Procter & Gamble, the 180-year-old consumer goods company, has been a darling to dividend investors. There aren’t many companies in the world that can boast of 61 years of dividend increases. But lack of innovation, competition and its own size has made life extremely difficult for PG, as it struggles to get its sales moving despite its restructuring efforts.

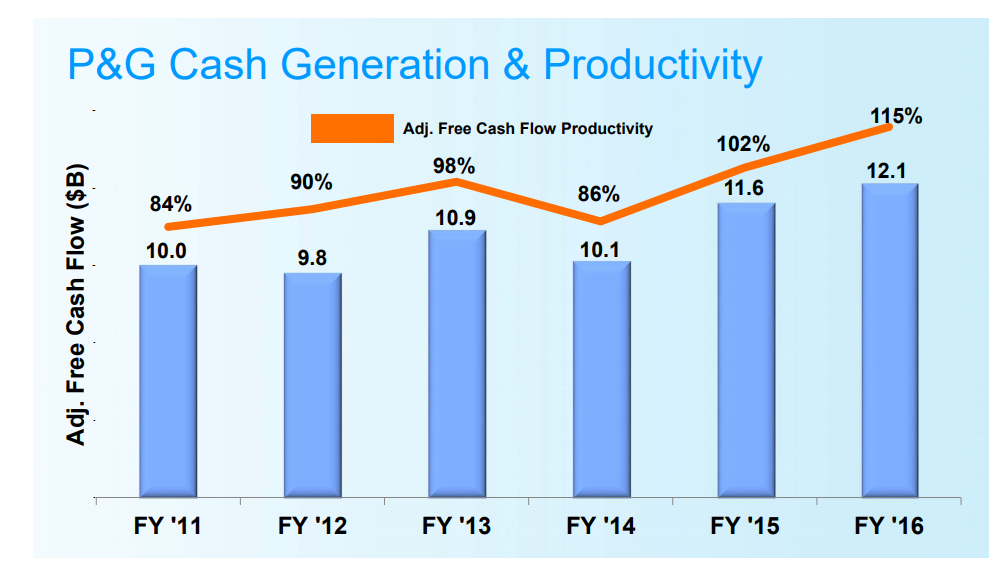

PG had several positives in 2017. Operating margin had increased from 15.6% in 2015 to 21.45% in 2017; adjusted free cash flow increased by $2.1 billion in the last five years; and PG has moved from running 170 brands to now nurturing 65 brands. It was natural to expect the company to keep the best products that can further its future growth. But despite the lean portfolio of products - which has proved to be higher margin products, as we clearly saw in the way operating margins improved in the last three years - sales growth remains a bit on the lower side, making one wonder about the long-term implications.

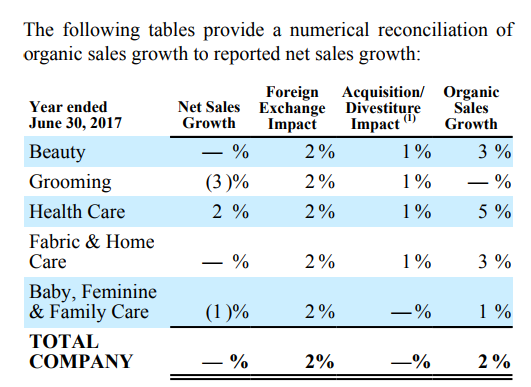

During the recently concluded fourth quarter, organic sales increased by 2% year-over-year, thanks to Beauty and Fabric & Home Care growing by 3% each and Health Care growing by 5%. Grooming showed flat growth, and Baby, Feminine and Family Care reported 1% organic sales growth.

PG Annual Report 2017

Net sales growth was flat during Fiscal 2017 thanks to a stronger dollar, which had a 2% negative impact on their growth numbers. But the real problem PG is facing is that it has sold off more than half of the brands it had during its restructuring process - a process that cannot keep going on forever. If the brands they selected can only post flat sales growth to 2% growth - without and with forex impact - the growth trajectory over the next ten years is going to be up and down at best.

PG is already walking a tightrope when it comes to dividends, and if sales growth keeps eluding the company, things will only get more difficult over the next five years. During 2017, PG paid $7.236 billion in dividends, which is nearly 52% of its operating income. PG spends. Operating margin numbers improved due to the restructuring process; and, since that process is nearly over, further increases will be hard to come by. That means that any dividend increase from here on out will keep increasing their payout ratio.

By the end of 2017, PG had $15.137 billion in cash and marketable securities against long term debt of $18.038 billion. The balance sheet position does offer some breathing space for PG, and will give it some time to get its sales back on track. But until revenue starts growing in a meaningful way, PG’s dividends will remain under pressure. Wait for PG to show steady revenue growth before investing, because the long-term risks outweigh the current 3% dividend yield.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.