When I saw the Real-Time Pick from Chuck Royce (Trades, Portfolio), as tracked by GuruFocus, in Perceptron (PRCP, Financial), I was sceptical. Come on, a company called Perceptron? That sounds too much like the Transformers. I never forgot Peter Lynch's advice to always go for the companies with boring names. Don’t go for the -trons, but the Pep Boys & Mannies (PBY) of the world. Even so, I dutifully decided to check it out, and what I found was remarkably interesting.

Royce Investments is a small cap specialist boutique targeting mainly companies with market caps of up to $5 billion. They are very much a value-oriented fund, so this pick is a little bit surprising.

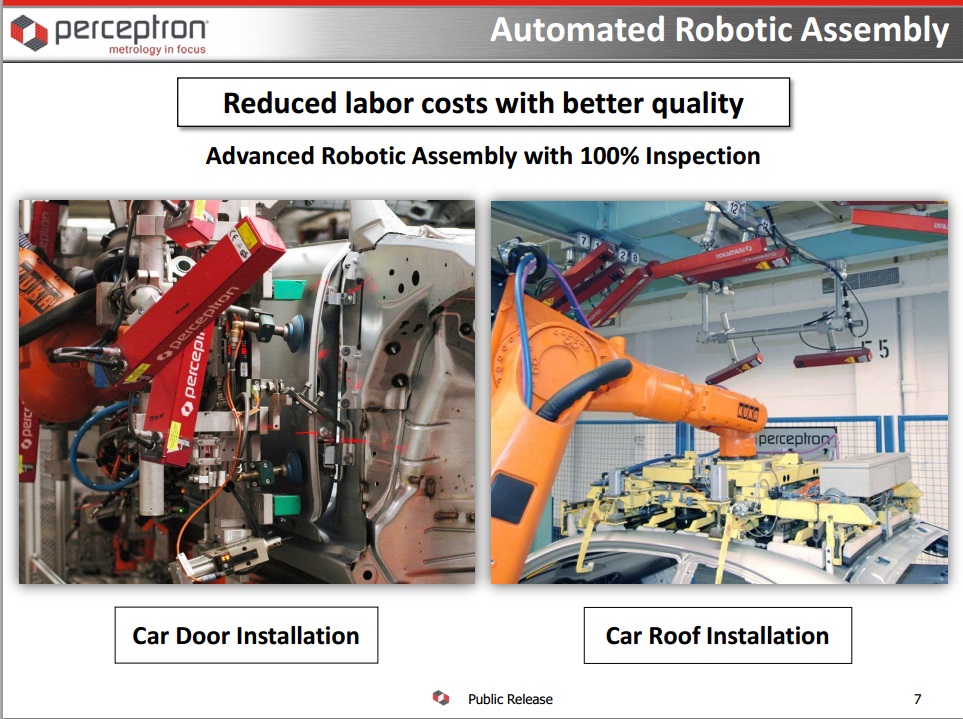

Perceptron makes robots for the automotive and aerospace industry among a few other things. So, there is some Transformers going on here. These robots, however, are already useful at the present. Even though this is a company with a $70 million market cap and an even lower enterprise value, it’s not a start-up with an unusable product.

The price of the stock declined sharply over the past year, perhaps due to the first two acquisitions the company has made in its 15-year history:

- Coord3 Industries s.r.l, a mid-market designer and builder of a full range of high-quality and high-performance coordinate measurement machines (CMMs), based in Turin, Italy.

- Next Metrology Software s.r.o., a technical leader in CMM operating software and the developer of TouchDMIS, based in Prague, Czech Republic.

A few signs of a bad investment are there: glamour industry and multiple acquisitions (integration risk) just behind it. However, investors have been chewing the acquisitions over and the share price already declined. Therefore, that risk is pretty much priced in. At the current price, we are paying 16x forward earnings according to the average Reuters analyst estimate. That’s a little bit below the S&P 500 average and the industry average. On that basis alone, the stock isn’t particularly undervalued.

Is the balance sheet representative of the average S&P 500 company or the average company within its industry? I think not.

The company holds almost $14 million in cash and no long term debt. If you adjust for cash, it trades at just a 12.8x forward earnings multiple. If its forward earnings turn out to be sustainable, it could lever up the balance sheet while staying within a conservative ratio and create a lot of value for shareholders.

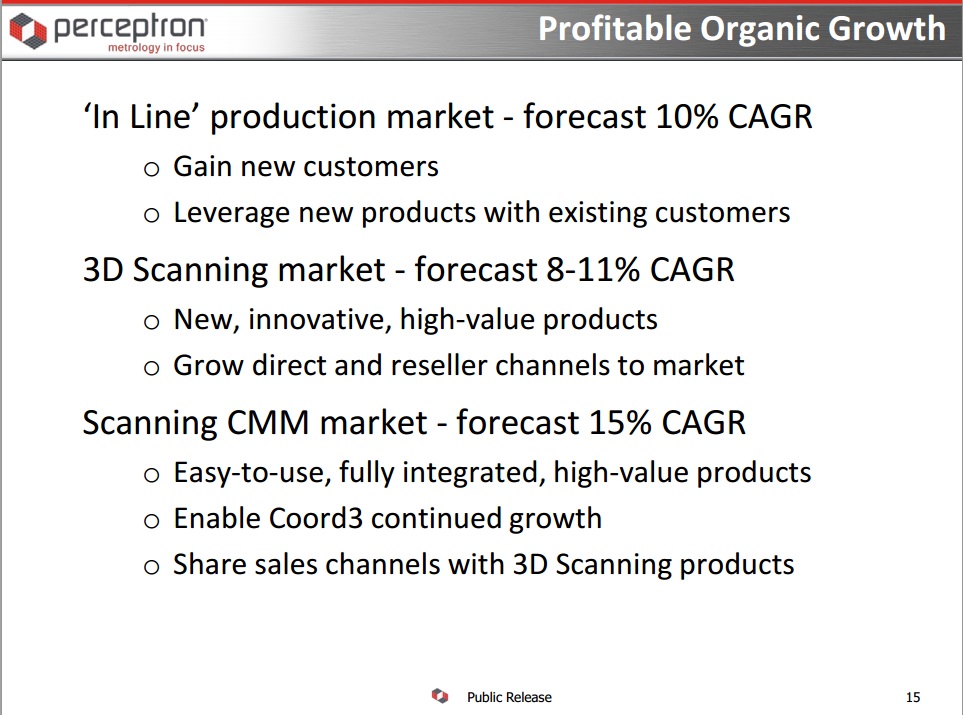

Another interesting point is that the company isn’t just average in growth prospects either. It’s obviously smack in the middle of a glamour industry because it is a growth industry. The problem with glamour industries, and why the returns on these stocks tend to be bad, is that you usually end up overpaying. However, this one trades at 12.8x forward adjusted earnings, which implies growth in the near future, but its growth track record is also pretty good:

Management forecasts between 8% and 15% of organic growth. The exact rates differ by segment but are impressive. The average S&P 500 constituent can only dream of forecasting an 8% growth rate for the next few years out, not too mention a 15% rate.

In addition to the Royce funds owning nearly 10% of the company, another guru, John Rogers' Ariel Investments is its largest backer, owning a 15% stake. It has no debt, has significant cash, is active in a high growth market, forecasts between 8% to 15% CAGR for the next few years and it trades at a forward P/E multiple considerably below that of the market or its industry. Maybe for once, Peter Lynch should be ignored.