IBM (IBM) has been reporting decent results, despite the pandemic. More importantly, the financial results show that IBM's corporate strategy is now de-emphasizing financial engineering via stock buybacks and focusing more on growth and deleveraging.

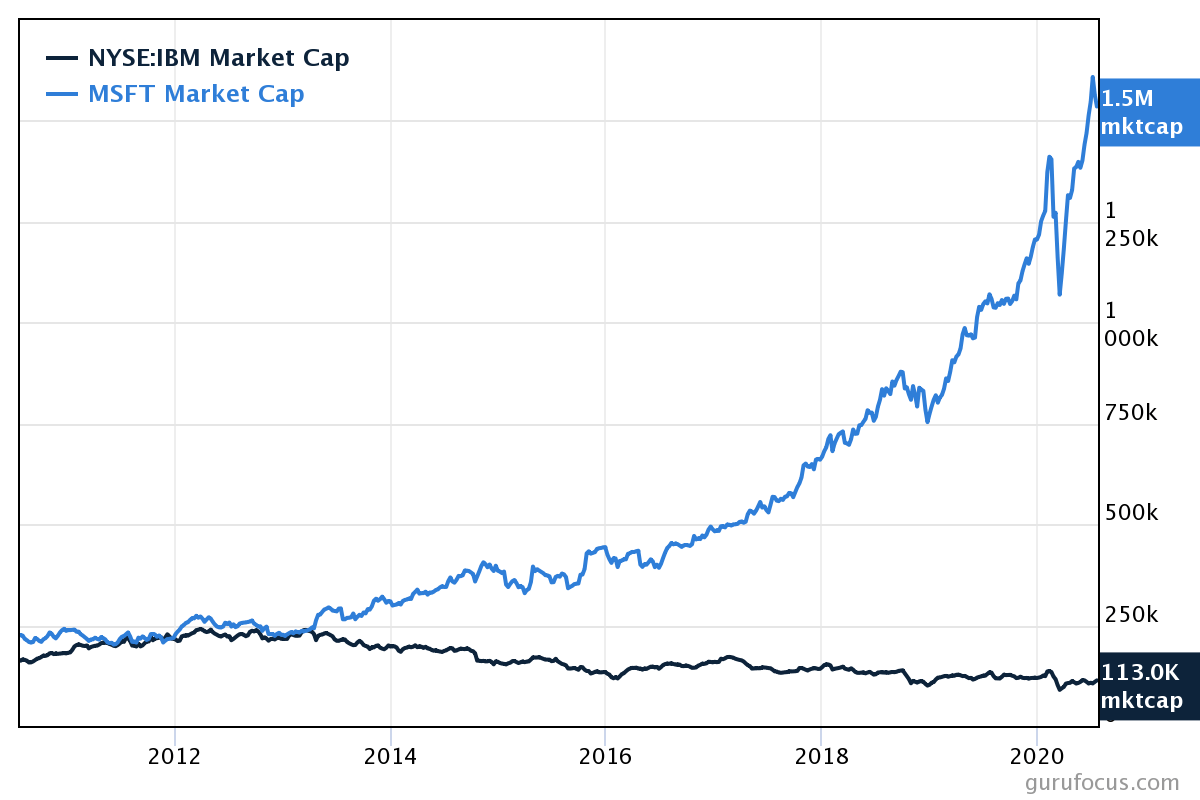

Last year, IBM, often called by the nickname "Big Blue," made one of the most important acquisitions in its history, the acquisition of RedHat. Then, it replaced its CEO with a new one. This is somewhat reminiscent of what Microsoft (MSFT) did in 2014 by replacing a former "marketing/sales/finance" oriented CEO with one with a strong tech and R&D background. Satya Nadella shifted Microsoft decisively towards the Cloud, and the market cap has compounded by 600% (see chart below comparing Microsoft with IBM).

The board at IBM is probably hoping that the new CEO, Arvind Krishna, can ignite IBM's growth, similar to what Nadella did with Microsoft. Krishna was the executive who led the Red Hat acquisition and integration. While its too late to catch the leaders in the cloud space, the market is so large that it's possible IBM can carve out a profitable position.

Source: Gurufocus.com

Source: Gurufocus.com

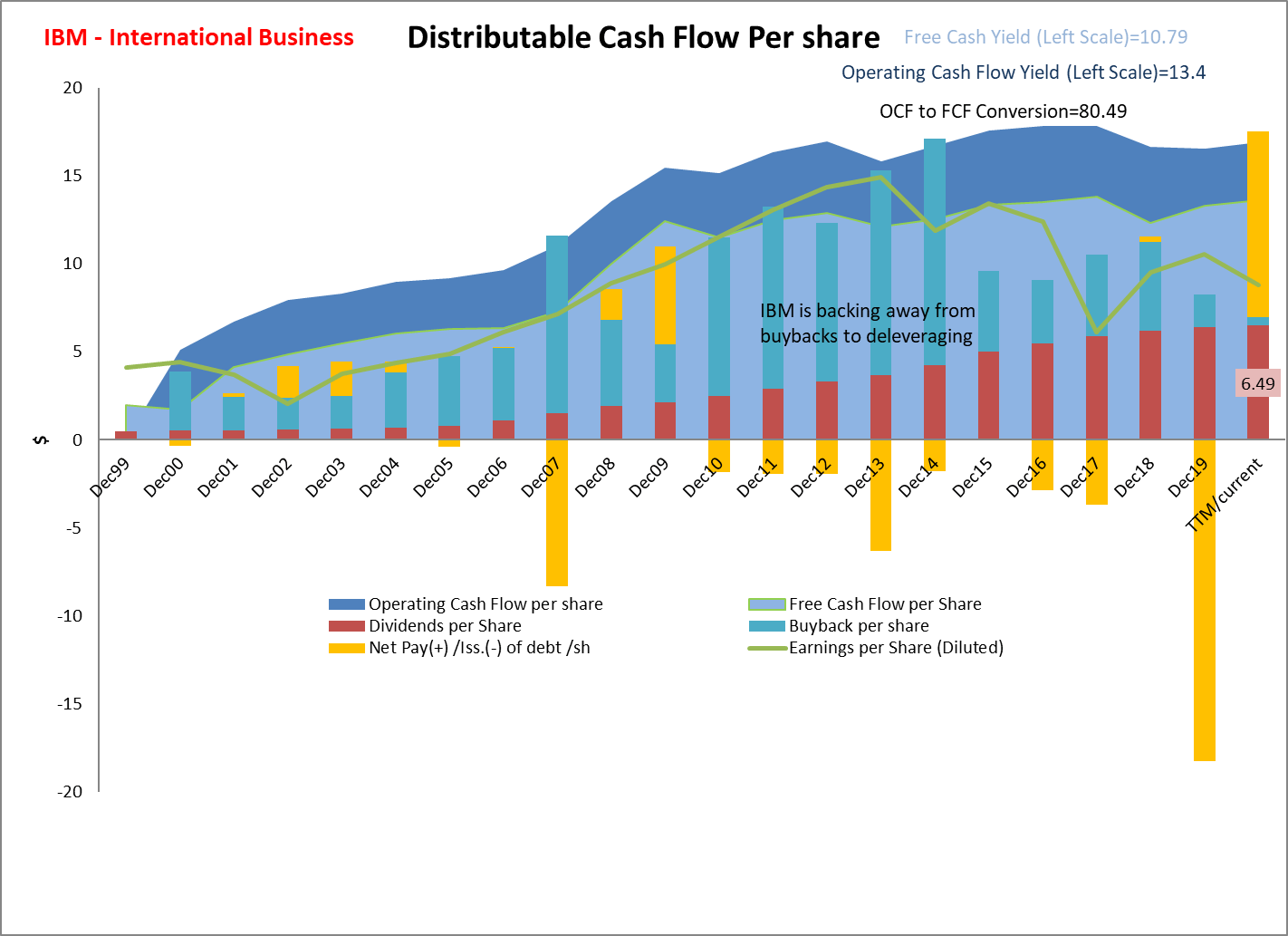

Stock buybacks have Slowed

I think a CEO change with a mandate for growth can result in a discontinuity in a company's former trajectory. This appears to be starting at IBM. I would like to draw your attention to the following chart, which lays out IBM's cash flow per share going back 20 years. While the chart is complex, it carries a lot of key information that will help understand the situation.

The dark blue area shows the operating cash flow (OCF) per share, while the light blue area shows the free cash flow (FCF) per share. Both remain very robust. The green line tracks GAAP earnings per share (EPS). The stacked bars show IBM's dividend, share buybacks and cash flow from debt (all normalized to per share, per year). Dividends are red (IBM paid $6.49 per share in dividends over the last 12 months). The teal part of the stacked bar shows the amount (on a per share, per year basis) IBM spent in buyback shares. Buybacks in theory are supposed to benefit shareholders and so are classified as "return to shareholders." The yellow stacked bars are the net long term debt (on a per share, per year basis) IBM had taken or paid off. Yellow stacked bars below zero represent an increase in debt, while the yellow bars above zero represent decrease in debt. Again, as owners of the company, shareholders benefit when debt is paid off.

Source: Author, with data from Gurufocus.com

Since the year 2000, IBM spent a lot of cash flow buying back shares while also increasing debt. In fact, from 2010 to 2017, IBM took on net debt to buy shares. This was misguided in hindsight, as resources should have been directed to business building activities such as making large acquisitions to position the company into emerging areas. While Amazon (AMZN), Microsoft and Google (GOOGL) were building their moats in the cloud, IBM was busy doing financial engineering. While IBM execs constantly talked about cloud and cognitive computing, the rhetoric was not matched by results, and IBM kept falling behind the curve.

Finally, in 2019, IBM bought Red Hat, a fast-growing opensource cloud company. As can be seen from the chart above, IBM took on a big slug of debt to fund the acquisition. What is interesting is that in the last 12 months IBM has paid back a lot of that debt from operating cash flow and has reduced buybacks to a minimum. It looks to be a change of thinking has happened in the top leadership and a realization that financial engineering is not paying off. This is welcome news, in my opinion.

Revenue growth

Investors are especially keen to see IBM grow overall revenue. With the pandemic still raging, it too early to see substantial revenue growth following the Red Hat acquisition. Organizations are spending the bare minimum in the face of massive uncertainity.

Revenue did increase by 3.14% from last quarter, though it fell 5.43% from the same quarter last year. So, all in all, it was a flat revenue quarter at best. Cloud revenue (including Red Hat) grew by 30% and AI/cognitive revenue grew 8%, but pretty much all other segments fell.

It's good that overall revenue has not fallen in these times, and I believe revenue growth will return when business normalizes. The problem which IBM has to manage is that while it pushes on cloud and AI, it is slipping in business services, particularly on systems (IBM Z mainframes, storage, etc.). The latter is a very high margin business but in secular decline. In fact, IBM's overall operating margins have slipped from ~18.5% 10 years ago to ~12.5% now. So for every dollar of "legacy" revenue lost, IBM is faced with generating a dollar and fifty cents to maintain profitability.

This is a classic "innovators dilemma" which competitors like Amazon and Google do not have, though Microsoft did and is successfully navigating this challenge as it grows out of the Windows and Office monopoly. IBM can help transition its system Z customers into the open-source hybrid cloud instead of losing them to competitors. Hopefully, faster growth and volume can make-up for decreased operating margins.

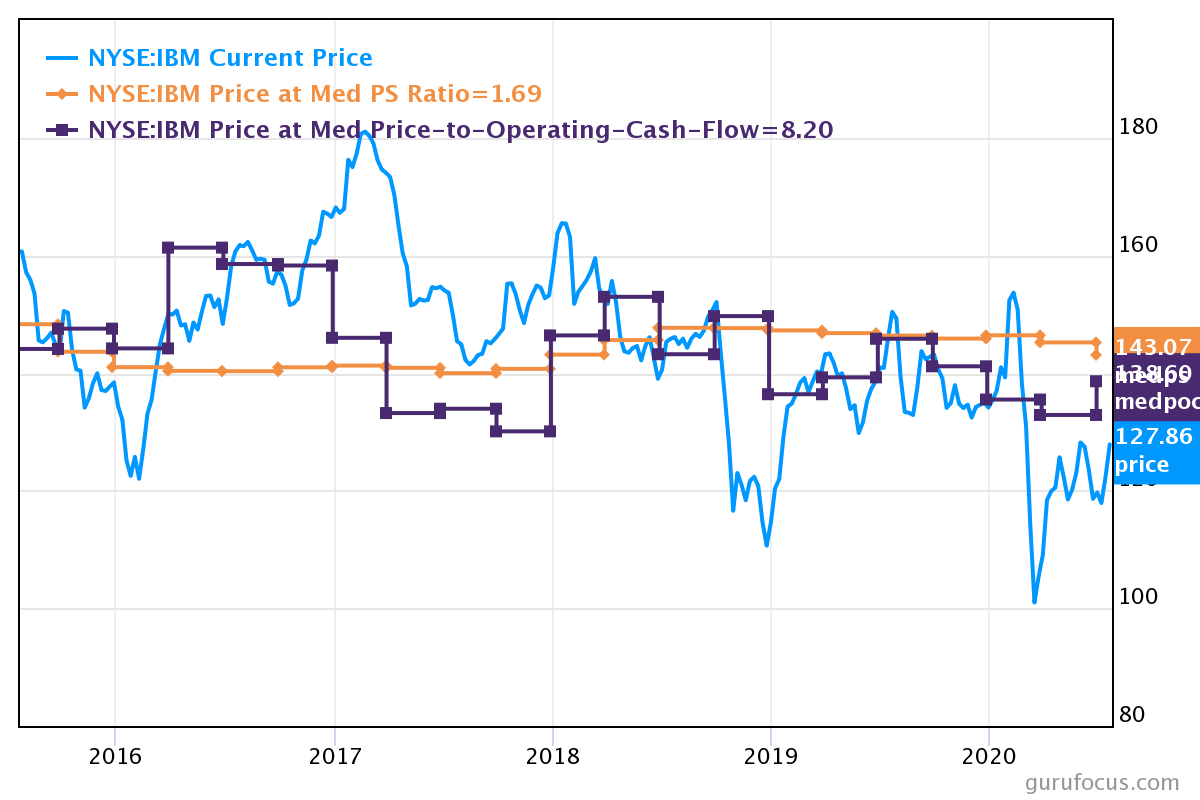

Valuation

Looking at median price-sales ratio and the price-to-operating-cash-flow ratio over the last five years, IBM appears to be moderately undervalued. Using this valuation model, I get a value between $138 to $143. I think this is conservative because if IBM shows revenue growth, these multiples will expand.

Using the Gurufocus two-stage discounted cash flow model with the assumptions given below, I get a value of over $180. This model assumes that IBM can grow free cash flow per share at the rate of 5% over the next 10 years and 2% for the following 10. Note that this is an aggressive assumption, as IBM grew FCF per share by only 1.2% per year in the last decade, so it assumes a solid turnaround. A cost of capital of 8% is also assumed.

Bottom line

I think IBM is a relatively low-risk way to get into the emerging areas of cloud and AI. It has the potential to become a strong #4 behind Amazon, Microsoft and Google. It has a long tail of declining but still highly profitable cash-producing businesses which can support investments in new areas.

Red Hat was a good start. However, its needs to continue making big and bold moves which can move the needle and de-emphasize short term shareholder returns such as stock buybacks and even dividends. The name of the game in the cloud and AI is growth. If Arvind Krishna and the team can deliver that, IBM can be worth multiples of where it is now. The alternative is stagnation, which in IT means death.

Disclosure: The author is long IBM.

Read more here:

- Berkshire Hathaway: Stepping Up Buyback of Shares

- Thoughts on the Cap Rate Metric and Simon Property Group

- Investment Note: Empire State Realty Trust

Not a Premium Member of GuruFocus? Sign up for a free 7-day trial here.