A lot of analysts are saying that iPhone sales have peaked, and the only way for Apple (AAPL, Financial) is down. It's not too hard to see their case.

The number of people around the world who can use a smartphone is a finite number. Though there are pockets in the world where smartphones have yet to penetrate, there isn’t much left to cover. iPhones clearly fall in the luxury segment so once you factor in the cost of the average iPhone the potential market for iPhones is a subset of the potential smartphone market, and growth cannot happen forever.

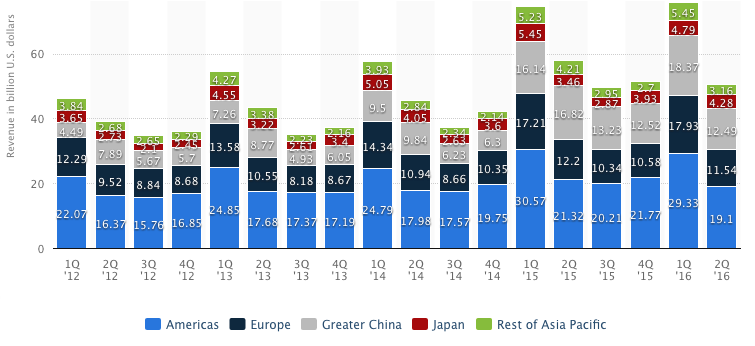

Apple knows this, and with major parts of developed markets already covered, it knows that there is volume in emerging markets. That's something I covered in my recent article on Apple's earnings for the third quarter. It also knows that its current price point will be a huge barrier in such markets simply because of economic disparity. As you can see from Apple’s revenue history, Greater China is the only emerging market that makes a significant contribution to the company’s top line.

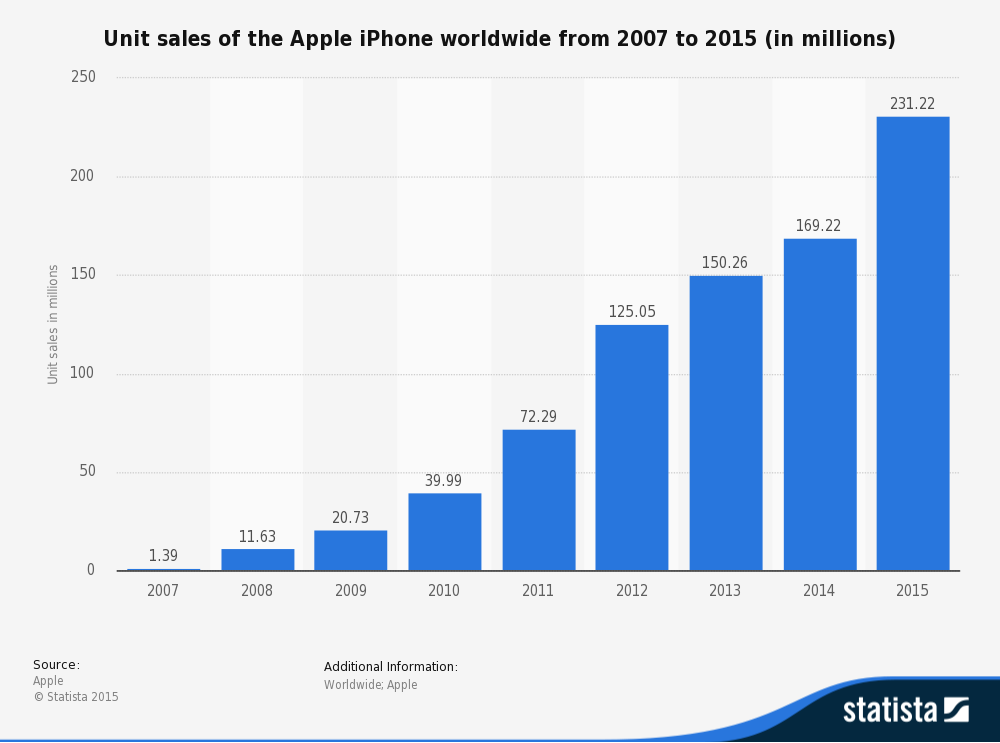

Source: Statista

So now Apple has a challenge as well as an opportunity. Large populations across the world sit outside their spheres of influence because of the high cost of iPhones, iPads, Mac PCs and other iOS devices.

Enter iPhone SE

The cheapest iPhone yet, the iPhone SE is a product that can help expand Apple’s reach in highly populous emerging countries. But even with this newfound market strategy to target the mass smartphone market instead of its bread-and-butter luxury smartphone market, Apple’s iPhone sales cannot grow forever.

The company will reach a point, sooner or later, where the sales of iPhones around the world stabilize. When that happens, unit sales growth and revenue will directly depend on new product launches and the frequency with which iPhone users upgrade their devices.

There is huge speculation in the market that the day has already arrived, but I respectfully disagree with that assertion. It will happen someday for sure but not while Apple still holds the premium market.

Let’s use the automobile industry as a loose analogy. Carmakers like Mercedes and BMW (XSWX:BMW, Financial) are primarily in the large luxury segment, but they do have cheaper models in the entry-level luxury segment as well with models like the C Class, 2 and 3 series. Naturally, margins are lower in this second segment, but sales volumes are much higher. Opening up to these non-premium markets allows Mercedes and BMW to expand their markets while holding on to the premium segment.

As you can see, volumes are much higher in the subpremium segment for all these companies.

Similarly, the iPhone SE represents that same subpremium market for Apple. It’s not going to take away from high-end iPhone sales; rather, it will bolster Apple’s top line until and beyond the point where premium iPhone sales will start to plateau – something that is inevitable once penetration reaches a certain level.

Why user ecosystems are so critical

Apple recognizes the problems of high penetration, but it also recognizes the problem of subpremium devices on the market. The iPhone SE is as low as Apple is willing to go, and once this market, too, achieves high penetration, what other options does it have to keep growing its top line?

That brings us to Apple Services, a reporting segment that is already showing signs of healthy growth.

Apple’s services portfolio or the “Apple ecosystem,” as I like to refer to it, has many products and services such as Apps, Apple Pay, Apple Music, iTunes, Maps and many more to come.

All these are components of an ecosystem that tech companies today are forced to build around their core products or services. In Apple’s case, these components are monetized – it makes money from each of these, with the possible exception of Apple Maps.

But take Google, for example. Apart from its share of app revenues, Android doesn’t really make that much money for Google. And what about Google Maps, Google Search, Gmail, Drive and all the other free services? None of those are direct revenue earners, but they are important conduits to bring traffic to Google Sites and search pages, where the real money is made on its ad networks.

The entire purpose of the ecosystem is to keep the users within that ecosystem so they can ultimately be guided to that monetized part of the system. That’s the reason Facebook (FB, Financial) spent billions on acquisitions and video initiatives; that’s the reason Microsoft (MSFT, Financial) is building its own ecosystem with Windows 10, the Universal Windows Platform and the new push into mobile with Xamarin.

All of these companies have recognized that user growth and user engagement are key to their financial success.

A word to investors

And that’s something Apple has realized as well. With the gamut of services it offers, it's created an ecosystem where users will ultimately be guided toward the revenue-generating parts of that system.

The more Apple is able to engage users through its services, the tighter these users are integrated into the ecosystem and the greater the likelihood that they will start using paid services that ultimately make up Apple’s top line.

Devices aren’t enough anymore, and Apple knows this. This is what analysts have identified, but they are missing the dynamics behind Apple building that ecosystem. Apple’s service segment is part of that ecosystem as much as its devices are.

I’m strongly against the doomsday scenario that a lot of analysts have painted for Apple’s future. The company still has tremendous upside, and services form a major part of that upside. As the company keeps expanding services like Apple Pay and keeps investing in companies like Didi Chuxing, market leaders that can benefit immensely from products like Apple Maps, the company will keep growing.

It’s time for the second phase of Apple Inc., and that phase is heavily reliant on the ecosystem it is building. The iPhone SE and Apple Watch may help stem revenue bleed in the short term, but I see services as the core revenue conduits – if not growth engines – of Apple’s future.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.