Nike (NKE, Financial) investors are well aware of the ambitious $50 billion target that the company has set for itself for the year 2020. At the current level of $30 billion, they need to keep adding an average of $4 billion each year between now and then.

Source: Nike Annual Reports

The question now is: Can it manage to nearly double its current sales in that time? Is that a realistic outlook when you consider the fact that growth typically slows as a company grows bigger? Does the market still hold that much potential for Nike?

Think about this: Nike currently has less than 10% market share in a $190 billion footwear industry – and that 10% is already a hefty 60% of its overall sales.

On the sports apparel front, it's facing stiff competition from Under Armour (UA, Financial), which is quickly closing the gap between first and second place.

But here’s where I think the opportunities lie – China, basketball and women.

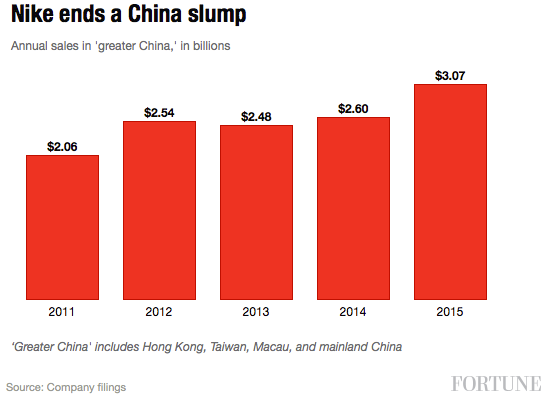

How Nike turned China around

China hasn’t been the best market for Nike over the last few years. Since the 2008 Olympics, its sales have been barely above the $2 billion level. Now, however, things are changing – and here’s why.

The biggest contribution to the China turnaround seems to be the success of the Jordan brand, and Nike is leaving no stone unturned. That’s why it sent Michael Jordan on a goodwill trip to try and fight the copycat manufacturing problems plaguing the nation.

The issue is not necessarily about shoe sales or apparel sales. It’s about the brand. If Nike can protect its brand value in China by highlighting why the public should not be buying counterfeit merchandise, it's made a big win.

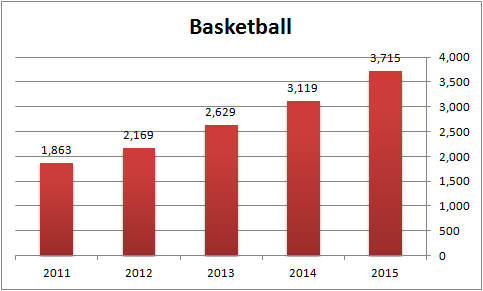

On the product side, however, it’s definitely the basketball segment – and its flagship Jordan brand – that will tear down the sales barriers and get them to that ultimate goal of $50 billion. From the looks of things, it seems that they’ve already begun setting that trend.

Source: Nike Annual Reports

The woman factor

Another reason I think its goal is not too far from being realistic is its women’s segment. Over the last two years it's increased sales by over $1.2 billion.

Source: Nike Annual Reports

As of 2015, Nike raked in $5.7 billion in sales from their women’s line of products. Nike’s target in this segment is to double sales and take it to upwards of $11 billion by 2020.

What are they spending to get them there?

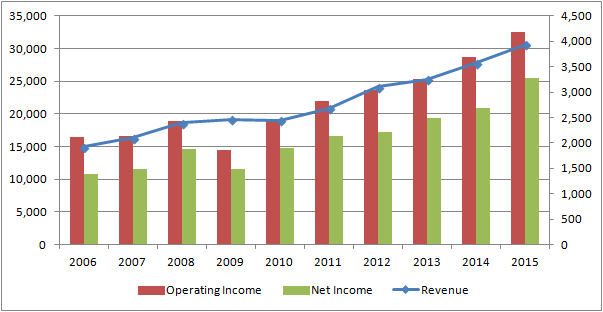

“To bring inspiration and innovation to every athlete in the world” is central to Nike’s branding, and that’s an expensive mission to fund. Let’s take a look at its sales, general and administration cost over a period of time to see how expensive it really is.

There are two parts to Nike’s SG&A – demand creation, and operating expenses. The first is what they pay to their star-studded cast of world-class athletes like Michael Jordan and LeBron James in basketball, Rory McIlroy in golf, Neymar Jr. in soccer and so on. This component also covers their marketing and advertising spend.

Source: Nike Annual Reports

Among their recent “acquisitions” here are Neymar Jr., and they’re also spending more depending on the terms of contract with each sportsperson. If they have a good season, they get paid more, for instance. As you can see from their demand creation spend over the past five years, they’re clearly changing gears in preparation for major gains over the next few years.

Though a lot of investors have been complaining about increasing SG&A, many fail to realize that the bigger increases are coming from OpEx rather than demand creation. Those additional overheads are primarily from getting infrastructure and digital assets into shape.

Nevertheless, their player endorsement costs will be the growth drivers that Nike needs if it wants to get to that $50 billion in the next four years. In fact, it's on track to start spending even more on that front in preparation for that major milestone.

Source: Nike Annual Reports

Source: Nike Annual Reports

As you can from the graph right above this paragraph, the overall spend in SG&A has been a good thing for them. It’s given them a solid growth path and greater profitability, putting them in a much better position than ever to achieve their lofty target.

The investment angle

What investors need to be looking at here is not how much they’re spending but how much more they’re growing as a direct result of those expenses. Nike has always been about branding, awareness and a sense of exclusivity attached to their products, and those are the strengths they’re playing to.

In this revenue growth projection assumed below, I see them hitting that $50 billion with a baseline CAGR of 10.5%. At the lower end, even a 9% growth rate will put them over the $47 billion mark.

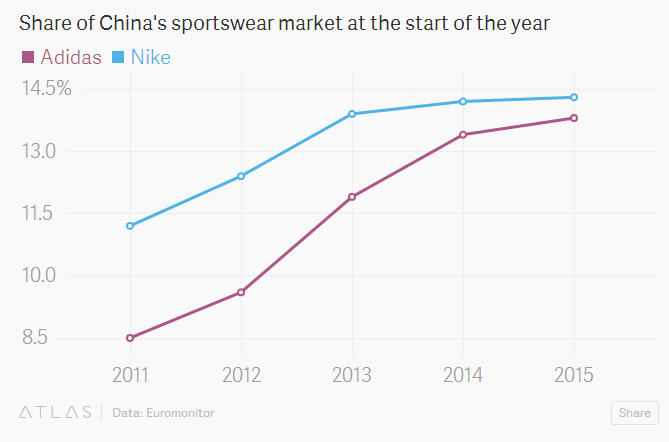

One of the biggest contributors of that solid growth is going to be China, where they’ve made tremendous gains after staying pretty much flat since 2008. Even in the current unstable economy in China – which I think has been exaggerated to a great extent – the sheer number of people being added to the “middle class” segment of the population will help offset any losses.

As for their women’s line, they’re seeing the move to casual wear as a lifestyle shift rather than a fashion or fitness trend. The company is now looking at launching 1,000 stores focused on women in China. Its rival Adidas (ADS, Financial) is already doing this and with a lot of success, too.

Source: QZ

The combination of these factors is what will take Nike over the top. CEO Mark Parker has his finger on the pulse of that great movement, and he’s the one investors should latch on to rather than what the company is actually doing. Great things happen when a great leader is at the front of the action, and that’s what we’re seeing at Nike, now more than ever.

My friendly advice to investors would be to keep adding to their positions whenever there’s a dip in share price. This company will keep growing, and if you want to be a part of that action, you’ll need to move as fast as they are.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.