Trigon Agri (TAGR, Financial) is a farming operator and land investor active in, of all places, Ukraine, Russia and Estonia. The market has been dumping pretty much anything Ukraine or Russian because of the widely publicized situation surrounding Crimea. Trigon Agri was already performing atrociously leading up the 2014 Crimea crisis but continued to sell off and is now worth next to nothing with a market cap of just $18 million. Its enterprise value, however, is over $100 million, and its net asset value, by my estimate, $73 million. Originally Trigon Agri was started by Trigon Capital with $20 million of capital in 2006. Joakim Helenius is executive chairman at Trigon Capital and still chairman at Trigon Agri.

Trigon Agri strategy is to vertically integrate with an objective of achieving cost leadership. It starts with the acquisition of farmland and former collective farms in Russia, Ukraine and Estonia. Then Trigon Agri brings in modern agricultural technology and the latest farm management techniques. Trigon Agri also does follow-on storage, sales and even engages in trading, all in-house, in order to maximize prices for the produced commodities. The infographic below shows the entire process from buying land to grain trading:

Source: Trigon Agri, corporate website

To achieve cost leadership Trigon Agri buys farmland in concentrated blots. It builds up land concentration within 75 km of its grain elevators and accessible by road or rail. When the company can put together large land clusters of 80,000 hectares, it allows it to achieve economies of scale and work toward a cost leadership position.

Financial strength

The company’s financial strength is a very interesting subject. The company sat down with its creditors and amended the terms of its facilities, and the bondholders voted unanimously to extend the maturity of the bonds to August 2017. The reason bondholders aren’t eager to have the company default and sell off its assets is that this will result in pretty much a worse situation than they are in right now. The company is already trying to sell its Russian assets but has very little success due to the tension between Russia and Europe over the Russia-Ukraine conflict. There are currently only Russian buyers. If the company goes bankrupt those assets still can’t be sold and the creditors may end up having to operate an agricultural company. Therefore I believe creditors want the company to continue operating so they aren’t stuck with assets that are, at this time, very problematic to sell.

Management

Joakim Helenius is chairman of the board. Helenius is also the founder and executive chairman of Trigon Capital. He co-founded Trigon Capital in 1992 which is a leading investment bank in the CEE region with offices in Estonia, Latvia, Lithuania, Poland and Russia. In 1994 Helenius started what is today’s largest direct investment fund in the Baltics. It’s called the Baltic Republics Fund. Helenius also manages TDI. TDI invests in startups in the CEE region.

Executive management is in the hands of Ulo Adamson, president and CEO of Trigon Agri. Adamson became COO at Trigon Agri straight out of the Stockholm School of Economics and became president nine years ago. His whole career revolved around Trigon Agri so he knows the company very well.

Overall, I’m happy that management consists of experienced capital allocators and it turns out it also aligned its interests with that of shareholders; Trigon Capital holds 7.8% shares in Trigon Agri. Currently, Trigon Capital manages Trigon Agri under a management agreement. As of 2016 the management agreement will be cancelled and Trigon Capital's team will be directly employed by Trigon Agri. Trigon Capital also manages a Russia fund, which tells me they know the country very well. Well-incentivized management is important to me and in this situation I view the management situation as favorable to an investment.

Valuation

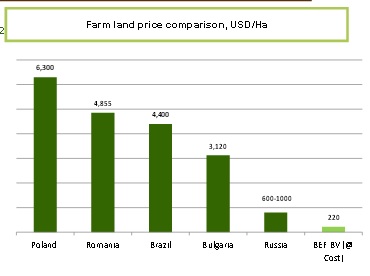

The value of Trigon Agri lies in its land as opposed to its operations. The company has 144,000 hectares of land under its control and 92,000 hectares in registered ownership. Competitor Black Earth Farming compared prices of Russian farmland to prices in other underdeveloped countries. Some are geographically very close to where Trigon’s farmland is located. If you look at these, it’s obvious politics have an effect on land values because this land yields are similar.

Source: BEP

Trigon owns land in Russia which is located in the Southern district and the Volga district. Prices here are significantly above average but still trades at a huge discount compared to Bulgaria and Romania just across the Black Sea. My estimate is that the company’s Russian-owned land is worth approximately $1,200 per hectare. This is a rough estimate based on quoted prices, observed values and the company’s description of the quality of its land. I believe it is a conservative estimate. The company also has control (shared ownership) of a number of hectares. These hectares can be converted to owned land through a highly bureaucratic process that takes at least a year. When the right manpower with knowledge of Russia’s system and time is allocated to this task, it can be done and the land is owned. For now I’ll apply a discount of 66% to the controlled land. The company has its land on the balance sheet at a slightly lower price, but in my view the net asset value of the company is very close to something like this:

| Value land in registered ownership | $110 million |

| Value land under control | $20 (potentially worth $60 when owned) |

| Cash, receivables, inventory: | $30 |

| Total assets | $160 |

| Total liabilities: $87 million | $87 |

| Total net asset value | $73 |

| in million USD |

Source: authors estimates

With the entire market cap of Trigon Agri at just $18 million there is plenty of room for a double or even a multi-bagger just by the stock recovering to net asset value. If the political situation in Russia improves over the next 10 years and the discount to Bulgarian land (the next cheapest farmland) disappears, that is another potential double.

Risks

Where to start? Trigon Agri is a commodity player so it is exposed to commodity price risk. The company is active in Russia and Ukraine, which exposes it to political risk. Shareholder rights in Russia are not as rock solid as they are in the U.S. and even in the U.S. government doesn’t always respect shareholder rights. There is the risk of the armed conflict between Russia and Ukraine escalating again. The company’s lands or facilities could be damaged or seized. It’s possible the company is the victim of sanctions from the world against Russia or from Russia against the Ukraine. There is the risk of the company not being able to sell off assets and or generate sufficient cash to repay bondholders and they will after all have the company in default.

There is enough to scare the bravest of investors but these risks should also be put in perspective. The company has an incredibly amount of hectares of farmland on its books in strategic positions. Crops and facilities can be damaged by war but land will survive. Bondholders can sell off assets but probably not all assets. There are so many hectares on the books.

Outlook

A heavily indebted farming company in the middle of a war zone may not immediately appeal to everyone. What does appeal to most people is an investment with limited risk and a +100% upside. Surprisingly, Trigon Agri AS fits both profiles. Trigon Agri has secured enough working capital for the 2015 season, but many farmers are struggling because of the political instability and the effect this has had on commodity prices. This may drive some smaller competitors out of business which will drive prices higher. Trigon Agri, meanwhile, aims to avoid diluting shareholders, focuses on core assets and sells non-core assets. It's going to pay off debt with the non-core asset disposal and go to a debt-free position. Further management wants to roll out irrigation infrastructure on the farmland in Russia and Ukraine which will allow the company to grow higher margin crops. For the foreseeable future its likely tension between Russia and Ukraine remains and investors can expect a highly volatile stock price.

Edit: I've edited the article 6-3-2015 to reflect the answer I received from Trigon Agri asking whether Trigon Capital still held a stake and new information about the management agreement.

Disclosure: Schildpad & De Haas Investments CV is invested in Trigon Agri. We have no intention of trading the stock anytime soon but reserve the right to do so at any time and without warning.