It is no secret that the retail environment is brutal nowadays. However, the current earning disappointments present great investment opportunities for those investors willing to look through the current headwinds. In fact, everything goes through a cycle, and the retail industry is just going through a down cycle. Today, I would like to share my new finding, Ascena Retail Group (ASNA). It is a retailer with a focus on female shoppers and a 40% upside potential, even under my conservative assumptions. I believe that this investment is worth exploring further, and my analysis below should help provide more insight.

Business Overview

Ascena Retail Group is a leading national specialty retailer of apparel for women, and tween girls and boys. It operates under various brands including Justice, Lane Bryant, Maurices, Dressbarn, and Catherine's.

ASNA targets the female shoppers with extensive age ranges. Justice targets tween girls and boys at about age seven. Maurices targets young adult customers, and Lane Bryant, Dressbarn, and Catherines serve female shoppers age 33 and above.

As most retailers are now focusing on omni-channel, ASNA is working hard on improving its omni-channel, too. ASNA currently derives only 10% of sales from e-commerce. This indeed gives a lot of room for the e-commerce to expand as ASNA has already budgeted for the investment into omni-channel. As e-commerce takes a bigger share of total sales, it will help to drive further sales growth in the future.

The Disappointing Guidance

Although it is disappointing to hear the lowered EPS guidance in the range of $0.90 to $1 in 2015, it is good to hear the management team mention that they were done with the markdown, and the inventory was in a good shape. This helped to give comfort to investors that there might not be any further deterioration in the profit margins in the near future. In addition, ASNA executives expected the gross margins rate growth across all five brands, and they even went deeper to point out that freight synergies were the main contributor for the gross margin rate improvement.

What's more, if we pay attention to the same store sale figures, it might be a concern for prospective ASNA investors. The same store sale figures have recently turned negative for the previous few quarters. This has reversed the upward trends in same store sales established since 2009. As the negative same store sales can be a good indicator for any business deterioration, I will continue to pay close attention to it and see whether it can trend positively any time soon.

Normalized Free Cash Flow is Attractive

ASNA is expected to have capital expenditures of about $350 million next year for the normal business need and the roll out of new omni-channel. That is a big drop from the $480 million capital expenditure in 2014. As my expected cash from operation is about $380-$400 million, the free cash flow will be very small relative to the historical average around $180 million. But fortunately, ASNA CEO David Jaffe gave hints that the capital expenditure will be normalized below $300 million in 2017. Once the capital expenditure drops back to below $300 million, together with the cost synergies going into effect, I am confident that ASNA should return back to its free cash flow average of approximately $180 million, which implies more than 8% free cash flow yield.

ASNA has an owner-operated mindset. Once the capital expenditure comes to its normal level, ASNA should start to pay down debts. Longer term, future share repurchases should be a viable option to return capital back to shareholders. As the Jaffe family owns close to 20% of the outstanding shares, their interests should be well aligned with ASNA shareholders.

Self-Help Cost Savings Plan

According to the latest conference call, ASNA delivered $23 million in combined synergy savings and overhead reductions versus the guidance of $18 million. The management team forecasted that there will be long-term savings from synergies and overhead reductions at $100 million, which is net of depreciation in 2016. To put this into context, the cost savings plan should help ASNA to move closer to its operating margin goal of 10% from the 5.5% operating margin in 2014.

Other than cost savings, ASNA's new distribution center in Etna, Ohio can dramatically shorten the distribution time. This will assist the stores in receiving updated merchandise and respond more quickly to fashion trends. I expect that this will drive more sales volume in addition to lower costs due to the distribution center consolidations.

Valuation

I would like to project my valuation in 2016. I assume that ASNA can grow its sales by 3% per year. Based on historical EBITDA margins ranging between 9.4% and 14%, I conservatively assume that ASNA would attain 10% EBITDA margins in 2016. Please note that ASNA has an internal goal to achieve 10% operating margins compared to approximately 5.5% operating margin in 2014. Relatively speaking, my 10% EBITDA margins might underestimate the earning capacities of ASNA. However, due to the current disappointing 2015 guidance, I would like to use more conservative margins until better outlook can be provided. Combined with a slightly below industry 7x EV/EBITDA ratio, the enterprise value of ASNA can trade up to $3.5 billion. This implies approximately 40% upside potential under my conservative assumptions.

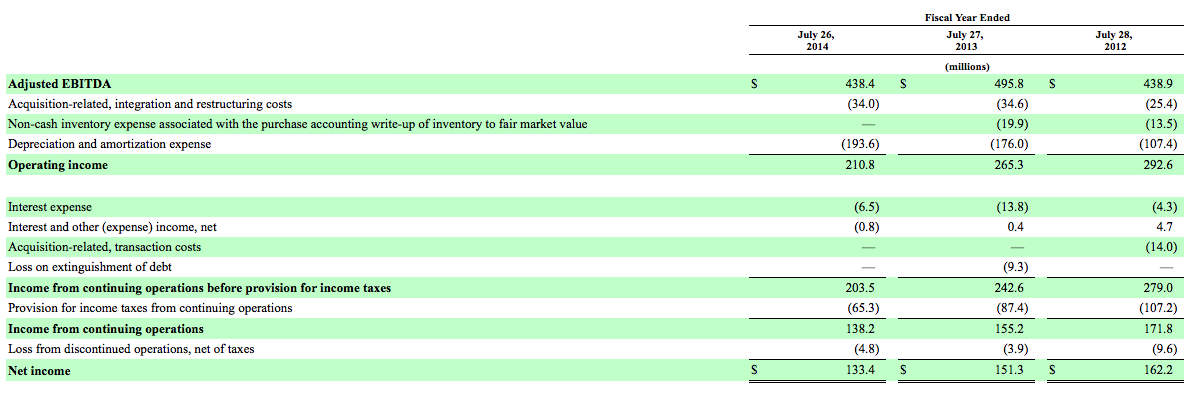

From another perspective focusing on the EBITDA, the below 10K provides the historical EBITDA data:

(click to enlarge)

Source: 10K

As we can see from above, it is reasonable to assume that ASNA can attain $500 million EBITDA in 2016 as ASNA had $438 million adjusted EBITDA in 2014, $495 million in 2013, and $438 million in 2012.

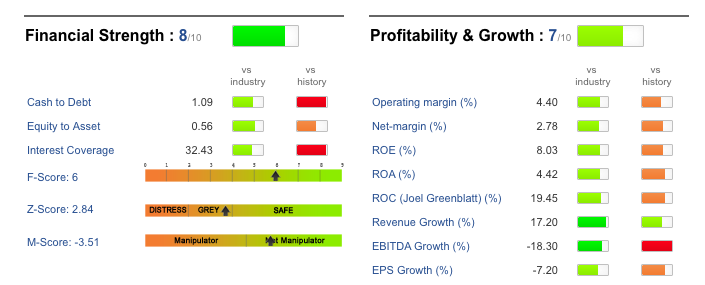

Financial Strengths

ASNA has $172 million in debt. With EBITDA $435 million and expected normalized $180 million free cash flow, the leverage ratio is very low. The high financial strengths are further confirmed by GuruFocus' financial strength indicator below:

(click to enlarge) Source: gurufocus.com

Source: gurufocus.com

Management Team

Experienced Management Team with "Skin in the Game:" Ascena's Management team is the classic example of a non-promotional, owner-operator looking to build wealth over the long term versus near-term earnings. Management collectively are the largest shareholders of ASNA, with a ~20% stake, aligning interests with long-term shareholders. Importantly, since the management team is vested, they are incentivized to be smart with the cash, primarily utilizing excess cash flow for accretive acquisitions (growing the business from one portfolio company, Dressbarn, into a retail platform) and share buybacks, forgoing tax-inefficient dividends, which eliminate the common shares from ownership by certain investors.

The above summarizes the management team well. ASNA is owner-operated with a long-term view aligning interest with shareholders.

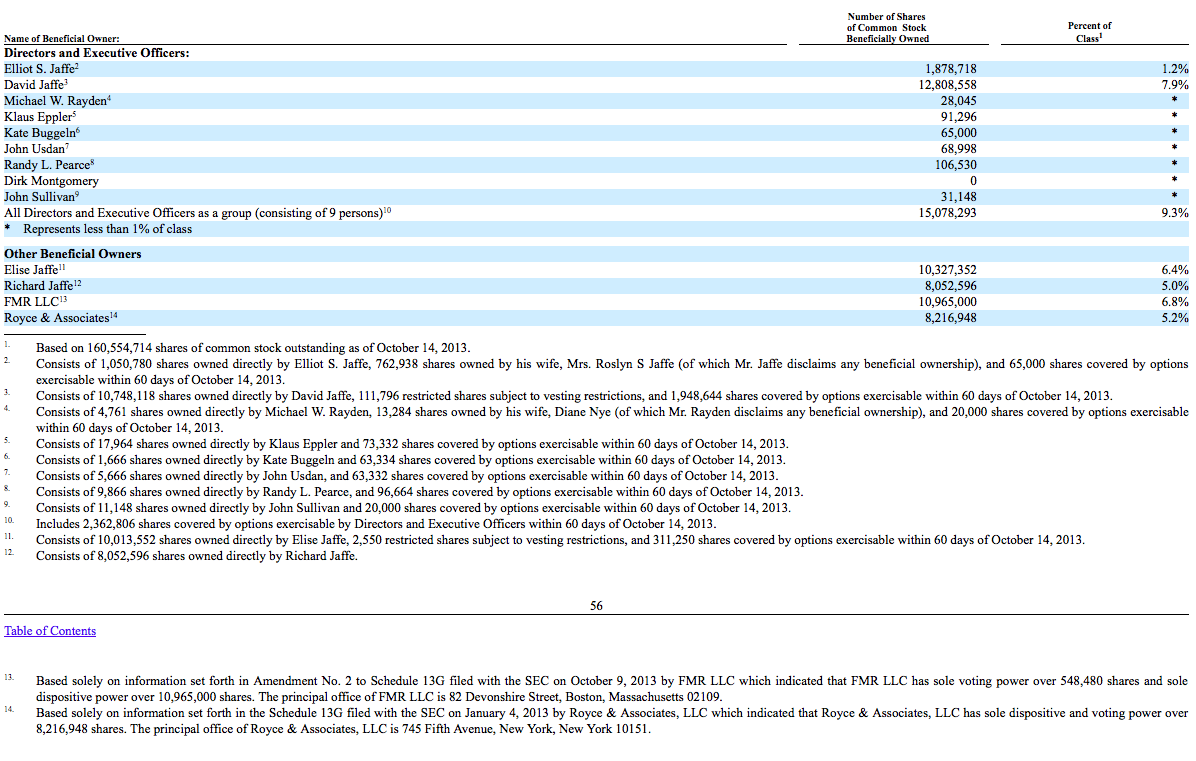

(click to enlarge)

Source: Proxy Statement

Through the latest proxy statement, we can further confirm that Elliot Jaffe, the co-founder and chairman of ASNA, owned 1.2% outstanding shares, and David Jaffe, the CEO of ASNA, owned 7.9% outstanding shares. In addition, the Jaffe family, including Elise Jaffe and Richard Jaffe, owned 6.4% and 5.0% outstanding shares respectively. The combined ownership of the Jaffe family was close to 20% of ASNA.

Elliot Jaffe co-founded ASNA in 1962 and served as its CEO from 1966 to 2002. Afterward, he passed the CEO role to his son, David Jaffe, who continues to lead ASNA. On one hand, we might question whether David Jaffe is the most suitable candidate to run ASNA since David inherited the CEO role from his father. On the other hand, ASNA is run with the owner mindset. The Jaffe family would like to see ASNA to do well in the future, which is well supported by their significant share holdings in ASNA. Further assessing the pros and cons, I believe that the benefits of the Jaffe family running ASNA might outweigh the negatives.

Risks

First, the cost reduction program might be delayed or not achieve the anticipated results. Plus, ASNA is still integrating the Lane Bryant and Catherine's brands. All of those initiatives involve execution risk. Second, ASNA might do dilutive acquisitions in the future and adversely affect shareholder interest. Nevertheless, such acquisition dilutive risk is low given that the Jaffe family has significant shareholder interest. Third, the current highly promotional retail environment might persist longer than expectation. This will further put pressure on the margins and sales of ASNA. Fourth, please refer to the risks section of the 10K to further understand the business risk investing in ASNA.

The Bottom Line

Since ASNA has already demonstrated its capabilities to improve profit margins for the Justice brand after its acquisition, investors should have faith in the integration of the Lane Bryant and Catherine's brands. Although it is inevitable that there might be hiccup in the process, I still believe that ASNA will finally improve its profit margins, and ASNA should be worth much more than today. For long-term investors, the potential 40% upside should be enough to compensate for the current headwinds. Indeed, if ASNA can catch the fashion trend in the future, my 40% upside potential might even prove to be conservative. As a result, I will recommend prospective ASNA with long term investment horizon to seriously consider investing into ASNA.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.