2016 has been really kind to Advanced Micro Devices (AMD, Financial). The stock is up 89.9% since the start of the year and is trading at more than twice the price range it was at around this time last year. But does that mean AMD’s business fortunes have brightened? Considering the intense competitive pressure from the star of the industry, Nvidia (NVDA, Financial), that might not be the case.

The Polaris ddvantage

AMD announced the launch of its first Polaris graphics card, the next generation Zen-based processor, in June, pricing it at $200. The product opened with some good reviews and, at that price point, AMD’s product certainly has an edge with which to capture some market share.

“The GTX 1060’s first problem is its cost. The GPU debuting today is the Founder’s Edition, priced at $299. Partner cards starting at $250 are already on the way, but the $300 version of the GPU is 25.5% more expensive than the RX 480 while offering 7 – 13.5% better performance. That gives the 8GB edition of the RX 480 a clear value advantage. The $250 version of the GTX 1060 will be far more competitive, but AMD has the 4GB RX 480 sitting at the $200 price point. Given that the performance difference between the 4GB and 8GB cards is minimal, a $200 4GB RX 480’s performance-per-dollar will compare extremely well against the GTX 1060.”

If you look a bit closely at AMD’s stock price run up, you will notice that investor enthusiasm was given a boost right after AMD’s announcement early this year that Polaris graphics cards are expected to hit the market sometime in the middle of 2016, a commitment that the company has kept. It is now evident that positive reviews around that — as well as the pricing — have indeed helped lift investor sentiment.

Is AMD in the clear?

But what does that mean for the company’s future? By no means is the new product line going to get them out of the woods. The company has been losing money for the last four years and revenue has been stagnant for the last 10 years. But the company says that it expects to see revenues grow in 2016, with the second half of the year showing stronger numbers than the first.

But it will be a tough job to get back to profitability unless Polaris sees some real success in the market.

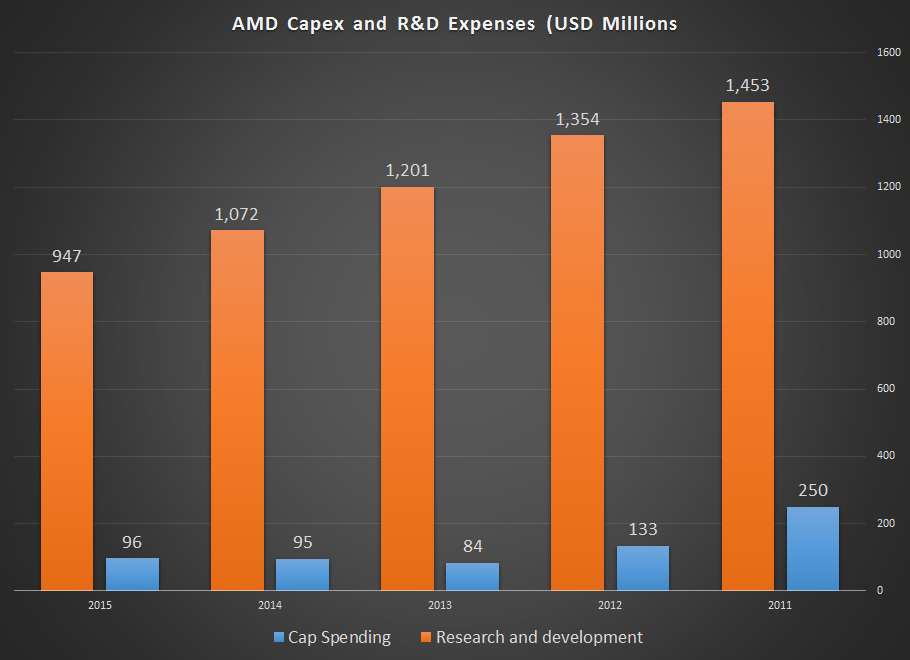

The good news is that AMD has low debt, which will give it a little wiggle room to get out of the hole it's in. High debt would have made the situation much worse because it may have curtailed the ability to pump more money into R&D, which any company in this segment needs to do on an ongoing basis. It's already had to cut R&D spending as well as capex on the back of declining revenues, as you can see from the graph above.

With Nvidia spending in the $1.3 billion range for research and development for the last three years, AMD will want to get back to those levels soon. As long as it is in the red, however, that’s not going to happen, and the competition is going to keep running away with more market share.

Disclosure: I have no position in any of the stocks mentioned, and no intention to initiate any position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.