I started researching the housing industry and was lucky to stumble upon a couple of research papers. One paper titled, "Homebuyer Insights," was released by Bank of America (BAC, Financial). Bank of America surveyed 1,000 adults in 10 major metropolitan areas to assess homebuyer attitudes. The other paper is titled, "America’s Rental Housing." It discusses trends in the rental market and was released by Harvard. Each study revealed insights that contradicted my preconceptions.

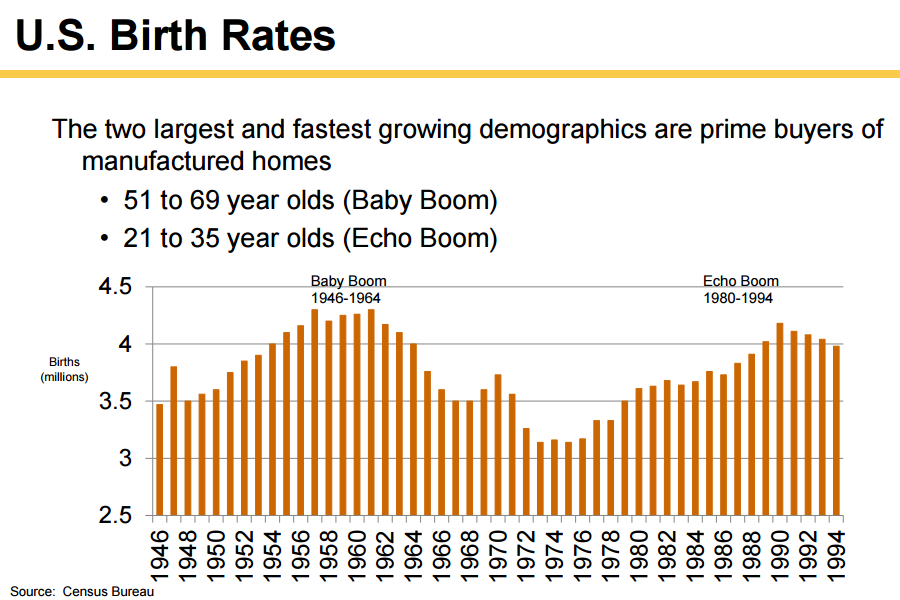

My interest in researching homebuilders started from noticing favorable demographic trends. The graph below is from Cavco, the nation’s second-largest U.S. home builder by market share, which serves the affordable housing market. It shows how the millenial generation, those born from 1980 to 1994, is entering into peak household formation years. It’s reasonable to forecast that demand for home ownership will go up as millenials age. The papers from Bank of America and Harvard, on the other hand, give a more complicated picture of the housing market and spotlight issues related to home buyers.

Homebuyer insights by Bank of America

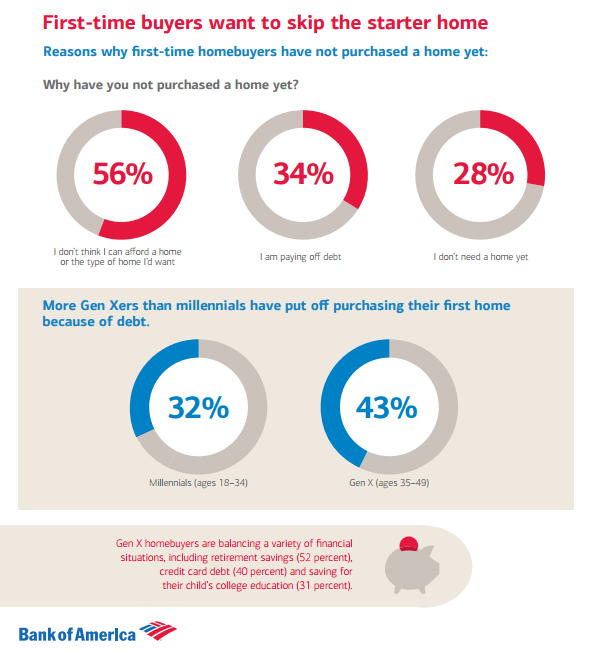

The first interesting and surprising insight from Bank of America is that many first-time buyers want to skip the starter home and go straight to buying a home that will meet long-term needs. Only 25% preferred buying a starter home over waiting for a long-term home; 69% of respondents were willing to take longer to save money so that they could purchase their long-term home.

Twenty-eight percent don’t feel the need to purchase a home. This may signal changing attitudes toward home ownership. Prior to the Great Recession, many people believed that houses were solid investments that always went up over time. The housing crash changed that perception which has lowered the appeal of homeownership. Fifty-six percent cited lack of funds and 34% cited debt burden as reasons for not buying a home. A higher percentage of Gen X responders, those aged 35 to 49, have deferred buying a home when compared to millenials. One might guess that a higher percentage of Gen Xers are more financially burdened since they’re older and more likely to have children. In another post, I wrote about how Gen Xers have more student debt than millenials.

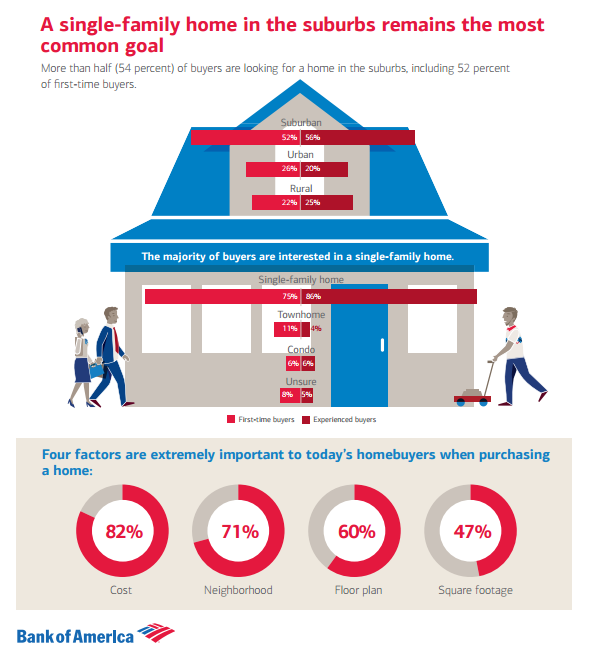

The survey also asked what type of homes people are most interested in. By a wide margin, respondents chose suburban homes over other locations; 52% wanted suburban versus 26% for urban and 22% for rural.

Rental housing study by Harvard

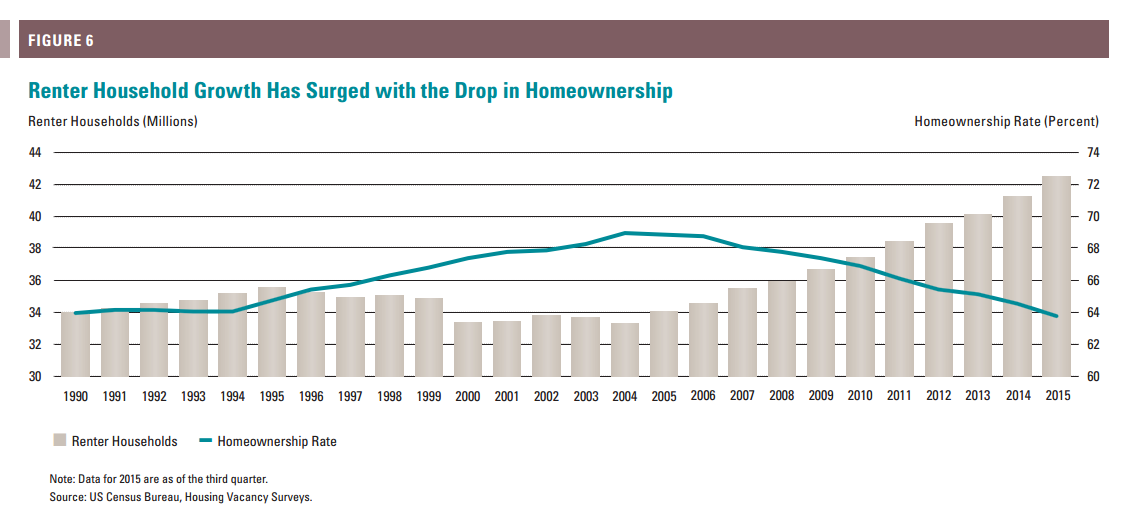

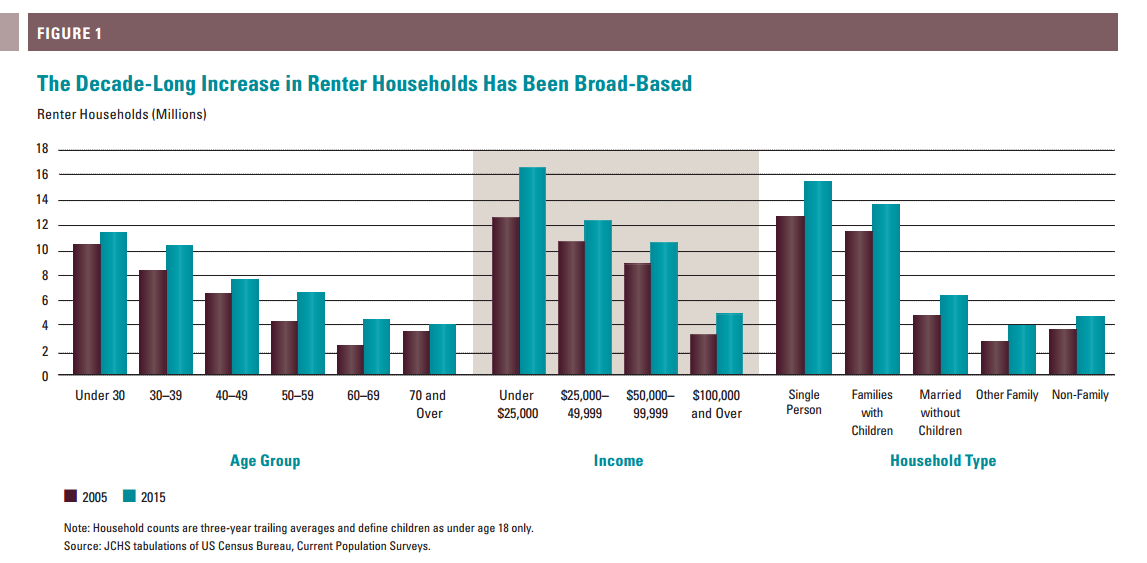

The America’s Rental Housing study by Harvard shows how home ownership rates have fallen to a level not seen since the early 1990s. At the same time, it shows how renter households have skyrocketed starting from 2004 onward. As a result, the rental housing stock grew by approximately 8.2 million units from 2005 to 2015.

One explanation for these trends might involve the fact that between 2001 and 2014, real rents rose 7% while household incomes fell by 9%. Housing costs are becoming more burdensome and are obstacles to saving for down payments on homes. Renters of all age groups, income levels and family types have increased. A common assumption is that renters are largely comprised of younger people, but the numbers show that there are more renters over the age of 30 than under 30. There’s been an especially pronounced increase of renters aged 50 to 69 since 2005.

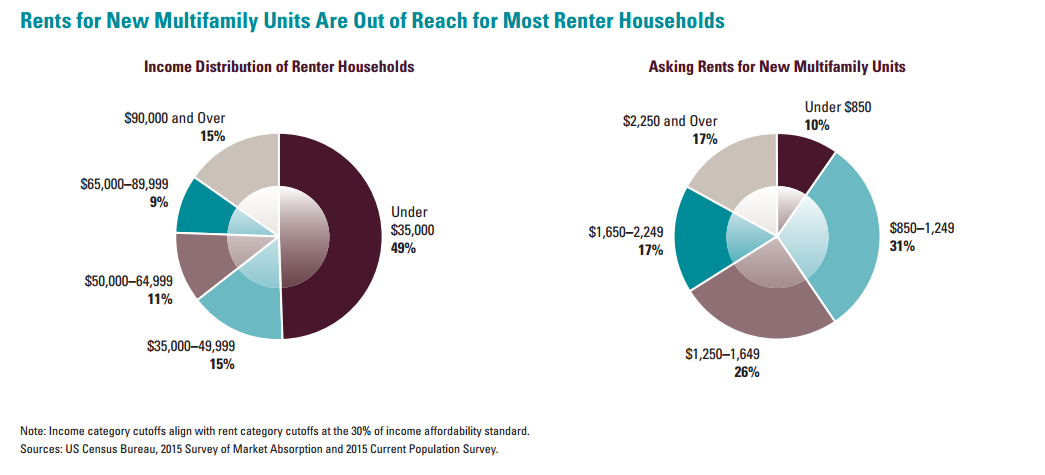

Harvard’s paper paints a picture of a divided rental market. One segment is geared toward higher income consumers. On the other end, there is a much larger number of consumers in need of affordable housing. The problem is that the needs of the consumer and the economic incentives of home builders and municipalities are not aligned. Home builders and municipalities want to maximize profit and tax revenue by building more expensive units.

Land is a fixed cost. It’s more profitable to build expensive units to get the most out of that land. In addition, many municipalities have zoning laws limiting the number of multifamily units which prevent builders from lowering per unit costs. These factors lead to more supply of expensive rental units and less supply of affordable housing units. Not enough affordable housing units are being built. There’s also demolition of existing lower cost units as they deteriorate and become uninhabitable which again reduces supply. The charts below show how many renters can’t afford newly built rental units. In the meantime, vacancy rates have fallen and rents keep going up. It’s possible for markets to be oversupplied with luxury apartments and undersupplied with affordable housing.

Final thoughts

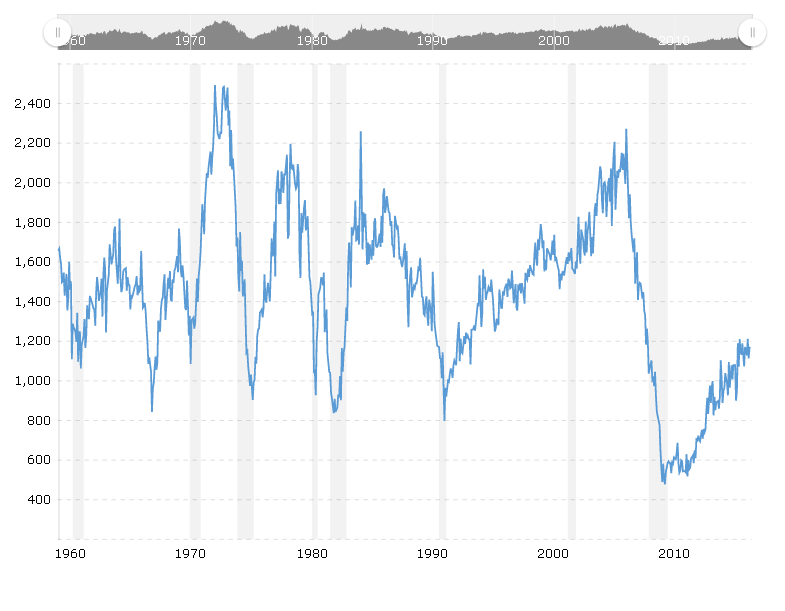

From an investor perspective, one might look at the historical low housing starts we’re currently experiencing and hypothesize that there will be reversion to the mean and home builders may be a good place to invest. The graph below shows housing starts going back to 1960.

It’s a good idea to ask what’s changed. We don’t know if millenials will aspire to home ownership in the same percentages as baby boomers. We don’t know if they will want marriage or kids so we don’t know what type of houses they will consider as starter homes versus long-term homes. What I do know is that the homebuilder industry is challenging. There are long lead times as companies need to buy land and go through the permitting process. There are low barriers to entry. In addition, weather can be a huge problem. In other manufacturing industries if one factory runs into problems, companies can divert resources to other factories to compensate for the shortfall. For homebuilders, if there’s extreme weather like flooding, there’s no way to make up for lost time. Financing is another unpredictable variable. In some areas, home builders are having problems finding enough skilled laborers. The list of challenges goes on and on.

Industry resources like Bank of America’s survey and the Harvard paper are extremely valuable in my research process. I especially like impartial sources like Harvard where there’s no conflicting agenda. They are studying an industry to develop policy prescriptions.

On the other hand, I take surveys from private companies with a grain of salt. If Bank of America produced a survey that showed nobody wants to buy homes, that would have negative implications for their business and one wonders how much biases may color the findings.

Start a free seven-day trial of Premium Membership to GuruFocus.