On July 15, 2026, we present a DCF analysis for Sherwin-Williams Co SHW, a company currently trading at $328.50. Over the past year, SHW has experienced a price decline of 3.8%, reflecting some volatility in its stock performance.

- DCF Earnings-based intrinsic value of $218.38 vs current price of $328.50 (margin of safety: -50.4%)

- DCF FCF-based intrinsic value of $167.65 vs current price (second opinion)

- GF Score™ of 87/100 indicates high reliability of the DCF inputs

What Is SHW Worth? DCF Earnings-Based Model

The DCF earnings-based model for Sherwin-Williams Co SHW utilizes a two-stage approach to estimate the intrinsic value of the stock based on its expected earnings growth. The first stage accounts for a high growth rate over the next ten years, while the second stage reflects a more stable growth rate thereafter. Below are the key assumptions used in this model:

| Parameter | Value |

|---|---|

| Current EPS (TTM, excl. non-recurring) | $11.55 |

| 10-Year Growth Rate | 12.5% |

| 10-Year Treasury Rate | 4.61% |

| Discount Rate (ceil(Treasury) + 6%) | 11% |

| Terminal Growth Rate | 4% |

In the first stage, we project that EPS will grow at 12.5% per year for the next ten years, which is then discounted back to present value at a rate of 11%. The value derived from this growth stage is $124.44 per share. In the second stage, we assume a terminal growth rate of 4% for the following ten years, which also gets discounted at the same rate, yielding a terminal stage value of $93.94 per share. The summary of these calculations is as follows:

| Stage | Description | Value |

|---|---|---|

| Growth Stage (Years 1-10) | EPS growing at 12.5%, discounted at 11% | $124.44 |

| Terminal Stage (Years 11-20) | 4% terminal growth, discounted at 11% | $93.94 |

| Intrinsic Value | Growth + Terminal | $218.38 |

Comparing the current price of $328.50 to the intrinsic value of $218.38 indicates that SHW is modestly overvalued, with a margin of safety of -50.4%. It is important to note that GuruFocus uses EPS excluding non-recurring items, as research shows stock prices correlate more closely with earnings than free cash flow. For further details, you can access the SHW DCF Calculator.

What Does the Free Cash Flow DCF Say?

In addition to the earnings-based model, we also analyzed Sherwin-Williams Co using a free cash flow (FCF) DCF model. The FCF-based intrinsic value calculated is $167.65. This value is significantly lower than the earnings-based intrinsic value of $218.38, suggesting a divergence in the two valuation approaches. Both models indicate that SHW is modestly overvalued, with the FCF model showing a margin of safety of -95.9%.

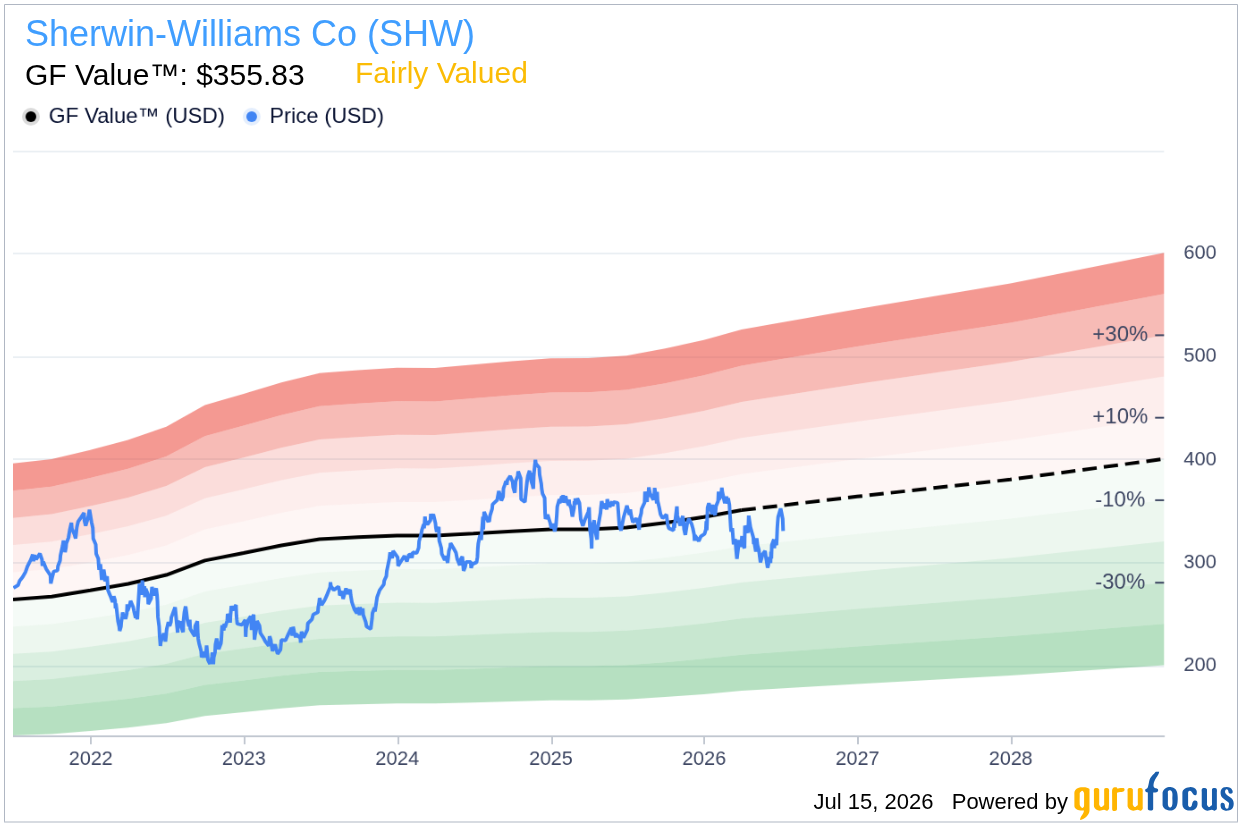

How Does GF Value™ Compare to the DCF Models?

The GF Value™ for Sherwin-Williams Co is calculated at $355.83, providing a third perspective on the valuation of the stock. GF Value™ is GuruFocus' proprietary measure derived from historical trading multiples, past business growth, and future performance estimates. While the DCF models suggest that SHW is overvalued, the GF Value™ indicates that it is undervalued. This discrepancy highlights the importance of considering multiple valuation methods. For more information, visit the GF Value™ page.

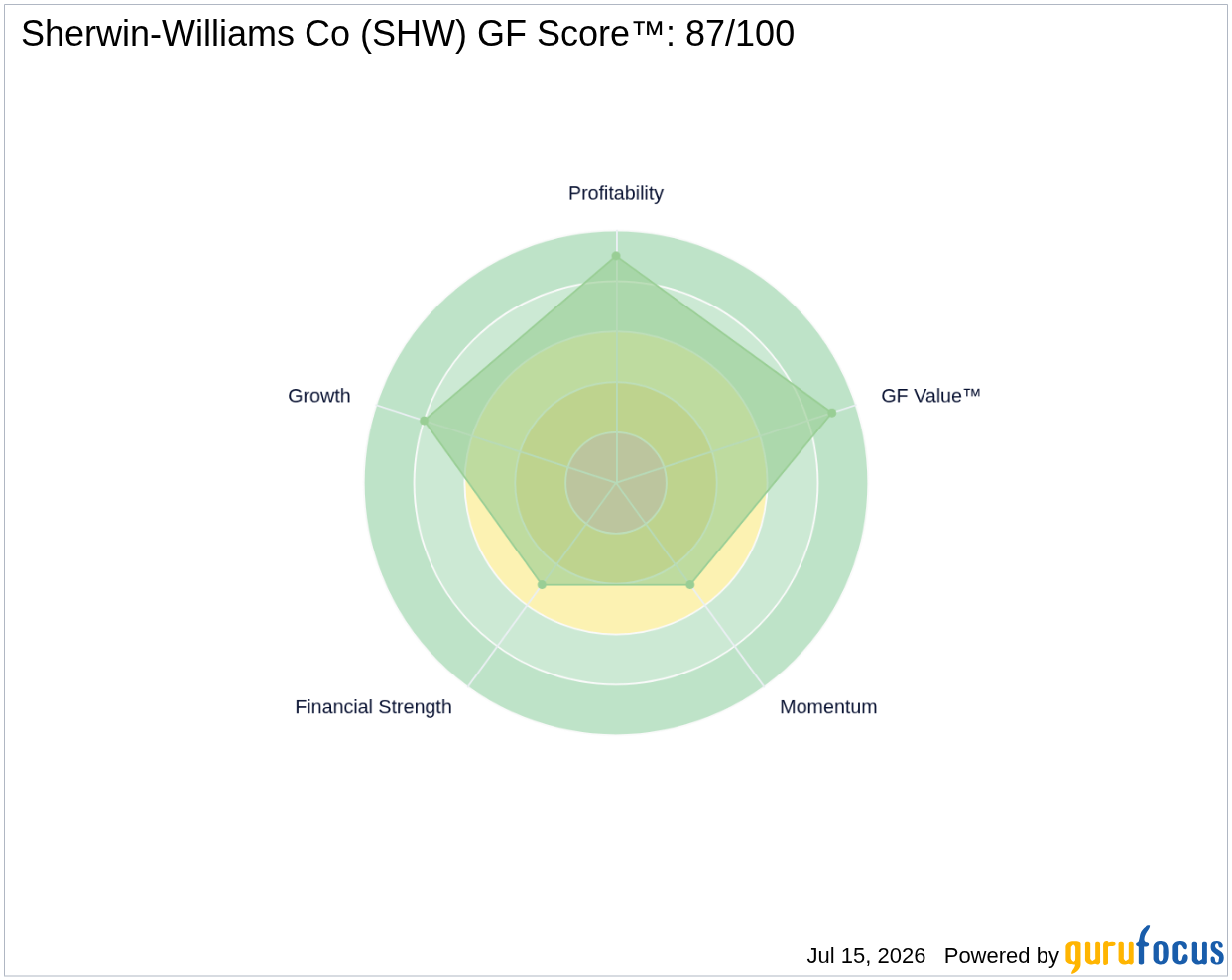

What Does SHW's GF Score™ Tell Us?

The GF Score™ ranks stocks from 0 to 100 based on five key aspects: Financial Strength, Profitability, Growth, Valuation, and Momentum. Stocks with higher GF Score™ values have been found to generate higher long-term returns based on backtested data from 2006 to 2021. Below is the GF Score™ breakdown for Sherwin-Williams Co:

| Metric | Rating |

|---|---|

| GF Score™ | 87/100 |

| Financial Strength | 5/10 |

| Profitability | 9/10 |

| Growth | 8/10 |

| Valuation | 9/10 |

| Momentum | 5/10 |

With a predictability rank of 2 out of 5 stars, it suggests that the DCF model may be less reliable for this stock. For more detailed information, visit the SHW stock page.

Key Assumptions and Limitations

It is important to note that DCF models are highly sensitive to the assumptions made regarding growth rates and discount rates. Stocks with low predictability ratings, such as Sherwin-Williams Co, tend to produce less reliable DCF estimates. The terminal growth rate of 4% is a simplifying assumption that may not fully capture future market dynamics.

What This Means for Investors

In summary, the three valuation models—DCF earnings, DCF FCF, and GF Value™—present a mixed picture for Sherwin-Williams Co. The DCF models suggest that the stock is overvalued, while the GF Value™ indicates it may be undervalued. Overall, investors should consider these differing perspectives when evaluating SHW's investment potential. For the full DCF analysis, visit the SHW DCF Calculator. You can also explore the GF Value™ page, or use the GuruFocus Stock Screener to find undervalued predictable companies.

Frequently Asked Questions

What is SHW's intrinsic value based on DCF?

[Answer: earnings-based $218.38, FCF-based $167.65]

Is SHW overvalued or undervalued?

[Answer using DCF + GF Value™ consensus]

How reliable is the DCF model for SHW?

[Answer using predictability rank 2/5]

This stock alert was generated using automated technology and GuruFocus financial data to provide readers with timely and accurate market reporting. This content was reviewed by GuruFocus editorial team prior to publication. Please send any questions or comments about this story to [email protected].