It looks like China may be folding.

We’ve talked all year about how China is the largest driver of markets this cycle and their deleveraging was the force behind the widening performance gap between the U.S. and the rest of the world.

The continuation of this trend has been dependent on China’s willingness to stay the course and press on with much-needed financial and economic reform. A reversal of policy would be seen as a failure and a direct hit to Xi Jinping’s credibility.

Cue recent reports indicating the Chinese Communist Party can’t take the heat and has decided to ease once again. Here’s Bloomberg's take on China’s policy U-turn (author's emphasis):

China unveiled a package of policies to boost domestic demand as trade tensions threaten to worsen the nation’s economic slowdown, sending stocks higher.

From a tax cut aimed at fostering research spending to special bonds for infrastructure investment, the measures announced late Monday following a meeting of the State Council in Beijing are intended to form a more flexible response to “external uncertainties” than had been implied by budget tightening already in place for this year.

Fiscal policy should now be “more proactive” and better coordinated with financial policy, according to the statement — a signal that the finance ministry will step up its contribution to supporting growth alongside the central bank. The People’s Bank of China has cut reserve ratios three times this year and unveiled a range of measures for the private sector and small businesses.

“It is now quite clear that Beijing has fully shifted its policy stance from the original deleveraging towards fiscal stimulus that will be underpinned by monetary and credit easing,” said Lu Ting, chief China economist at Nomura Holdings Inc. in Hong Kong.

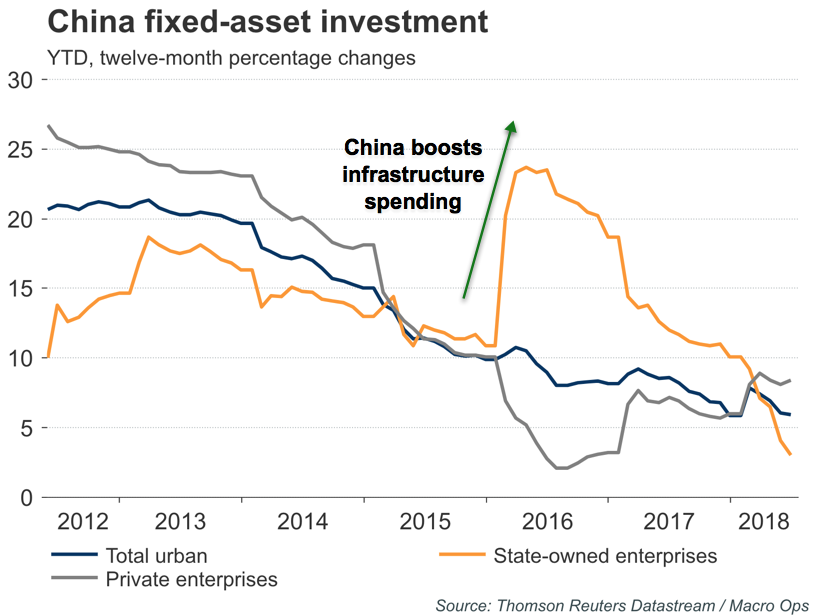

China’s State Council plans to raise local government spending by roughly 1.35 trillion yuan ($200 billion), which is to be spent primarily on infrastructure this year.

And the tax cuts aimed at boosting consumer spending are equivalent in size to the tax cuts passed last year in the U.S. — not an insignificant amount.

Why has China decided to backpedal on what was one of Xi’s and the party’s top goals last year?

It seems there’s increasing fear at the top of losing control of the economy and this fear is being exacerbated by the escalating trade war. Chinese State media recently warned that the Asian country's judiciary should prepare itself for a possible spike in corporate bankruptcy cases as a result of the trade dispute with the U.S.

The South China Morning Post recently published the following (author's emphasis):

In an opinion piece published on Wednesday by People’s Court Daily, Du Wanhua, deputy director of an advisory committee to the Supreme People’s Court, said that courts needed to be aware of the potential harm the tariff row could cause.

“It’s hard to predict how this trade war will develop and to what extent,” he said. “But one thing is sure: if the US imposes tariffs on Chinese imports following an order of US$60 billion yuan, US$200 billion yuan, or even US$500 billion, many Chinese companies will go bankrupt.”

As Chinese courts have yet to have any involvement in the trade dispute, the fact that the newspaper of the nation’s top court, ran an opinion piece – for a judiciary-only readership – suggests concerns might be rising in Beijing about the possible socioeconomic implications of the row.

There’s also been a number of reports (so far, unverified) over the last few weeks of serious trouble brewing within the party. Geopolitical Futures recently shared the following:

Last Friday, online reports indicated that gunfire had been heard for roughly 40 minutes in Beijing near the Second Ring Road. The reports claimed it was a violent spasm by groups that sought to overthrow Chinese President Xi Jinping. The following day, French public radio reported it had heard rumors that former Chinese leaders, including Jiang Zemin and Hu Jintao, had allied with other disgruntled Chinese officials in an attempt to force Xi to step down. A Hong Kong tabloid went so far as to suggest that Wang Yang, chairman of the Chinese People’s Political Consultative Conference, might be the compromise leader next in line.

It’s impossible for us to know if there’s any truth to these rumors (China keeps a tight lid on these types of things), but just the fact that they’re circulating are an indication of growing unease with the state of the Chinese economy. It may also be why we’re seeing this policy change by the Chinese Communist Party.

We also don’t know if this easing will be enough to reverse the negative trends kicked into gear by the initial deleveraging, nor do we know how long and aggressive the Chinese Communist Party will be in this round of easing. All we know for sure is that however they choose to carry it out, policy will continue to have an outsized impact on markets and the global economy.

For our part, we just have to keep a close eye on the data and change up our positioning to account for the new uncertainty created by this shift back to easing.

Two important data points we’ll want to watch in order to gauge the scale of the current easing response are fixed asset investment (i.e., infrastructure spending) and China’s M1 money supply (which has a close leading correlation to changes in industrial metal pricing).