David Einhorn (Trades, Portfolio)’s second-quarter 2017 letter is out. In it, he comments on both his long General Motors Co. (GM, Financial) position and his short Tesla Inc. (TSLA, Financial) position. The full letter is embedded below. He broke up the commentary on purpose as it is not intended to be a pair trade, although it could be one. Quoted from the letter, emphasis mine:

"General Motors (NYSE: GM) fell 1% to $34.93 after announcing a strong first quarter, with earnings 15% above consensus estimates. Still, auto sentiment remains poor, and the company continues to trade with the lowest multiple in the S&P 500. We continue to believe that the market is overestimating GM’s vulnerability to the next down-cycle and is underestimating its longer-term competitive position, the impact of share repurchases and its current earnings power."

Not two days ago, I commented oh how General Motors trades at three times operating cash flow, how it will have generated operating cash flow equal to its current market cap in a couple of years and that it trades at 5.6 times earnings and 5.3 times EV/EBITDA.Â

If you buy into the idea General Motors is undervalued, it is clear this kind of operating cash flow (partially) directed toward share buybacks will yield favorable results for a shareholder. The massive cash flow takes out more than it is worth in equity, which results in ever greater future cash flows. Once these get rerated, a shareholder is looking at a double whammy.

"GM is capitalized to survive any foreseeable downturn. It has $20 billion of cash and a$14.5 billion undrawn revolver. Meanwhile, it is currently generating billions of dollars in free cash flow. TSLA is capitalized to survive only the next three quarters. While its cars do not burn gasoline, the company burns more than enoughcash to compensate, and behaves as if it will have access to nearly free capital for theforeseeable future."

Below you will find a comprehensive number of statistics to compare the two companies from the GuruFocus analysis page.

| Company |  | Revenue (Mil) | Market Cap ($Mil) | P/E Ratio without NRI | P/S Ratio | P/B Ratio | Operating Margin | Net Margin | ROA | ROE | EV/EBIT | EV/Revenue | Dividend Yield | Dividend Payout Ratio | Debt-to-Equity |

| General Motors Co | Â | $170,315 | $54,901 | 5.64 | 0.33 | 1.18 | 6.06% | 5.92% | 4.65% | 23.01% | 9.4 | 0.72 | 4.16% | 0.24 | 1.98 |

| Tesla Inc | Â | $8,549 | $52,492 | 0 | 5.79 | 10.46 | -7.91% | -8.46% | -4.44% | -22.72% | -98.65 | 6.72 | 0% | 0 | 1.63 |

The EV/Revenue metric and the price-book (P/B) ratio are especially interesting metrics to compare the companies on. Other valuation metrics do not work as well since Tesla continues to lose money.

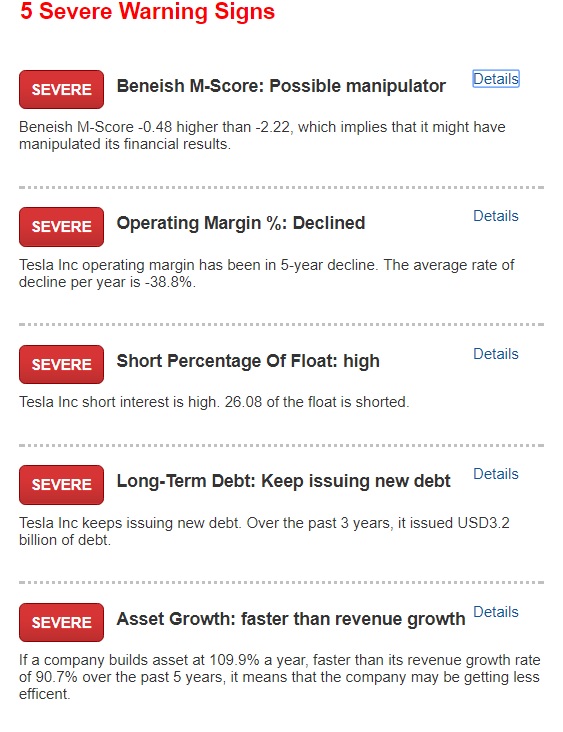

It would suprise me if Tesla CEO Elon Musk is not able to raise more money from investors who support an electric future, but GuruFocus does identify no less than five severe warning signs:

Einhorn comments on availability:

"GM bears are focused on the overhang from leased vehicles returning to the market, making the case that excess vehicles are forcing down used car pricing, which will inturn pressure new car sales and margins. This may be true, but we believe TSLA faces the same risk and then some. 2014 was the first year of TSLA’s three-year leasing program. Already, many of those cars are hitting the resale market at surprisingly low prices. It is a real risk for TSLA that customers may prefer a three-year-old Model S available right now to a Model 3 available in a year or two at roughly the same price point. TSLA’s balance sheet reveals that deposits have been returned to many prospective Model 3 customers."

Checking into Einhorn's comments on the availability of the 2013 Model S, there is one available on eBay (EBAY, Financial) for just $36 thousand with around 80 thousand miles on it, which is a price level comparable to the new Bolt or model 3:

Source: eBay

There is even one for $36 thousand with only 25 thousand miles on it:

Source: eBay

Einhorn is a guru I try to follow closely as his portfolio tends to sport many great investment ideas. Both of these positions are no exception. Like a true value investor, Einhorn shorts the no cash flow and pie-in-the-sky company and is long a company that is throwing off cash with a balance sheet that can be optimized further.

Greenlight Q2 17 by marketfolly.com on Scribd.

Disclosure: No positions.