price-earnings multiples.

In my opinion, stocks are not as cheap as forward multiples suggest. Earnings estimates are too high and are likely to come down. In addition, the ERP has increased pinching multiples. However, if the economic slowdown begins to appear less severe as the Market is expecting, then stocks would be rather cheap. That would mean that analysts are not overestimating future earnings. However, given the turmoil in the housing market and the relationship to consumer spending, it’s likely the coming quarters will be weak.

_____________________

Source: Financial Alchemist

According to my calculations, the S&P 500’s mean P/E = 14.2 and median = 13.2. Thirteen companies were excluded due to negative earnings. The highest P/E was 90, and only ten firms had multiples greater than 30. The chart shows the frequency distribution of the individual firm’s P/Es constituting the index.

So is the market cheap? The low price multiples suggest that it is.

The Consensus estimates point to a strong recovery. According to Thompson, Analysts predict earnings to jump 15.3 percent this year.

In my opinion, that magnitude of growth is wildly optimistic. The Market isn’t buying it either. It’s not that the market is cheap, it’s that investors believe consensus estimates are too high. Why do I think that? Because if the market had full confidence in the forecasted numbers, I doubt the market would trade at these multiples. Hence, investors are pricing in lower earnings than the consensus forecasts thus making multiples higher.

The most probable outcome will be downward revisions to the earnings estimates. It’s possible that some of the consensus numbers are stale, meaning analysts have been slow to update them. This seems plausible given the current environment of uncertainty, and the inherent lack of visibility, may delay updates to estimates. In some cases, analysts may be waiting for a clearer picture going forward, or updated guidance from firms before making revisions to this and next years’ full year estimates.

Another possibly is that the required rate of return investors demand from equities rose, the “Equity Risk Premium.” This implies that the Market perceives increased risk inherent in the equity markets. This seems plausible since volatility has increased relative to years past. Higher perceived risk leads to higher demanded returns which compresses price-earnings multiples.

In my opinion, stocks are not as cheap as forward multiples suggest. Earnings estimates are too high and are likely to come down. In addition, the ERP has increased pinching multiples. However, if the economic slowdown begins to appear less severe as the Market is expecting, then stocks would be rather cheap. That would mean that analysts are not overestimating future earnings. However, given the turmoil in the housing market and the relationship to consumer spending, it’s likely the coming quarters will be weak.

_____________________

Source: Financial Alchemist