Verizon (VZ, Financial), the No. 1 wireless carrier in the U.S., finished the first quarter with 146.013 million subscribers, nearly 12 million more than second-place AT&T (T, Financial) and more than twice that of third-place T-Mobile (TMUS, Financial). But the problem for wireless carriers is the state of the market.

The top five players of the market had 416 million subscriptions in the U.S., a country with a population of around 325 million and smartphone penetration of 80%. The subscription count is higher than the overall population because there are a lot of consumers using multiple subscriptions. The penetration level is already way too high, and the market is already in a state of retention rather than growth.

With a bulk of its revenue coming from wireless operations, Verizon’s ability to grow its revenue is under a huge threat, and growth itself has been coming down over the past several quarters. Both AT&T and Verizon, the top two carriers in the U.S., are aggressively diversifying into other areas so they can get their revenue growth back on track, and this is one of the main reasons why both stocks are trading with yields higher than 5%.

Consulting firm Strategy Analytics predicts that 100 million wireless connections will be added between 2015 and 2020 but only foresees a 0.2% increase in wireless service revenues. The reason for such a dour forecast can easily be divined: There are five strong players in the market who need to share between themselves any additional connections that come their way. The fierce fight for the additional customer – and not to forget the work needed to retain customers – will force companies to outplay each other, doling out promotions and discounts while increasing the product’s value at the same time, all the while driving down margins and profits in the process.

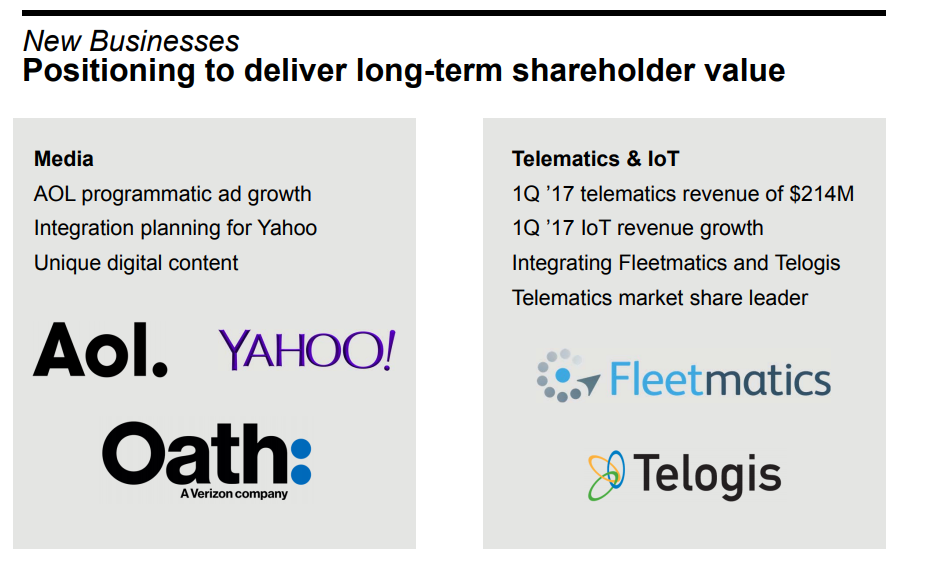

Verizon has embarked on an ambitious content strategy, buying several media properties such as AOL and Yahoo (YHOO, Financial). But the results are yet to start showing up on the bottom line. With no clear path to return to steady revenue growth, the market has remained indifferent to Verizon, and the stock has been moving sideways in a tight trading range of $45 to $55 since 2013.

At the end of the first quarter Verizon had long-term debt of $112.83 billion, paid $1.13 billion as interest expense during the quarter and spent another $2.354 billion as dividends while capital expenditures were $3.067 billion. Verizon had an operating income of $7.181 billion for the quarter and, one can clearly see, there isn’t much room for Verizon to play around with its cash flows. Its best bet is obviously to get the revenues back on track.

It's not really a surprise that the dividend yield has shot above 5% because there are significant risks the investor needs to take with Verizon. Though the size, scale and the No. 1 position in the U.S. wireless market – not to mention the high capex nature of the industry – will allow Verizon to hold on to its market leadership position. In the current state, though, it is  difficult to recommend Verizon as a solid dividend play.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.