Starbucks (SBUX, Financial), the global premium coffee house chain, continued its sideways journey, reporting weak same store sales as traffic in U.S. stores kept slowing down. The stock has been stuck between $55 and $65 since the start of the year, and fourth quarter earnings did nothing to improve market sentiment towards the company.

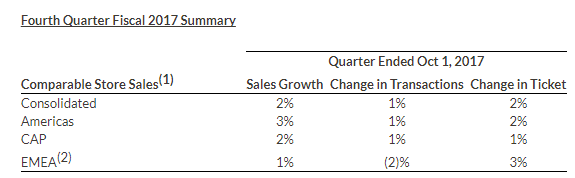

Starbucks reported adjusted earnings per share of 55 cents - in line with market expectations - but revenue came in at $5.7 billion, below the expected 5.8 billion. The worst news was that comparable store sales were down to 2% during the quarter as transactions during the quarter grew by just one percent.

Comparable store sales in the U.S. were 3%, lower than the 3.4% the market was expecting. The Americas segment is the largest market for Starbucks, accounting for nearly 70% of the company’s revenue. For fiscal 2017, Starbucks reported 3% comparable store sales growth, and all of that growth was due to Starbucks increasing prices by 4% as transactions remained flat.

The price increase, coupled with the opening of 2,254 stores, is what helped Starbucks post 5% revenue growth during the year. Starbucks certainly has a huge runway in terms of store openings globally, targeting 37,000 stores by 2021. It’s a long way to go from the 27,339 stores the company had at the end of fourth quarter of 2017, and the company still needs to hit 2,500 net openings annually to achieve that target by the end of fiscal 2021.

The company revised its long-term earnings per share growth downward, and now expects annual EPS growth of 12% instead of the previously expected 15% to 20%.

China remains at the core of Starbucks’ growth plan. The company opened 550 stores during Fiscal 2017, taking the total number of stores in the country to 3,000 stores across 135 cities. Starbucks has also ramped up its investments in technology to increase its sales, and some of those efforts have started to pay off.

During the fourth quarter earnings call CEO Kevin Johnson said:

“In fiscal 2017, Starbucks Rewards membership in the U.S. rose 11% year-over-year. Per member spend increased 8% in Q4 alone. The cumulative effect is that today 36% of tender comes from Starbucks Rewards. The vast majority, via our mobile app.”

The company is also planning to roll out its “Mobile Order and Pay” capabilities to all of its customers soon, instead of keeping it exclusive to Starbucks Rewards members. But it still remains to be seen if these digital initiatives will be able to get more customers through the door for Starbucks in the U.S.

Though new store openings will certainly keep Starbucks’ revenue growth numbers ticking, the stock price will remain under pressure as long as comparable store sales remains weak in the home market.

The company has a lot of short-term headaches to address, but still remains one of the best long-term investments in the segment. It’s a global brand with more than 25,000 stores spread across 75 countries, and has no direct competitor of scale to challenge its premium coffee house positioning. At a forward P/E of 20, the stock certainly looks like an attractive investment for the long term.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Â