Before I reveal the name of the stock I am going to discuss today, I would like to lay out the facts. First, it is a retailer growing its e-commerce sales from 6% of total net sales in fiscal year 2008 to 12% of total net sales in fiscal year 2013. Second, it has already spent $44 million in highly automated distribution and fulfilment centers and information systems to support future growth. This infrastructure investment can support the company to expand into a national retail footprint of 500 stores from 203 stores today. Third, it has $57 million cash compared to the market cap of $225 million. The cash represents around 25% of the total market cap valuation. Forth, it pays 3.8% dividend yield. Now, let me reveal the name of this attractive stock, Tilly's (NYSE:TLYS). I will further illustrate the lucrative potential return of 100% and discuss what my base scenario will be for TLYS.

Company Overview

(click to enlarge)

Source: Company Website

TLYS operates about 206 stores in 33 states and is a leading specialty retailer in the action sports industry selling clothing, shoes and accessories. Its main target customers are teenagers. TLYS offers one of the largest assortments of brands and merchandise from the top players in the surf, skate, motocross and lifestyle apparel industries available both in stores and online at tillys.com. It was founded in 1982 and is headquarterd in Irvine, California.

Why did TLYS decline to today's depressed level?

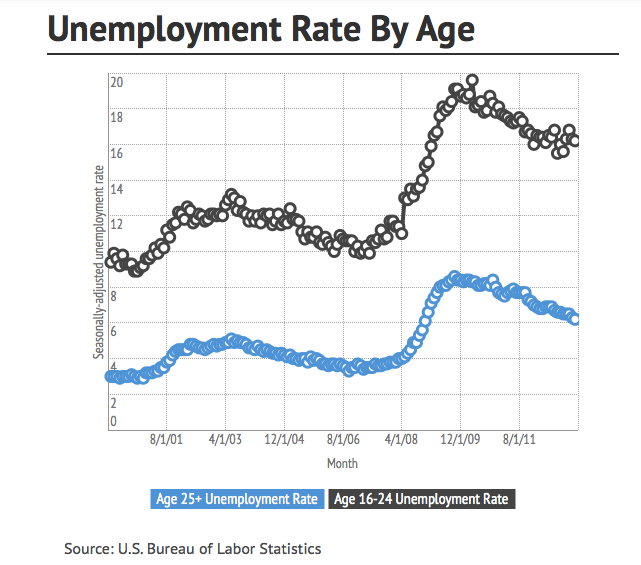

As almost all retailers are struggling in today's highly promotional environment, TLYS is no exception. In fact, it is even worst for TLYS since its core customers are teenagers, who are under even more stress since teenagers'Â unemployment rate is higher as shown in the chart below:

(click to enlarge)

Furthermore, the comparable store sales, which include e-commerce sales, decreased by 7.1% in Q2 2014 compared to the prior quarter in 2013. If we look further into the trend of comparable store sales, TLYS has already gone through several negative comparable store sales growth. With the share price of TLYS near its 52-week low, I believe that the downward comparable sales trend has already been reflected in the share price. If the economy continues to recover, there is a good chance that the profit margins of TLYS can rebound, which I will discuss more in the valuation section.

Valuation

| In Millions of USD | FY 2007 | FY 2008 | FY 2009 | FY 2010 | FY 2011 | FY 2012 | FY 2013 | FY 2014 | Current/LTM |

| Margin % | 15.74 | 16.23 | 9.26 | 7.38 | 7.34 | 8.57 | 5.11 | 3.66 | 2.70 |

The net margins of TLYS have been in a downward trend. As we all know, the sales environment for teenagers is dismal. Some might argue that the terrible sales trend will continue. However, we have to consider the fact that TLYS doubled its e-commerce sales for the past 5 years, invested $44 million in distribution infrastructure and had 25% of market value in cash. All these positive factors should help to support the current share price regardless of further weakness in sales or margins. On the other hand, how about the teenager spending recovers? Or TLYS can catch a fashion trend in the future and sell its products at significant high margins. I believe that the possibility of a rosy outlook warrants consideration, too.

For my best-case scenario, I assume that TLYS maintains its current 3% net profit margins without any improvement in margins due to the highly promotional retail environment. With consensus sales forecast to grow by 10%, TLYS can generate around $550 million sales next year. The net profit will become $16 million. Given the enterprise value of $170 million, TLYS currently trades at around 10x earnings relative to the enterprise value. Taking into account the fact that TLYS has relatively low margins and still experiences downward pressures in both sales and margins, I assign 14x earnings multiple instead of 16x. My target price is $10.5, implying 30% upside potential.

As a side note, I chose to use enterprise value instead of market value since TLYS has 25% cash. TLYS can utilize cash to repurchase its own shares in the future.

For reference, Zumiez (NASDAQ:ZUMZ) is a close competitor to TLYS. ZUMZ demands 6.22% net profit margins, relative to around 3% net profit margins for TLYS. Although I admit that the business model of ZUMZ is different from TLYS, comparing ZUMZ directly with TLYS should be performed carefully. Nevertheless, TLYS can improve itself through learning more about the strategies from ZUMZ. One thing I notice is that TLYS has already made changes in its business plan to gain operation efficiency. For example, one of the major deference between TLYS and ZUMZ is store size. As a result, TLYS implemented a new strategy to lower the size of the new stores so as to increase sales per store square feet. I believe that this is a positive development with the potential to increase profit margins for TLYS.

For the bullish case scenario, TLYS can revert back to 6% net profit margins. With $550 million expected sales and 14x PE multiple, TLYS can be worth $460 million, which is 100% upside potential. Although it is difficult to foresee such bullish scenario to become reality today, we should not rule out the possiblitiy for TLYS to catch a fashion trend and demand industry comparable 6% net profit margins for a good period of time. If that happens, TLYS has the potential to double itself.

Source: Company Presentation

From another perspective in regards to Free Cash Flow "FCF," TLYS forecast to have about $26 million in capital expenditures in 2014, which is reverted back to its mean after heavy capital expenditure to develop e-commerce platform and store expansion for the past two years. With the capability of TLYS to generate $44 million cash flow from operations, TLYS will generate about $18 million FCF, which results in about 10x EV/FCF.

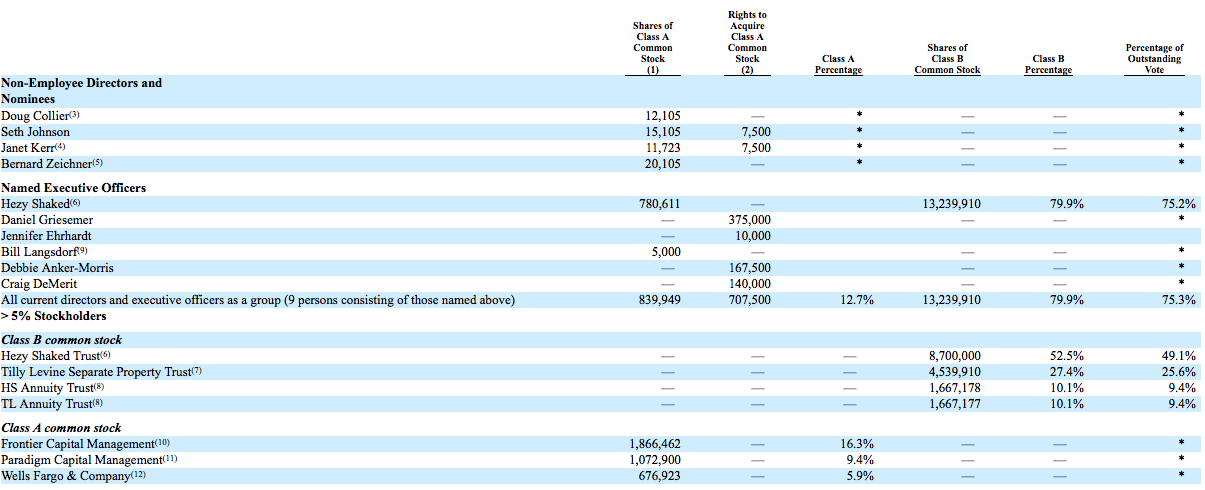

Management Team

(click to enlarge)

Hezy Shaked, as a founder, has in-depth knowledge about TLYS. Plus, he has 29 years of experience in the retail industry. Hezy Shaked, who is the current CEO and the chairman of TLYS, owns 75.2% of shares of Class B common stock. The Class B common share has ten votes per share. Hezy Shaked has the controlling stake in TLYS through its Class B common stock. This might pose some hesitation for prospective investors as they know their influence as a minority shareholder is very limited. However, companies run by founders can be good too. For example, TLYS invested $44 million in distribution infrastructure. I believe that only if TLYS is run by owner mindset, such big investment with long time benefit will be made and not replaced by some short-term projects with immediate profit incentives. All in all, I believe that the benefit of founder owned companies can sometimes outweigh the negativity derived from less influence imposed by shareholders.

In addition, directors and executive officers together own 12.7% Class A shares. The ownership is significant and indicates that insiders have positive outlooks for TLYS.

Risks

First, the sales and profit margins of TLYS can continue their downward trajectories. Plus, the economy can fall back into recession if there is a war or any adverse events triggering economic downturn. Second, the strategy of TLYS having a big store size and expanding from the West Coast throughout the nation might not be attractive to its targeted customers and can be proven to be unprofitable. Although TLYS implemented new strategies to improve probabilities, it is still too early to draw a conclusion. However, TLYS has been profitable since its IPO and has around 25% in cash to weather any unexpected downturns. This should help to mitigate the business risk investing in TLYS. Third, the fashion trend is very difficult to forecast, and the business nature of TLYS is volatile. Therefore, TLYS is more suitable for high risk tolerant investors.

The bottom line

TLYS is a risky investment due to the business nature as a teenager retailer. However, TLYS provides a favorable risk/reward profile. As I mentioned above, TLYS has the potential to double if TLYS can demand 6% profit margins, which is not out of reach for TLYS. The downside risk of TLYS can go towards $5.5 per share, close to the book value of TLYS. But as long as TLYS can maintain a reasonable amount of cash on hand and remain cash-flow positive, it is difficult for me to foresee that TLYS trades close to 0.3x sales in the future. All the positive traits of TLYS should help TLYS to rebound soon even if it declines to its book value temporarily. In conclusion, I believe that the risk/reward profile is very favorable for high-risk-tolerant investors with the patience to navigate through today's brutal retail environment.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.