(Published by Bob Ciura on July 28)

There are hundreds upon hundreds of dividend stocks to choose from. But for investors interested in only the highest-quality dividend stocks, the Dividend Aristocrats are the “cream of the crop”.

The Dividend Aristocrats are stocks in the S&P 500 Index with at least 25 years of consecutive dividend increases.

Consolidated Edison Inc. (ED, Financial) is a standout among the Dividend Aristocrats.

The company’s dividend history is highly impressive. It has increased its dividend for 43 years in a row. It is the only utility stock on the list of Dividend Aristocrats.

Right now, it has a 3.4% dividend yield. With more than 100 years of dividends and at least a 3% dividend yield, ConEd meets our definition of a "blue-chip" stock.

We will discuss why ConEd should be at the top of the list for investors interested in blue-chip utility stocks.

Business overview

ConEd is a regulated gas and electric utility. It provides service to more than three million electricity and one million gas customers in New York.

ConEd has four operating segments:

- Electric (71% of revenue)

- Gas (14% of revenue)

- Steam (5% of revenue)

- Non-Utility (10% of revenue)

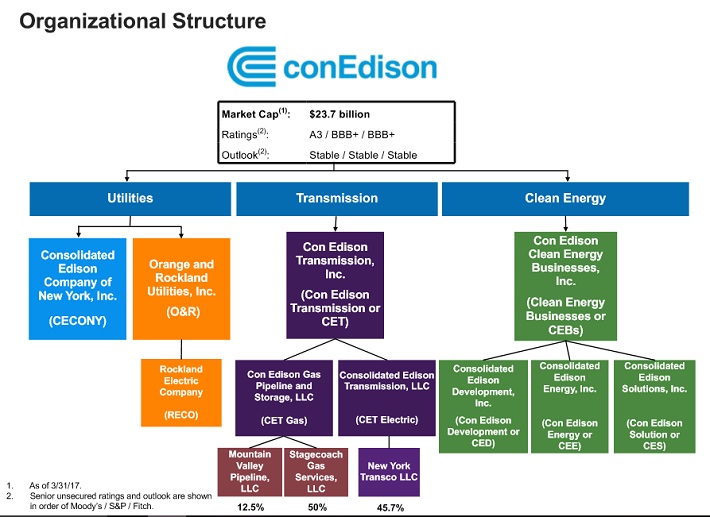

It has a variety of subsidiaries in the electric, transmission and green energy businesses.

Source: First-Quarter 2017 Presentation, page 4

2016 was another year of steady growth for ConEd. For the year, earnings per share increased 2% to $4.15.

The fourth quarter was especially strong. Earnings per share, as adjusted for non-recurring factors, increased 13% due to favorable weather.

Earnings were boosted by the core electric utility business. ConEd enjoyed higher gas net base revenue, higher electric net base revenue and an increase in total gas customers.

ConEd also benefited from lower pension expenses last quarter. The company has seen operating expenses increase in recent years as it invests additional resources to modernize its assets.

ConEd’s growth this year and beyond will be from rate increases and new customer additions.

Growth prospects

The best aspect of buying utilities is their high degree of earnings predictability. Thanks to regulatory approvals and population growth, ConEd is almost certain to grow earnings each year.

In early 2017, ConEd received approval for rate base plans over the next three years in both the electric and gas delivery segments.

From 2017 to 2019, the company expects to grow its average annual rate base by 5% to 6% per year. This will be a significant boost to revenue growth over that period.

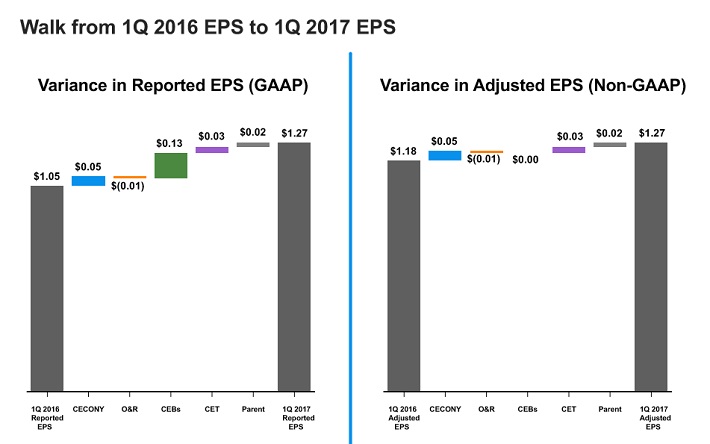

Rate increases are the main driver of ConEd’s growth. This was on full display in the first quarter of 2017. Higher rates at the core CECONY segment fueled last quarter’s growth.

Source: First-Quarter 2017 Presentation, page 8

Electric and gas rate changes contributed 20 cents per share of earnings growth last quarter.

Overall, ConEd’s adjusted EPS increased nine cents year over year to $1.27. Earnings grew 8% year over year, which is a very strong earnings growth rate for a utility.

Customer additions are an additional catalyst, accounting for a two-cent boost to EPS in the first quarter.

ConEd also realized a four-cent benefit to EPS last quarter due to lower pension expenses. The company has deployed a cost-cutting program over the last several years to help offset the investment costs of modernizing its generation assets.

The benefits of higher rates, new customer accounts and lower operating expenses more than outweighed higher depreciation and tax expenses last quarter.

2017 is likely to be another year of modest growth for ConEd. Management forecasts adjusted EPS in a range of $3.95 to $4.15. The company expects 1% to 2% earnings growth this year.

Competitive advantages and recession performance

ConEd’s biggest competitive advantage is its industry. As a utility, the company delivers a service that is imperative to society. Electricity and gas are essentially a matter of national security.

This puts a very powerful floor underneath ConEd’s profit generation. Investors can buy high-quality utility stocks like ConEd and sleep well at night because they do not have to worry that profitability will one day disappear.

Another competitive advantage of the utility business is it has a very wide moat. ConEd has nearly $50 billion in assets. It would be nearly impossible for a new competitor to enter the industry and attempt to take market share.

The regulatory and operational costs associated with trying to compete at ConEd’s scale are extremely prohibitive.

As a result, ConEd maintains profitability every year, regardless of the economic climate. Its financial performance during the Great Recession is as follows:

- 2007 EPS of $3.48.

- 2008 EPS of $3.36.

- 2009 EPS of $3.14.

- 2010 EPS of $3.47.

EPS declined in 2008 and 2009, but the company remained highly profitable. In addition, EPS quickly recovered in 2010.

Valuation and expected total returns

ConEd has seen its valuation expand over the past several years. The stock has outperformed the S&P 500 Index in the past decade by more than 20 percentage points, including dividends.

Today, shares trade at a price-earnings (P/E) ratio of 19.8 based on 2016 EPS. This is a discount to the S&P 500 Index, which has an average P/EÂ ratio of 24.7 currently.

Utility stocks, however, typically trade at a discount to the market average since they tend to exhibit below-average earnings growth. Therefore, ConEd seems fairly valued at the moment.

Going forward, investor returns will be generated by earnings growth and dividends. A potential breakdown of future returns is as follows:

- 4% to 6% earnings growth.

- 3.4% dividend yield.

In this scenario, ConEd stock would return approximately 8% to 10% per year.

Not surprisingly, the dividend will play a major role in shareholder returns moving forward. High dividend yields are a big reason why investors buy utility stocks.

Importantly, the dividend is secure. ConEd aims for a target dividend payout ratio of 60% to 70% of annual adjusted EPS.

Its current dividend of $2.76 per share represents 67% to 70% of projected 2017 adjusted EPS, which means the company is right on target.

Final thoughts

Utility stocks may not be the most exciting to buy, but they serve a very valuable purpose. High-quality utilities like ConEd provide high dividend yields, with the added security the dividend payouts are highly sustainable.

ConEd has increased its dividend each year for more than 40 years.

The stock does not appear to be significantly undervalued at the present time. But it offers high single-digit to low double-digit total return potential and a rock-solid dividend.

Disclosure: I am not long any of the stocks mentioned in this article.