Alphabet’s (GOOG, Financial)(GOOGL, Financial) revenue is completely dependent on Google’s performance on the advertising front. Although there were several moving parts in Google’s revenue stream such as Google Cloud and Google Other Bets such as Google Fiber during the second quarter, Google’s advertising revenue was $22.672 billion, accounting for 87.16% of its overall revenue during the quarter.

At that level, both top-line and bottom-line performance are tied to the performance on the advertising front. After the second-quarter results were announced, Alphabet’s stock price declined despite reporting 21% revenue growth for the quarter, and the reason for worry was none other than Google’s rising Traffic Acquisition Cost, or TAC.

Alphabet shares fell after second-quarter results resurfaced a worrying trend: The company’s costs are rising as it spends more to expand Google’s newer, fastest-growing advertising businesses. “Growth in TAC accelerated for the third straight quarter, suggesting rising costs of future ad dollars,” said James Cakmak, an analyst at Monness Crespi Hardt & Co. –Bloomberg

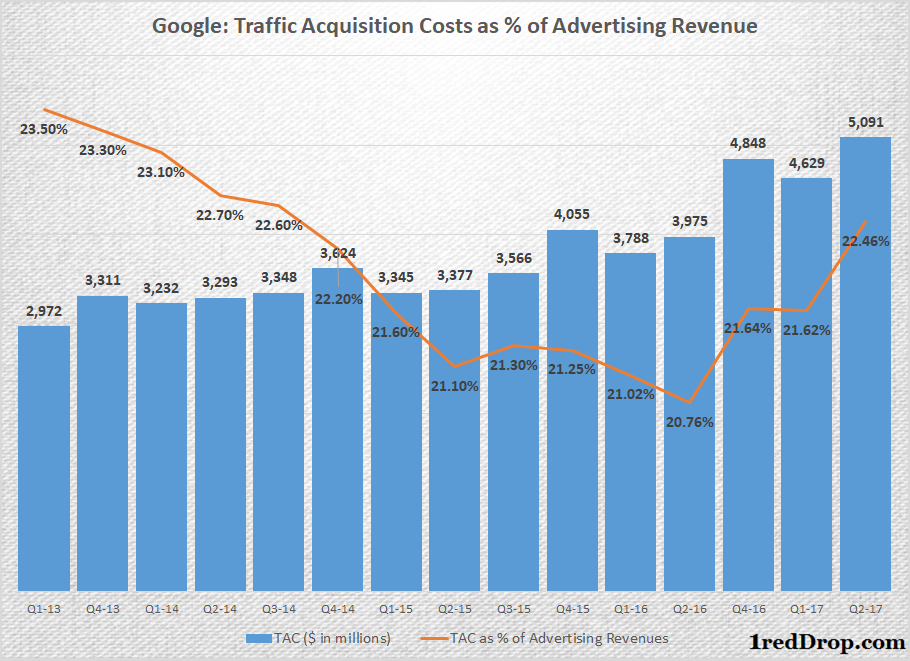

This was cause for concern because Traffic Acquisition Costs have increased from $2.97 billion in the first quarter of 2013 to $5.091 billion during the second quarter of 2017. TAC is the amount of money Google pays to its partners for sending traffic to Google properties, which traffic is then monetized.

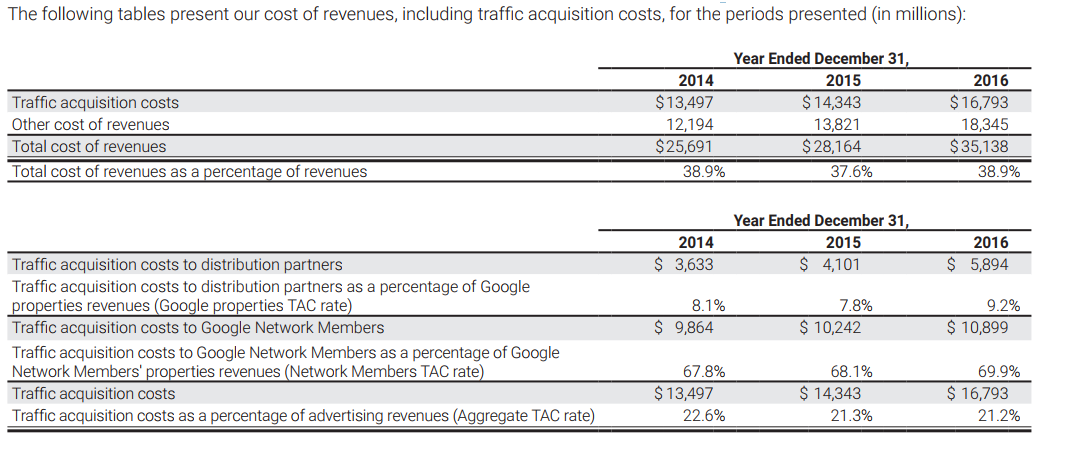

In Alphabet’s own words, from its 2016 Annual Report:

“Cost of revenues consists of traffic acquisition costs (TAC) which are paid to Google Network Members primarily for ads displayed on their properties and amounts paid to our distribution partners who make available our search access points and services. Our distribution partners include browser providers, mobile carriers, original equipment manufacturers and software developers.”

TAC as a percentage of advertising revenue declined in the 2013-2015 period before it started rising sharply in the last four quarters, increasing from 20.76% of advertising revenue to 22.46%. Since TAC accounts for the bulk of the cost, any increase will directly impact operating margin levels, which was the primary reason for the market’s reaction.

Source: Google 2016 Annual Report

During the second-quarter earnings call Ruth Porat, Alphabet chief financial officer, said

"Total traffic acquisition costs were $5.1 billion, or 22% of total advertising revenues, and up 28% year over year.

"The increase in both sites' TAC as a percentage of sites revenues, as well as network TAC as a percentage of network revenues, continues to reflect the fact that our strongest growth areas, namely mobile search and programmatic, carry higher TAC.”

The shift to mobile is an ongoing but irreversible phenomenon – irreversible because desktop shipments have been on a steady decline for the last five years and continued their decline this year as well. According to Gartner, PC sales declined 4.3% during the second quarter. We still don't know where the bottom is for the PC market, and even if it gets there sooner rather than later, we are never going to see it climb back up again to its pre-2012 levels. Smartphones and smart home devices have clearly eliminated the need for PCs, and mobile traffic is only going to increase at the cost of desktop traffic in the future.

As the shift to mobile continues, Google will have to keep paying partners like Apple to send traffic. Though Android continues to hold a major portion of the mobile OS market, Apple users – sitting in the premium position – are extremely important for Google. The higher the number of Apple users, the higher Google’s payments will get.

As Ruth Porat said, TAC is higher for mobile, and we expect higher traffic from mobile users over the next several years. The margins are going to shrink because of this, but as mobile traffic keeps increasing against declining desktop traffic, margins will shrink first and then stabilize. They cannot keep shrinking forever.

If the stock drops due to TAC increase in the next quarter, which I expect it will, investors should keep buying because the margin pressure will be a short- to medium-term one rather than a long-term one.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.