SiriusXM Holdings Inc. (SIRI, Financial) is on the verge of several new initiatives that promise strong, sustainable growth over the next several years. The satellite radio service provider is making the right moves in many directions, and this is cumulatively going to make it a much more valuable company from an investor’s viewpoint.

Let’s look at just some of SiriusXM’s past and current achievements in the new car segment and chart a growth map on the strength of new opportunities in the used car segment.

Strong subscriber growth and high penetration in new car segment

The first measure of success for any subscription-based service is, naturally, its active user base.

On that front, SIRI is averaging a healthy 7% or more over the past several years. The growth in subscriber base is, for now, driven by the new car conversion rate, which has been holding steady at around 40%. That means 40 out of every 100 new car buyers that had Sirius installed are opting to continue the SiriusXM service at the end of the trial period. The actual uptake in new car line up is actually at around 78% right now; meaning three in four cars roll out of the assembly line with Sirius technology pre-installed.

The reason it won’t go much higher than that is cost. Sirius initially started installing these in high-end automobiles where the additional cost burden would be a relatively small percentage of the overall cost of the car. As they travel down the model line-up for each of the manufacturers they partner with, the return on investment in installations gets tighter, and the uptake rate post the trial period gets lower because a large percentage of buyers of low-priced cars don’t have the kind of disposable income or the inclination to continue to pay for a premium radio service they received as a trial.

The current 78% is very close to that point of resistance, so we can’t expect it to go much higher than that.

On the other hand, the actual value for the company is when these car buyers extend their service beyond the free trial period. At 40%, that’s still a healthy figure, although the service has seen some contraction over the past three years.

During the fourth quarter, Sirius said it expected conversion rates on new cars to hover around the 38-40% level moving forward, and it managed to come in at the lower end of that estimate during the first quarter of 2016.

Being the kind of forward thinking business that Sirius is, however, it isn’t leaving anything to chance. That brings us to the most significant of the many initiatives I spoke about.

Used car installations and subscriber conversions

The logical move after new car installations is used cars, and Sirius is moving in fast on this segment. It already has an uptake of 6 million used car customers for the free trial period as of 2015, approximately 30% of which are expected to convert into paying subscribers.

The used car market is more than two and a half times the size of the new car market and penetration in that segment, according to a Forbes estimate, is much lower than in the latter.

This means a wide-open opportunity for Sirius to penetrate that market. Of course, it may not be able to achieve the 40% conversion level for used cars but, if it even manage to penetrate 20% of the used car market and convert 30% of that into paying customers, that means an additional 8 million paying customers.

I foresee subscription growth rates of over 10% if they manage to penetrate and convert at those levels, and it's getting close to that kind of growth with the last quarter’s figures. Year over year, it's increased overall subscribers from 27.74 million to 30.05 million, a growth of 8.3%. It's not there yet, but a couple of more quarters should give it more traction in this relatively new segment.

With 6 million installations creating nearly 2 million new customers, the growth for this segment is promising. Assuming that the projections are accurate, if Sirius can double the uptake to 12 million over the next two years and triple it in the next decade, it's looking at 35 million 50 million subscribers from the new and used car market combined.

That’s great news from any perspective, especially that of an investor.

That’s why Sirius is aggressively networking with used car dealerships across America to the tune of 19,000 or more. Naturally, that figure will also top out after a point, but they’re still only at the 50% mark on that front.

To be sure, Sirius is leaving no stone unturned when it comes to studying the potential of this market and grabbing every opportunity that comes its way. They’ve already signed up with about 80 Jiffy Lubes to get data on radio installations and active status; they are in talks with auto loan companies; they’re even approaching companies that have websites or mobile apps related to the used car market to make sure every angle is covered.

This kind of drive will easily help them double their used car installations as early as 2018, in my opinion. Seen in combination with a 30% conversion rate, that’s a solid growth curve over the next few years.

The problem with pricing

The only area where I see a problem is pricing. Sirius has been increasing its package pricing on a near-regular basis, and the company doesn’t seem to be worried about the churn rate going up. Some argue that the churn rate numbers are being “controlled” by the addition of discount-based customer win-backs, and I would agree with the gist of what they’re saying.

Price increases are never an easy thing to manage because after a point it precludes them from offering more economical packages to attract new subscribers.

For example, if they started offering a limited period new user discount on any one of their packages below, what’s the guarantee that a significant percentage of their subscribers won’t cancel their existing package and register as new users? It won’t show up in churn rates, but it will artificially boost conversion rates.

From a business perspective, the pricing they have right now is good enough. I don’t think they need to upset the apple cart just to put new wheels on it. Their focus needs to be on two things as far as subscribers are concerned:

Increasing the conversion rate for used car free trial installations

Adding more people to the top of the funnel for the free trial for used cars

As we’ve seen, those alone will take them to the next level of 35+ million paying customers.

The investment angle: what metrics to follow

Instead of losing focus by looking at the many things they’re doing, investors are better advised to keep their eyes on one area in depth so they know what’s really going on with the company.

With respect to new market segments within the United States, the key metrics to watch over the next few quarters are these:

Penetration in the used car market

Total installations in new and used car segments

Conversion rates in the used car market

Churn rate increases based on price increases

Spiking conversion rates post price increases

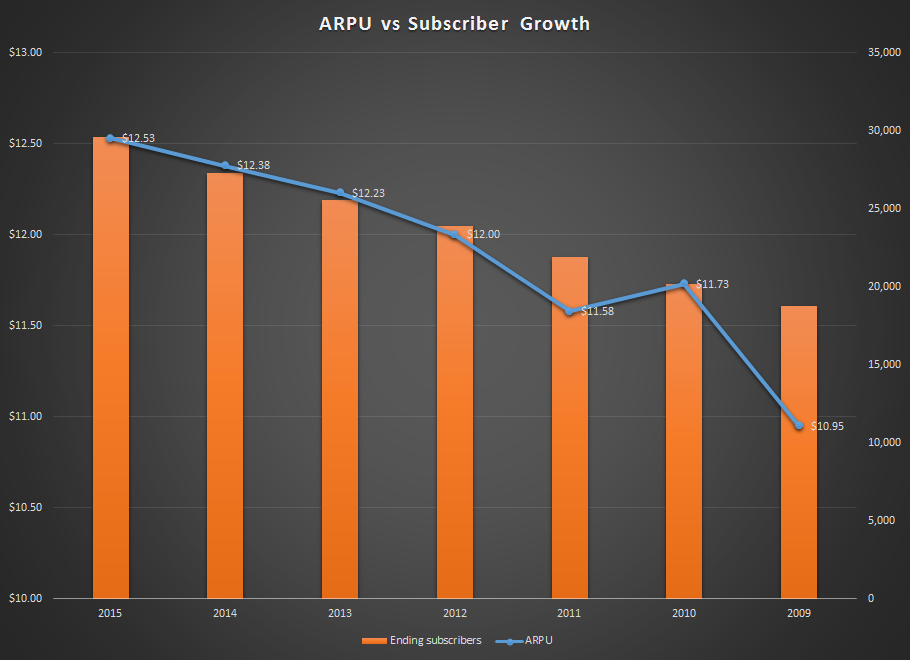

ARPU - average revenue per user

These six numbers are excellent indicators of the company’s performance.

I have no doubt that they’re pushing as hard as they can on used car installations, but we need to watch the new car installations to see where that resistance level is for that segment. From that perspective, a low penetration growth signals a mature market that can be sustained indefinitely at that level.

As for churn rates and spikes in new subscribers, that will be an indication that their pricing strategy is starting to show holes.

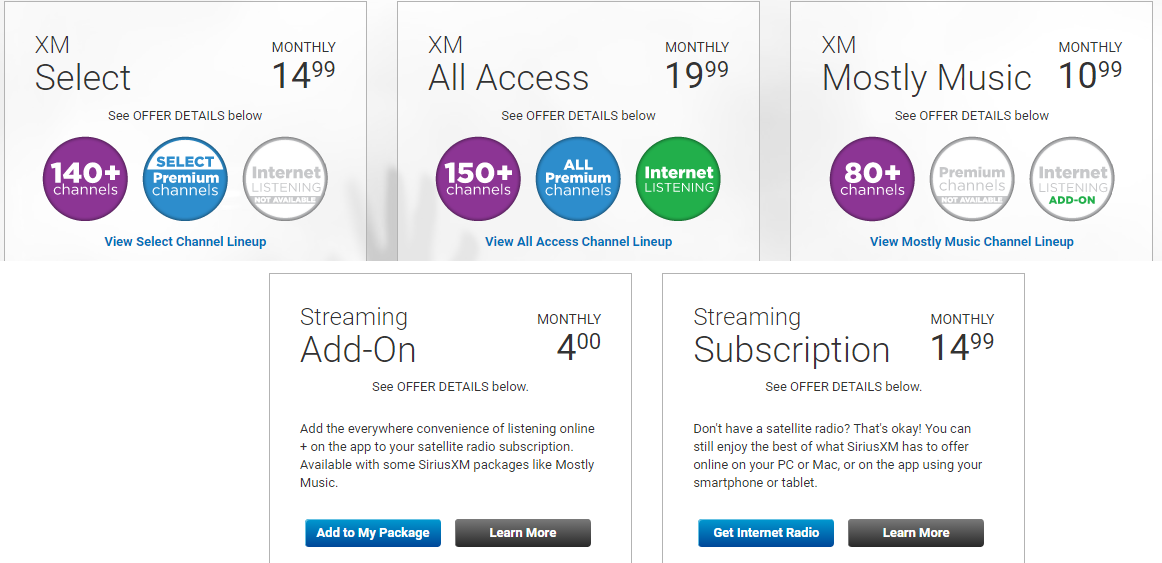

Average revenue per user is a good indicator of whether the customer base is moving towards high-end packages or making do with Select or Mostly Music as a preferred choice over All Access - and whether the add-on packages are making their way to the top line.

At this point, it must be said that regular price increases can mask a lot of the trends underlying consumer decisions; as such, it is not the best indicator of spending behavior.

On the bright side, the company’s margins will allow it to quickly drop pricing and maintain subscription levels if it sees any sort of anomaly in average spend, as long as they have a finger on the right pulse point.

Disclosure:I have no position in any of the stocks mentioned, and no intention to initiate any position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.