In an earlier article on Netflix (NFLX, Financial) earnings this past quarter, I explained why the market was so intolerant of its performance. The 800,000 subscriber miss left it wide open to market reaction, and it paid the price.

It's somewhat recovered since then, but it’s clear that investors are only looking at subscriber numbers each quarter, and that poses a problem for Netflix on the home front.

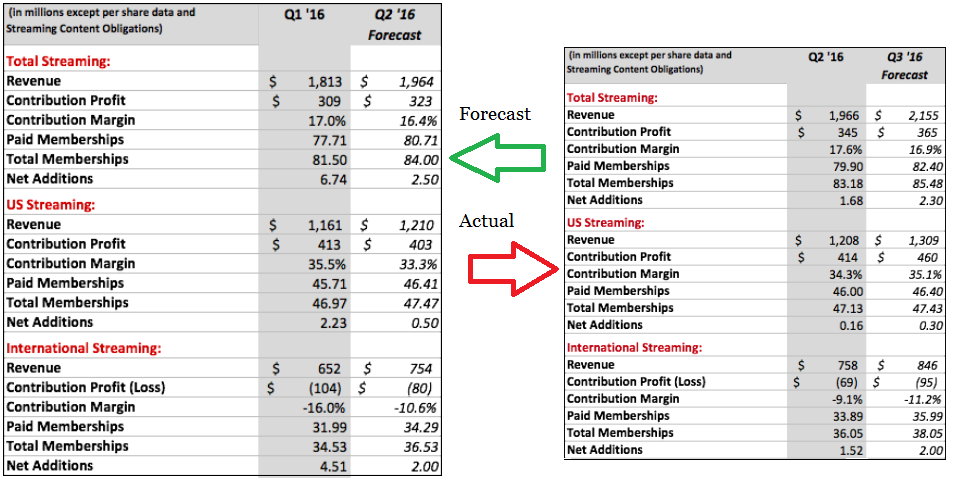

With 46 million paid members in the U.S., it's reached a high level of penetration among Internet users. But comparing that with the population isn’t a good indicator of penetration because many subscribers share their connections with family members. In fact, that’s how the subscriptions are designed. With the $8.99 and $11.99 plans, users can simultaneously watch on multiple screens.

Source: Venturebeat

So the best number to go after is the number of households or housing units in the U.S., which stood at 134.789 million in July 2015 according to Census.gov. Now, at the end of the first quarter of the current fiscal, about 91.54 million have broadband connections, which is ideally what you require for streaming video. And that’s the figure that tells us that 46 million subscribers gives Netflix a 50% market share in the U.S., confirming its status as the king of paid streaming video.

Why the competition hasn’t arrived yet

According to Netflix CEO Reed Hastings, the company’s lower subscriber adds this past quarter has little to do with the competition. One would assume that with so many streaming platforms available the competition would be intense. But this is what it said in its second-quarter letter to shareholders:

“As Internet TV rises in popularity, so do the SVOD offerings. In the U.S., for example, CBS (CBS, Financial) All Access, Seeso, Amazon (AMZN, Financial) Prime Video, Hulu, YouTube Red and many others are all growing. Our view, however, is that we are all growing primarily against linear TV hours and that competition did not contribute materially to our miss in Q2.”

What we have, then, is a scenario where penetration rather than competition is causing a slowdown in subscriber base, and that’s only temporary. Of course, we can’t expect the kind of growth it showed five years ago in the U.S. to continue unabated, but we can expect a gradual decline in new subscriber growth over the next few quarters. Let’s not forget that its churn rates aren’t going to stay high forever either. That figure will also gradually settle down to where net impact is far less than it was during the second quarter.

The real advantage for Netflix

The only advantage Netflix has is that the competition is still not ready to compete with it on an even scale. To put it another way, it has not yet given Netflix users enough reasons to switch over. That advantage, however, is only for current video streaming users. Netflix will have to fight tooth and nail to continue adding new subscribers in a market where content from other networks may eventually be equally appealing.

The next five years will be the time for Netflix to hold its ground in its home market while establishing itself as the default choice in newer markets. In addition, it has to figure out how to become profitable internationally while the U.S. is still making money for it. This quarter it reported a contribution profit of $414.359 million in the U.S. and a loss of $69.184 million from international operations. That has to change in the next five years; both figures need to be in the black. The only way to make that happen is to look for more localized content overseas or offer dubbed audio for existing content. Right now it only does it in about 20 or so languages, and this needs to increase along with its subscriber base overseas.

With Amazon Prime Video now in the fray with stand-alone monthly subscriptions, the ecommerce giant’s arms are reaching out into Netflix’s territory. It's recently launched Prime in India, which could turn out to be its second-largest market after the U.S. There are literally hundreds of millions of potential subscribers up for grabs in markets like this. Besides, it’s only a matter of time before Amazon Prime, YouTube Red and other providers add enough original content and move heavily into such markets to give Netflix a run for its money overseas.

Netflix will continue to grow, but with the stock trading at 5.4 times sales investors may not have enough cover. DCA (dollar-cost averaging) is the only way to build your position in this company, but remember that the stock will continue to be extremely dependent on subscriber numbers to keep up the high valuation. As such, these “subscription shockers” could provide you with ample opportunities to invest.

Disclosure: I have no positions in any stocks mentioned and no plans to initiate any positions within the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.